After the pandemic savings glut

18 JUL, 2023

By DWS

Like a series of gigantic natural experiments, the Covid-19 pandemic has provided a wealth of data to test causal mechanisms in various disciplines. For years, epidemiologists will be pondering the implications of different health policy interventions, while neurologists will study the clustering of usually rare autoimmune diseases around Covid hotspots.

Similarly, economists are taking a fresh look at how to think about the aftermath of recessions generally, in the light of pandemic recovery experiences around the globe.

Specifically, much attention is being devoted to household savings behavior. For example, a recent note by economists at the U.S. Federal Reserve board argues that in the United States excess savings, arising from above-trend savings rates, have largely been depleted by spring 2023. They also project that the remaining stock of excess savings in other advanced economies will be depleted by the end of 2023. Potentially, that could remove an important source of support for global aggregate demand.

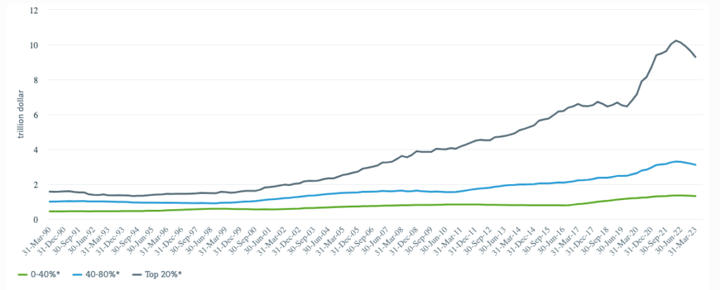

Trends in savings among U.S. households have been very uneven across different income groups

* Level of U.S. households' deposits by income group and its percentile. Sources: Federal Reserve Board (FRB), DWS Investment GmbH as of 7/12/23.

We are not quite so sure, but find the analysis intriguing. As our Chart of the Week shows, the decline in excess U.S. savings appears highly uneven, if one looks at household bank deposits at different levels of income. Much of the savings depletion took place among high U.S. earners, within the top 20% of households grouped by income percentiles. Such households typically have lower marginal propensities to consume.

Instead, the wealthy tend to smooth consumption over the lifetime of individual household members, reacting only slowly to sudden changes in wealth or income. The reverse tends to be true for less wealthy, lower income groups. As our chart shows, among lower income percentiles, there still remains some firepower in terms of bank deposits held by middle class and lower-income households. The working poor have also lately seen above average wage gains, reflecting tight U.S. labor markets. We believe, the remaining savings cushion of these groups should soften the blow, if and when the economy finally starts to shrink.

Behind all these trends also lie the many disruptions of pandemic life, from lockdowns to supply chain disruptions, which we all still vividly remember, but which will not be immediately obvious to future statisticians from just looking at the data. This points to a broader problem: how to interpret the most recent data in terms of extrapolating trend lines from it. Without getting too technical on this, the Fed economists’ excess savings estimates implicitly assume that households will be a lot more frugal than pre-pandemic trends would have suggested. This is in line with good econometric practice in recent years – but not necessarily true for this particular question.

More generally, some theory does suggest that as an economy contracts, households, facing financial uncertainty, may generally wish to reduce their consumption and bolster their savings, which then get unwound as the economy recovers and households regain confidence. However, the ability of households to do so critically depends on fiscal and monetary policies paving the path to recovery, which historically have rarely been as generous as during the pandemic. Fascinating as early studies are, it will probably take quite a bit longer to fully assess the long-term implications. In the meantime, expect economists at the Fed – along with the rest of us – to remain, you guessed it, data dependent, not least in terms of household savings behavior.