Are emerging countries the new developed markets?

17 NOV, 2023

In 2023, it has become clear that the economic prosperity sustained by globalisation over the last two decades is no longer viable. The world has become more unstable, while the scientific community agrees that the health, climate and economic challenges of the last three years were merely a prelude to the world of tomorrow. This observation leads us to believe that it is essential to broaden our investment universe while continuing to closely scrutinise the quality of macroeconomic fundamentals.

Developed countries face an unprecedented situation

In our article “Shift in Context for the Bond Markets”, we highlighted a significant paradigm shift, we highlighted a significant paradigm change: after years of rock-bottom interest rates, during which governments financed themselves cheaply, inflationary pressures and the rapid rise in interest rates that followed are placing Western economies, whose debt has traditionally been perceived as a safe haven, in a unique economic situation.

Indeed, the question of their capacity to bear the higher costs of refinancing their debt has

clearly arisen. While the situation in the United States is vulnerable, but less questionable thanks to a certain dynamism in economic activity, the situation in Europe is more worrying, since the massive fiscal spending made possible by the accumulation of zero-cost debt issues has not succeeded in creating sufficient production value within the economies over the medium term.

In concrete terms, the European economy is hoping for growth of around 2% a year over the next few years, while the cost of maintaining this growth is, as at November 2023, set at a reference value of 4.5% a year.

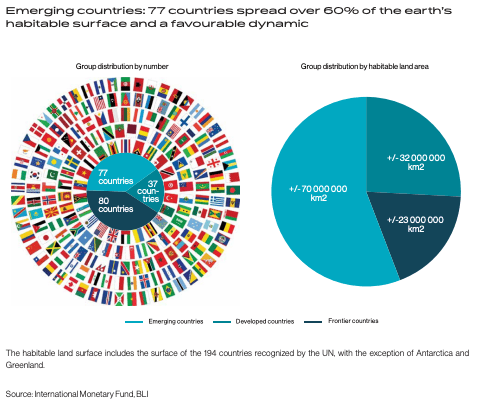

Over the last two decades, the international trade landscape has undergone profound changes that have redefined the drivers of international economic prosperity. Against this backdrop, emerging countries have managed to come out on top. First and foremost is China, which, with its affordable, skilled workforce, has benefited from these structural changes and attracted the bulk of the world’s production. The Chinese governing party, led by Xi Jinping, now holds the keys to global economic growth. Similarly, countries such as South Korea, driven by conglomerates like Samsung, LG and Kia, have succeeded in penetrating most of the old continent’s markets. In the tertiary sector, Oman, a small country in the south of the Arabian Peninsula, has become a luxury tourist destination. Chile, historically known for its landscapes, is now at the heart of the supply of resources needed to manufacture batteries.

These idiosyncratic economic stories reflect a geographical, cultural and economic diversification that seasoned investors can no longer ignore. Indeed, the growing importance of emerging economies is reflected in the financial markets. The investment universe for debt issued in hard currency is no longer limited to the Western countries whose economies are directly dependent on the euro or the dollar. Between 2000 and 2022, as euro and dollar rates fell, the secondary market for emerging country debt issued in hard currency consolidated. With an increasingly liquid market, the emerging market debt segment represents an attractive universe, if only for its size and diversity.

Why extend your investment universe to emerging countries?

In addition to the attractiveness linked to the above-mentioned characteristics of the universe, we have identified two main factors of long-term support: demographics and technological progress. Against these two favourable trends, however, the factor of the quality of governance in emerging countries must always be taken into account.

Demographics: a young population that rewards work

The world’s population increases every year, but the trends are different depending on

whether we analyse what is happening in developed or emerging countries. The age pyramid in advanced economies is in fact inverting, a phenomenon that is particularly marked in Europe. What’s more, while social benefits have been strengthened in the economic structure of developed countries, it seems that the value of work has been eroded, giving way to a fall in productivity. The structural effects of an ageing and less productive population are numerous. On the income side, the tax revenues received by governments will shrink, resulting in less flexible budget spending. While migration policies could be a solution to Europe’s demographic problem, history shows us that European cultures are not very inclusive, making such policies ineffective.

In contrast, emerging countries benefit from a younger, larger population that is beginning to

accumulate capital. This is evidenced by the increase in purchasing power that countries

such as Mexico, Indonesia and India have experienced over the last two decades.

The emergence of this middle class, which values work, is one of the structural factors

underpinning the sovereign debt of emerging countries. However, at present, a number

of factors are limiting the production and consumption capacity of this growing middle

class, notably the lack of financial inclusion and a level of corruption that is still too high.

Improving these two factors is essential to the long-term development of these societies. Medium- and low-income nations succeeding in including the majority of economic agents in their formal economy will increase their taxpayer base, resulting in greater flexibility and financial stability. These inclusion efforts must be accompanied by greater transparency of the economic system. Although some emerging economies have seen improvements in corruption and inclusion, notably in Eastern Europe, the road to full transparency remains arduous, with many challenges to overcome to avoid falling back into the mistakes of the past.

In 2023, it has become clear that the economic prosperity sustained by globalisation over the last two decades is no longer viable. The world has become more unstable, while the scientific community agrees that the health, climate and economic challenges of the last three years were merely a prelude to the world of tomorrow. This observation leads us to believe that it is essential to broaden our investment universe while continuing to closely scrutinise the quality of macroeconomic fundamentals.

Developed countries face an unprecedented situation

In our article “Shift in Context for the Bond Markets”, we highlighted a significant paradigm shift, we highlighted a significant paradigm change: after years of rock-bottom interest rates, during which governments financed themselves cheaply, inflationary pressures and the rapid rise in interest rates that followed are placing Western economies, whose debt has traditionally been perceived as a safe haven, in a unique economic situation.

Indeed, the question of their capacity to bear the higher costs of refinancing their debt has

clearly arisen. While the situation in the United States is vulnerable, but less questionable thanks to a certain dynamism in economic activity, the situation in Europe is more worrying, since the massive fiscal spending made possible by the accumulation of zero-cost debt issues has not succeeded in creating sufficient production value within the economies over the medium term.

In concrete terms, the European economy is hoping for growth of around 2% a year over the next few years, while the cost of maintaining this growth is, as at November 2023, set at a reference value of 4.5% a year.

Over the last two decades, the international trade landscape has undergone profound changes that have redefined the drivers of international economic prosperity. Against this backdrop, emerging countries have managed to come out on top. First and foremost is China, which, with its affordable, skilled workforce, has benefited from these structural changes and attracted the bulk of the world’s production. The Chinese governing party, led by Xi Jinping, now holds the keys to global economic growth. Similarly, countries such as South Korea, driven by conglomerates like Samsung, LG and Kia, have succeeded in penetrating most of the old continent’s markets. In the tertiary sector, Oman, a small country in the south of the Arabian Peninsula, has become a luxury tourist destination. Chile, historically known for its landscapes, is now at the heart of the supply of resources needed to manufacture batteries.

These idiosyncratic economic stories reflect a geographical, cultural and economic diversification that seasoned investors can no longer ignore. Indeed, the growing importance of emerging economies is reflected in the financial markets. The investment universe for debt issued in hard currency is no longer limited to the Western countries whose economies are directly dependent on the euro or the dollar. Between 2000 and 2022, as euro and dollar rates fell, the secondary market for emerging country debt issued in hard currency consolidated. With an increasingly liquid market, the emerging market debt segment represents an attractive universe, if only for its size and diversity.

Why extend your investment universe to emerging countries?

In addition to the attractiveness linked to the above-mentioned characteristics of the universe, we have identified two main factors of long-term support: demographics and technological progress. Against these two favourable trends, however, the factor of the quality of governance in emerging countries must always be taken into account.

Demographics: a young population that rewards work

The world’s population increases every year, but the trends are different depending on

whether we analyse what is happening in developed or emerging countries. The age pyramid in advanced economies is in fact inverting, a phenomenon that is particularly marked in Europe. What’s more, while social benefits have been strengthened in the economic structure of developed countries, it seems that the value of work has been eroded, giving way to a fall in productivity. The structural effects of an ageing and less productive population are numerous. On the income side, the tax revenues received by governments will shrink, resulting in less flexible budget spending. While migration policies could be a solution to Europe’s demographic problem, history shows us that European cultures are not very inclusive, making such policies ineffective.

In contrast, emerging countries benefit from a younger, larger population that is beginning to

accumulate capital. This is evidenced by the increase in purchasing power that countries

such as Mexico, Indonesia and India have experienced over the last two decades.

The emergence of this middle class, which values work, is one of the structural factors

underpinning the sovereign debt of emerging countries. However, at present, a number

of factors are limiting the production and consumption capacity of this growing middle

class, notably the lack of financial inclusion and a level of corruption that is still too high.

Improving these two factors is essential to the long-term development of these societies. Medium- and low-income nations succeeding in including the majority of economic agents in their formal economy will increase their taxpayer base, resulting in greater flexibility and financial stability. These inclusion efforts must be accompanied by greater transparency of the economic system. Although some emerging economies have seen improvements in corruption and inclusion, notably in Eastern Europe, the road to full transparency remains arduous, with many challenges to overcome to avoid falling back into the mistakes of the past.