EM Debt: Reassessing Risk Amid Resilience

11 JUL, 2023

By Barings

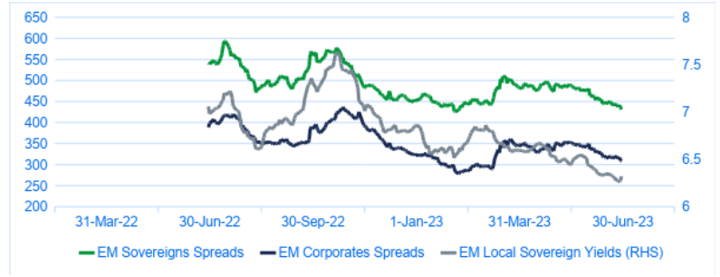

Against a backdrop of a relatively healthy global economy and resilience in household and corporate balance sheets, the second quarter saw positive performance for emerging markets (EM) sovereign, local, and corporate debt, with spreads tightening across the board.

EM spreads tighten across the board

Source: J.P. Morgan. As of June 30, 2023.

Sovereign & Local Debt: An Improving but Nuanced Picture

For EM sovereigns, the outlook appears quite positive. With inflation largely slowing, EM central banks are no longer hiking interest rates. Some central banks—in Costa Rica, Uruguay, and Hungary—already have cut rates while Brazil and Chile have indicated cuts may be coming soon. In addition, several tail risks have been moderated. Turkey, for instance, has appointed a new finance minister known for his more traditional policies, and Nigeria has a new administration offering the potential for reforms.

For sovereign and local debt, this backdrop presents both opportunities and challenges. For example, the differential between local rates and 5-year U.S. rates is near record low levels. That poses a headwind for local currencies, but if the U.S. Federal Reserve (Fed) is close to the end of its rate-hiking cycle, EM financial markets may be positioning themselves ahead of that move. At current levels, however, carry-through exposure to EM local debt remains For sovereign and local debt, this backdrop presents both opportunities and challenges. For example, the differential between local rates and 5-year U.S. rates is near record low levels1. That poses a headwind for local currencies, but if the U.S. Federal Reserve (Fed) is close to the end of its rate-hiking cycle, EM financial markets may be positioning themselves ahead of that move. At current levels, however, carry-through exposure to EM local debt remains attractive in many cases, with the Indonesian rupiah, Polish zloty, Mexican peso, and Peruvian sol looking particularly appealing. Meanwhile, the depreciation in the Chinese renminbi and South African rand looks likely to continue, while the Turkish lira may continue to be affected by government policies.

In terms of sovereign hard currency debt, while high-yield sovereigns recently outperformed investment grade, we believe this is not the time to add excessive risk. In fact, the countries driving the recent outperformance—including Ukraine, Tunisia, Ghana, and Zambia—may be too risky to warrant investment today. In an environment with tight credit conditions, we continue to see value in investment-grade sovereigns with strong fundamentals. Countries whose credit merits high yield status continue to find the cost of borrowing steep, and, in many cases, high enough to keep them out of the market. While we don’t see high-yield market dynamics changing much near term, we do see very select opportunities, specifically some positively trending BBs including Serbia, Oman, Morocco, and the Dominican Republic. We also continue to see value in Sri Lanka, which still trends positively while restructuring its debt.

Corporate Debt: A Case for Cautious Optimism

The recent EM corporate debt bounce-back that saw spreads narrow to levels prevailing just before the Russia-Ukraine war was driven by resilient corporate earnings and balance sheets, markets pricing in a relatively benign U.S. economic outlook and a possible Fed rate hike halt, and improvements in some idiosyncratic credit stories. The improvement in sentiment was reflected in high-yield corporates outperforming investment grade, and an increasing number of high-yield issuers accessing the new issue market.

Given the largely positive fundamental backdrop, EM corporate defaults remain low at 2.4%, driven mainly by Brazil as well as by China and Ukraine2. Staving off defaults, too, are indications of private credit stepping in and disintermediating banks in cases where public markets would not be accommodating.

While macro conditions largely support a glass-half-full outlook, risks persist, and the picture remains nuanced. Indeed, there are reasons for caution, and further spread tightening may be limited. Fund flows also remain negative. A return to inflows, however, could be a tailwind to drive spreads tighter. We see select opportunities at the high-quality end of the high yield corporate market, particularly BB names. We also see value in issuers with exposure to sectors related to climate transition, such as renewable power, as well as low-cost, high-quality producers, and companies involved in the structural shift taking place in the Gulf region. In the investment grade, we continue to see value in BBB-rated debt because it still offers some room for spread compression. In higher quality, selective opportunities remain.

Risks Ahead

Despite the Goldilocks state of the EM debt market—lower inflation, peaking interest rates, and a relatively strong global economy—risk is always present. Some of the macroeconomic, market and geopolitical risks we are monitoring include: an overzealous Fed that could tighten the economy into recession; IMF policies adversely affecting creditor rights; geopolitical tensions including frayed China/U.S. relations, Taiwan, and the Russia/Ukraine war; rising global food prices, which can lead to social instability in emerging markets; and surprising oil price stability that may indicate a global economy weaker than widely assumed.

As a result, we continue to believe that rigorous, bottom-up credit and country selection remains crucial to navigating the risks at hand and identifying the issuers that are well-positioned to withstand a changing environment.

For Professional Investors / Institutional only. This document should not be distributed to or relied on by Retail / Individual Investors. Any forecasts in this material are based upon Barings opinion of the market at the date of preparation and are subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance. Investment involves risk. The value of any investments and any income generated may go down as well as up and is not guaranteed by Barings or any other person. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

Barings is the brand name for the worldwide asset management or associated businesses of Barings. This document is issued by the following entity: Baring International Fund Managers (Ireland) Limited), which is authorized as an Alternative Investment Fund Manager in several European Union jurisdictions under the Alternative Investment Fund Managers Directive (AIFMD) passport regime and, since April 28, 2006, as a UCITS management company with the Central Bank of Ireland. 07/2991375

1Source: J.P. Morgan. As of June 30, 2023.

2Source: J.P. Morgan. As of June 30, 2023.