Fed cuts to be delayed to September, quarterly cuts to last longer

10 MAY, 2024

By Thomas Hempell from Generali Investments

Amid reaccelerating US inflation, markets have axed rate cut expectations for all major central banks. We expect the start of Fed easing to be postponed till September, but not cancelled. A first ECB rate cut remains due in June with at least quarterly cuts to follow thereafter.

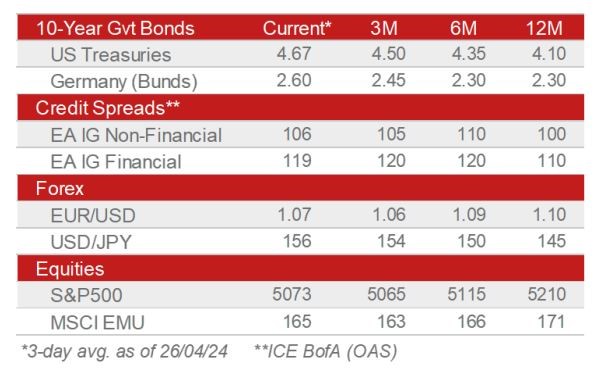

We acknowledge two-sided risk for yields near term, with a resilient US economy and stickier prices the most imminent risks. But with many bad inflation news now priced in, and 5-year forward 3-month rates near 4%, we see value in prudent long duration.

Amid the tug of war between high valuations and higher uncertainties on the one hand and global economic green shoots on the other, we keep an overexposure in IG Credit to reap the carry from risk premia. But we keep a neutral stance on Equities and High Yield amid elevated risks of further setbacks.

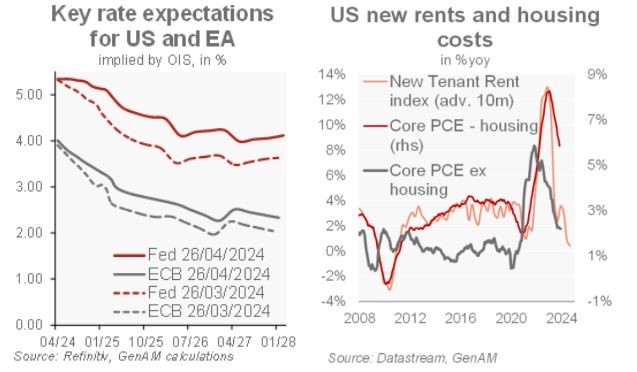

Investors seem to throw in the towel regarding rate cut hopes. Following solid US economic data and sticky inflation prints, markets are now pricing a full first Fed rate cut only for November and see the easing cycle ending above 4% (left chart), almost a full percentage point above levels we deem neutral. What is more, despite more encouraging disinflation progress in the euro area, markets also discount a striking ECB reluctance to lead the Fed in the easing cycle.

We have argued for some time that the last inflation mile would prove bumpy and that nearly seven cumulated 2024 rate Fed cuts, which markets priced around the turn of the year, reflected overblown optimism. Yet markets may be at the verge of turning overly pessimistic on that front now. Despite recent US inflation disappointment, quits rate points to moderating wage growth. After stripping out lagging housing costs, the Fed’s preferred core PCE is already close to target (2.2%yoy) – while new tenant rents clearly point to a moderation of housing costs (right chart). Goods may no longer be deflationary, but the ISM points to softer inflation in Services. The Fed will wait for more reassuring data after the recent bumpy readings and we now expect the first Fed rate cut in September, rather than July (though 3 monthly prints of CPI and core PCE are still due before the 31/7 meeting). We remain convinced that inflation prints will ultimately strengthen the case for a longer sequence of quarterly Fed rate cuts.

Fears that the ECB will shy away from policy easing ahead of the Fed seem overblown too. ECB officials have already telegraphed a June cut. And ECB doves are right to stress that a hesitant Fed will tighten financial conditions also in the euro area, owing to spillovers on bond markets. We are neither overly worried by the exchange rate, since it would require a big knock in the trade-weighted euro to materially alter the EA inflation outlook. With euro area disinflation still benign, we still have 75-100bp of ECB hikes in our book for this year.

Preference for IG Credit and prudently for duration

Easing inflation, prospective rate cuts and a soft landing of the US economy over the summer have been key reasons for why we have warmed up to moderately increase duration exposure. Global economic green shoots (including in the euro area) and bumpy US inflation prints keep the risks to yields two-sided in the short term, though, as evidenced in April. But we see 10-year US Treasury yields above 4.60% as a good entry level. A brighter economic outlook will keep corporate earnings underpinned, but geopolitical risks and valuations that still price a lot of cyclical optimism leave us neutral on riskier segments such as Equities and High Yields. Anticipating stable spreads on high-quality names amid green shoots in the euro area, we prefer EUR IG Credit financed by underweights in Cash and short-dated Government Bonds.