Fed meeting this week: what can we expect?

Updated:

9 DEC, 2025

By Joanna Piwko from RankiaPro Europe

The Fed’s December meeting takes place this week. The Federal Reserve is expected to cut rates, although this time experts differ on what the move will look like and what it will signal.

Here is the outlook for this week’s meeting from the experts:

Paolo Zanghieri, Senior Economist at Generali AM (part of Generali Investments)

The U.S. economy is largely driven by consumer spending (supported by wealth effects) and AI investment. We expect GDP to grow 2.0% next year as the non-tech component of capex catches up.

Despite a partial reversal by the administration on tariffs, these will continue contributing to inflation for some time. We expect core PCE to end this year slightly above 3%, and around 2.5% by late 2026.

We anticipate that the policy rate will be cut by another 50 basis points by the first quarter of 2026, significantly less than what the market expects.

The minutes of the October meeting showed that many members of the Federal Open Market Committee (FOMC) see no need for further cuts this year. The lack of solid data makes a commitment difficult. A rate cut in December followed by a final cut in the first quarter remains our base case, although with low confidence. It would be reasonable for the Fed to wait until January while signaling an accommodative bias.

Markets expect the policy rate to bottom at 3% next year. We consider this too accommodative given the persistent nature of inflation and project the terminal rate to settle in the 3.25%–3.5% range.

The U.S. economy shows two-speed growth

After the end of the government shutdown, the flow of economic data has resumed; however, critical information on October CPI and employment will not be available. Partial evidence indicates a two-speed economy:

- Consumption is increasingly concentrated among higher-income households, supported by strong wage dynamics and a significant wealth effect from equity markets. This boosts consumption, especially in services.

- Meanwhile, lower-income households are experiencing slower real income growth and greater vulnerability in certain segments of the labor market.

Job growth in September, although stronger than expected (119,000 new jobs), remains concentrated in leisure, hospitality, and acyclical sectors such as healthcare.

Business surveys confirm that, outside the tech sector, capital expenditure decisions remain cautious. After a weak fourth quarter, we expect the impact of tax cuts on consumption and investment to materialize at the turn of the year, ensuring solid 2% growth next year.

Strong demand for services will prevent rapid disinflation in that sector. The impact of tariffs—although smaller than anticipated, partly due to tariff reductions on agricultural products—will become increasingly noticeable.

Thus, we forecast that core PCE will end the year at around 3% year-on-year and remain clearly above 2% in the first half of next year.

Marco Giordano, Chief Investment Officer at Wellington Management

The President of the New York Fed, John Williams, indicated that he is open to a rate cut at the December FOMC meeting. In a speech delivered in Santiago, Chile, Williams stated: “I still see room for a further short-term adjustment to the target range for the federal funds rate, in order to bring the stance of monetary policy closer to the neutral range and thus maintain the balance between achieving our two objectives.”

He noted that downside risks to employment have increased, while upside risks to inflation have diminished, and described monetary policy as “modestly restrictive.” His comments significantly boosted market expectations for a December rate cut, which are now fully priced into futures markets.

The Committee remains divided ahead of the December meeting, but we believe that most members will lean toward bringing the policy rate closer to neutrality in order to pre-empt any further weakening in the labor market.

Martin Van Vliet, Global Macro Strategist at Robeco

Since May, we have anticipated that a weakening labor market would push the Fed to resume its monetary easing cycle, ultimately bringing monetary policy back to a neutral stance despite persistent inflation risks. So far, this scenario is unfolding as expected.

Of course, at the end of October, Chair Powell emphasized that another rate cut at the December meeting is “far from guaranteed”, while also noting that inflation risks remain tilted to the upside. However, Powell also remarked that monetary policy is still considered “moderately restrictive”, which in our view leaves the door open to further easing.

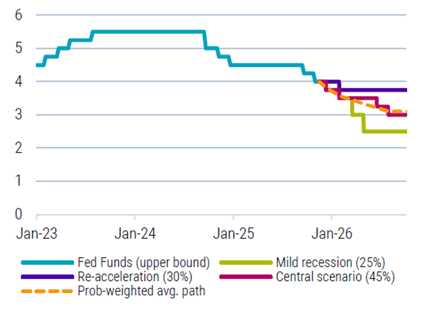

Therefore, even if the Fed were to pause in December, it is unlikely that the easing cycle has reached its end. Our base case continues to project a terminal policy rate between 2.75% and 3.00%. This level could be reached in the first half of 2026 if labor market conditions fail to improve, or later, after the new Fed Chair takes office in May 2026.

We assign a 25% probability to a recessionary scenario, which would justify more substantial rate cuts. Conversely, we also assign a 30% probability to a scenario where only limited further easing occurs if inflation proves more persistent and the economy regains momentum. Taking these scenarios into account, our probability-weighted forecast for the fed funds rate is slightly below what the market is currently pricing in.

Figure 2 – Three scenarios for the Fed through September 2026 (%)

Vontobel

Andrew Jackson, Chief Investment Officer and Head of the Fixed Income Boutique

Christopher Koslowski, Senior Investment Strategist

Gregor Kapferer, Head of Global and Swiss Bonds

Peter Zöllner, Senior Advisor

When central bank credibility weakens, markets stop interpreting its policies through the lens of economic data and begin viewing them through a political perspective. (…) Looking ahead, we outline three plausible scenarios, ranging from a mild erosion of Fed independence to full political interference. (…) Scenario 1: Pullback and reset, no further influence – Probability 10–20% In this scenario, market instability prompts the Fed to deliver a somewhat larger rate cut to restore stability. (…) With the Fed’s credibility in fighting inflation restored, long-term inflation expectations are likely to re-anchor near the 2% target. (…) Credit markets would likely breathe a sigh of relief under renewed Fed independence. (…) Scenario 2: Soft erosion (no legal change) – Probability 45–65% Although the Fed formally operates independently, policymakers occasionally opt for more dovish measures than the data alone would justify. (…) The yield curve steepens in this environment. (…) Scenario 3: Episodic interference – Probability 15–25% Political intervention affects Fed decisions intermittently but frequently enough to erode credibility. (…) Expectations become unanchored and investors price in greater inflation and policy-error risk. (…) Scenario 4: Open interference or legal change – Probability 2–5% The central bank’s independence is effectively nullified or severely compromised. (…) If the Fed caps long-term yields, nominal yields may be forcibly suppressed while pressure shows up in wider breakevens and a weaker dollar. (…) Gold and alternative assets would likely surge, and concerns over the Fed’s independence could further fuel gold demand.