How will the US election impact the markets?

6 MAY, 2024

By Jose Luis Palmer from RankiaPro Europe

The US elections are approaching, we are now less than six months away from the key date. As we approach the US elections and the candidates, Trump and Biden, begin to unveil their proposed economic and political agenda, markets are gradually reacting. The outcome of the Biden-Trump showdown will have an impact on the markets, given the differences in the economic proposals of the two candidates. Industry experts analyse what impact the election cycle and the most awaited election result in recent years will have on the market.

Do US elections influence the Fed's decisions?

Paolo Zanghieri, Senior Economist at Generali AM

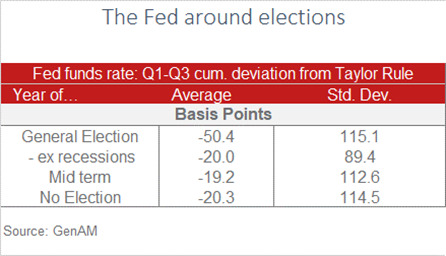

There are speculations that the Fed may refrain from cutting rates in order not to give the impression that it favours the incumbent candidate in the presidential election. We can safely rule out such a conjecture, based on both historical evidence and reasoning on the Fed mandate. We looked at the difference between the effective Fed rate and a benchmark given by a standard Taylor rule and considered the cumulative change between the first and third quarter of the election years against non-election years. The table below shows that the Fed appeared on average “softer” than the benchmark in general (Presidential and Congress) election years, but this result is heavily biased by the Great Financial Crisis (2008 election) and the Covid outbreak (2020). If those episodes are excluded, it becomes evident that the Fed does not behave differently in election years.

More conceptually, we think that the point made in 1992 by the then-President of the Dallas Fed McTeer remains valid. The common assumption is that the Fed is biased toward the incumbent, and therefore it would strive to either avoid a recession or (as in the current context) to make sure that inflation falls ahead of the election. It would then seek to quickly tame inflation and minimise the impact on unemployment, which is however fully consistent with its dual mandate. Therefore, Mc Teer concluded, the incentives of the Fed are aligned, with that of any incumbent President, and there is no reason to think that the electoral cycle may lead the Fed to deviate from its preferred policy stance.

However, the outcome of the election may matter a lot for the Fed in 2025, using the possible further deterioration of the federal balance. Both candidates have pledged measures that will further widen the deficit. Even discounting some propaganda and considering the possibility of a split in government (i.e., a Congress without a majority or ruled by a different party from the president’s), a further worsening of the fiscal outlook appears likely in 2025. The Trump-era tax cuts and the expanded subsidies for health insurance both expire at the end of 2025 so Republicans will have to rush to prevent the former, and Democrats the latter. Without a unique majority in Congress and at the White House, there is still scope for a deal that would add around $1tn to the federal deficit. Higher public debt adding to the already elevated private one will help move up the neutral rate, which is the main reason behind our forecast of a 2.9% nominal r-star, some 40 bps higher than those shown in the December dots. A new Trump presidency moreover brings the risk of sweeping trade tariffs, which are inflationary. It is not fully sure, however how the Fed would respond to that, as they would impact a negative supply shock, raising inflation while depressing activity.

The Trump vs Biden rematch: Markets implications of unprecedented policy divergence

Juhi Dhawan, Macro Strategist at Wellington Management

This year’s US presidential election will be closely contested, and I expect six key areas of policy debate to impact markets most: the federal deficit, tax and spending shifts, regulatory policy, immigration, trade, and geopolitics. I offer thoughts on each of these topics below but will begin with the bottom line: Investors should work with a much wider range of estimates on bond yields, growth, and inflation prospects for the US and be ready for a more radical shift in the trade and geopolitical landscape. They should also consider the possibility that equity markets may reward different sectors going forward, as earnings potential and valuations are impacted by these shifts.

Why do investors have so much to think about as the election process plays out in the coming months? Just consider the vast policy gulf between the two candidates and the potential economic impact. For example, in a scenario where former President Trump wins and is backed by a Republican-led Congress, I would expect to see lower taxes, higher deficits, higher inflation, higher yields, less regulation, and more isolationist trade and geopolitical policy. Or take the case of a win for President Biden but a still-divided Congress. I would expect that to yield higher taxes for higher income earners, contributing to some deficit reduction, but also a continuation of green energy subsidies that would limit fiscal prudence. And should President Biden win with a Democratic-led Congress, I would expect to see a somewhat higher corporate tax rate, an extension of the child tax credit, efforts to curb health care costs for consumers, and more money for areas such as education, low-income housing, and climate.

Before I get into the details of this policy divergence, let me spend a moment on the election math.

Key areas of economic and market impact

Let’s turn to the six policy areas that I think investors should be keeping track of in the coming months.

The federal deficit

For the candidates from both parties, as well as the American public, the size of the federal budget deficit is a low priority. This suggests that fiscal policy is unlikely to tighten meaningfully under either party unless markets (which do care about the deficit) force discipline. That said, a divided Congress would be more likely to limit the ability of either party to maneuver and, therefore, might help to contain the deficit.

Looking ahead, I think it is fair to say that Trump explicitly cares less about the size of the deficit and, as a result, financial markets would demand higher term premia for US bonds if he were to win and have the benefit of a Republican-led Congress. It’s worth noting that the deficit, which currently stands at about 6% of GDP, typically widens by about two percentage points in a recession, suggesting a significant potential vulnerability for the US economy and markets as far as the discount rate is concerned. I expect interest rates to rise in either election outcome, but I would be more concerned about rates if Trump wins.

Tax and spending shifts

The US economy faces a tax cliff at the end of 2025, when Trump’s 2017 tax cuts are set to expire. If no action is taken, this would raise taxes by $400 billion annually, with individual tax rates reverting to the higher 2017 levels, the standard deduction cut in half, the estate tax exemption reduced, and the 20% deduction for pass-through businesses disappearing, among other changes. Trump would like to make the tax cuts permanent (at a cost of $2.7 – $3 trillion over the next 10 years) and lower the corporate tax rate further. Biden would like to hike taxes on those with incomes above $400,000 but keep them low for the remaining taxpayers (at a cost of $1 – $2 trillion over the next 10 years). This is perhaps the most underrated policy decision the incoming government will face, and the increasing dysfunction in Congress suggests that the compromises that could be required on many tax issues will be difficult to achieve. Ultimately, the extent of any compromises will depend on the makeup of Congress and on the economic situation at the time, with the easiest solution likely being to limit the period for which the taxes are extended.

Another tax issue that will be up for debate in the coming election is the way multinational corporations pay taxes. In particular, will the US enact a global minimum corporate tax, as proposed by Treasury Secretary Janet Yellen, and if not, could other countries end up retaliating? These changes in tax law would have important implications for corporate profit growth in the US, in turn impacting future stock market returns.

On the spending side, Biden’s 2022 Inflation Reduction Act (IRA), which included the largest investment in climate and energy in US history, will, if it is allowed to proceed unchecked, end up costing almost $1 trillion or three times the initial estimate. Trump is of course far less interested in green energy subsidies, so if he wins, we could see subsidies curtailed in both the time period over which they are offered and the breadth of green energy sources that receive them. Electric vehicle tax credits are also likely to be on the chopping block. With 71% of projects announced under the IRA still in the planning stage, it is conceivable that some will be cancelled or delayed until election clarity emerges. Industrial company and green company earnings in the US have received a large boost from these subsidies and under a Biden administration would see a still strong path ahead. However, the runway for subsidies and the breadth of earnings lift could be curtailed under a change in administration.

Overall, the two candidates’ stances on taxes and their potentially unsustainable spending plans could add $1 – $5 trillion to the deficit and raise the risk of higher interest rates.

Regulatory policy

While fiscal and tax policy depend on both Congress and the president, the latter has a much bigger say on regulation. For instance, under President Biden, we have seen higher capital requirements for banks, more scrutiny on drug prices, and tougher EPA emissions standards. Trump would be more likely to deregulate industries and reduce what he considers onerous requirements on businesses. Trump would also like to bring independent regulatory agencies, such as the Federal Communications Commission and the Federal Trade Commission, under presidential authority. These shifts would have a notable impact on regulated sectors of the economy.

To offer one example of where Trump might cut regulatory red tape after taking office, he could reasonably be expected to modify or repeal the EPA’s planned 2027 emissions upgrade. With changes like this (and the possible green energy spending changes noted earlier), a Trump administration would slow the pace of the country’s green energy transition and maintain a somewhat greater reliance on fossil fuels.

Immigration

From an economic standpoint, this is another underappreciated election issue. The cost of dealing with undocumented immigrants is admittedly a challenge for border states, and in some polls, immigration is now the number one issue, surpassing inflation. But the ongoing surge in immigration — which will add some seven million people to the US population by 2026, according to the latest estimates from the Congressional Budget Office — has provided a positive supply-side shock for the economy that has helped reduce wage pressure and contributed to better balance in the labor market. While many immigrants being counted in the labor force today are legal, thanks to a catch-up in the visa backlog, the surge in undocumented immigrants has been a factor. Trump has vowed to enforce border control more effectively but has also promised to deport undocumented workers, which would be a significant negative labor supply shock and would be inflationary.

Trade initiatives

If Trump wins the election, it is widely expected he will raise tariffs, perhaps by as much as 10% across the board and as much as 60% for imports from China. Estimates suggests that a universal baseline tariff could raise $1 trillion over 10 years, which would help fund some of Trump’s tax plans. On the other hand, higher tariffs will add to inflationary pressure and hurt consumer purchasing power.

In other areas of trade, Trump could use the joint review of the United States-Mexico-Canada Agreement (USMCA) scheduled for 2026 to implement shifts in policy relating to Mexico. Relationships with Europe and Japan are also likely to be less cordial than under a Biden administration.

If Biden is reelected, trade policy will likely continue on its current path, with decoupling from China remaining a priority but Europe and Japan considered strong allies.

Geopolitics

The reshaping of the geopolitical map is a given should Trump return to power. Withdrawal from NATO and an increase in defense spending by Europe, the US, and possibly Japan are all potential spillovers. Energy security would be an important policy pillar for a Biden or Trump administration, but would manifest itself differently, from large green energy subsidies and curbs on natural gas exports under Biden to higher fossil fuel production and exports under Trump. Decoupling from China would remain an imperative in either election scenario, but Trump prefers tariffs to subsidies, so the substance of US industrial policy would shift accordingly.