Ignore the ‘sell in May’ adage

11 MAY, 2023

By Julius Bär

There are plenty of reasons to exercise caution right now. The name of the month is not one of them. Rather than using seasonality as a guide, investors should weigh up the expected rewards and risks of each asset on its own merit. In this Research Weekly, our experts also indicate why strong US labour data is likely to stall rate cuts, and highlight Switzerland as a safe haven for investors seeking stability.

As in every May, the ‘sell in May’ adage has set in. It is surprising that investors are so stubborn about seasonality, especially when they do not give it such serious consideration in other aspects of their lives. For example, using seasonality as a guide would mean not organising outdoor parties in Europe during the summer given that it is the season with the heaviest rainfall. Yet, rather than missing out on the warm summer nights, we simply put in place a ‘plan b’ for possible thunderstorms. When it comes to investing, however, a similar approach seems to be out of the question for the average investor.

The May custom may lead to some fluctuations on the stock markets in the weeks ahead. However, there are even better reasons to exercise caution right now; geopolitics is one of them, with the war in Ukraine and tensions around Taiwan, as well as the unpredictable debt ceiling gamble in the US. The crisis in US regional banking may also continue to hit the headlines.

Our task is to judge whether it is worth holding a financial asset given the expected rewards and risks attached. The good news is that there are plenty of expected rewards compared to the risks mentioned above. The even better news is that now you do not have to take excessive risks. Holding quality should pay off all by itself. In this context, we have further de-risked our credit portfolio by downgrading eurozone high-yield bonds.

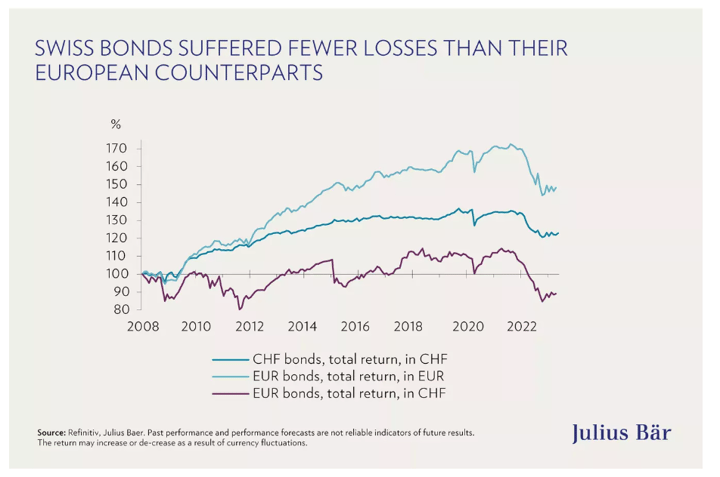

Switzerland: a ‘safe haven’ for bond investors

As the global bond market experiences volatility and fiscal uncertainty, Switzerland is a compelling option for investors. Switzerland is known for its disciplined fiscal policy and low inflation rates. The country’s robust financial sector and high credit ratings further showcase Switzerland as an ideal and strategic investment choice that effectively decreases the overall risk profile while providing diversification options.

Another positive factor for the Swiss bond market is the strength of its currency, as the Swiss National Bank declared its intention to contain any unwarranted weakening of the Swiss Franc last year. In our view, this heralds more Swiss franc strength in the medium term, making Swiss bonds an increasingly attractive option. Although the security associated with investing in Switzerland comes with a price, we thus recommend the Swiss debt market as a viable portfolio diversification strategy.

Amid the backdrop of the global bond market suffering volatility and fiscal uncertainty, this chart shows that Switzerland may be a compelling option for investors.

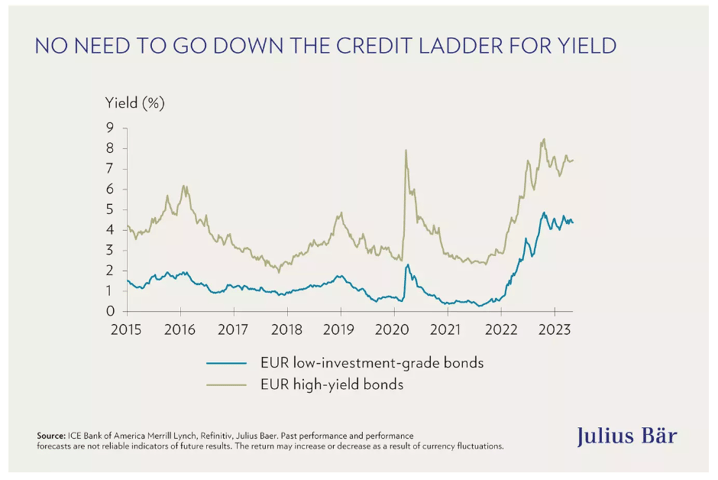

Fixed income: EUR high-yield downgraded to Underweight

Following our downgrade of the USD high-yield segment last month, we have now added the EUR high-yield segment to our least-preferred list and continue with our strategy of de-risking credit portfolios. Credit dynamics in developed markets are weakening fast, warranting a more cautious stance on credit risk overall. Thus, we have downgraded the EUR high-yield segment to Underweight and favour corporate EUR low-investment-grade debt at this juncture.

This chart outlines the yield data of EUR low-investment-grade bonds and EUR high-yield bonds.

Resilient labour market data likely to keep Fed on hold

Last Friday’s April US employment report showed a drop in the unemployment rate to 3.4% and strong growth of average hourly earnings rounded off a solid set of labour market data. With markets having already priced in three rate cuts by the end of the year, this robust labour market data is likely to postpone expectations for the first rate cut. We still expect the tighter monetary policy to impact economic growth meaningfully later this year. We stick to our view that the Fed has completed its tightening cycle at the current federal funds target range of 5%–5.25% and expect the first rate cut in December, when higher rates will weigh on the economy.