Monetarist avengers (try to) assemble

17 FEB, 2023

By RankiaPro Europe

By Gilles Moëc, Chief Economist at AXA IM.

A sense of theoretical deja-vu is a side-effect of spending three decades in the economist profession. Dominant paradigms come, go, and return, leaving your humble servant often sceptical about their universal explanatory power. Monetarism, considered for more than two decades as a historically interesting object with limited practical use, is attempting a comeback. Martin Wolf in the Financial Times has written a very interesting piece last week on some attempts to resurrect the Old Faith. Our contention, however, is that, as always, looking at the gyrations in money supply is going to be useful to understand the recent past, while being of poor use to try to predict the near future.

One paper mentioned by Wolf is by Claudio Borio, from the Bank of International Settlements. He matters. He came up with one of the most interesting breakthroughs in monetary policy decision-making by spotting how, in a globalized economy, capacity utilization across the world may matter more for inflation in any particular country than domestic conditions. It may sound obvious now, but just like every great intellectual innovation, someone had to spot it and articulate it. So, when Claudio Borio decides to look at excess money growth in its relationship with inflation in our current configuration, you know it’s time to dust off your Friedman and make sure you know your M1 from your M2.

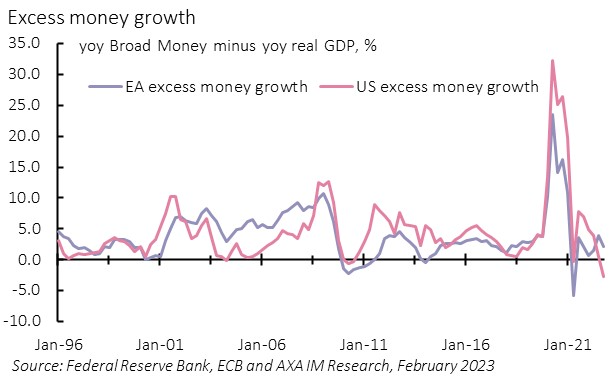

Borio’s starting point is that money supply may not usually matter much, but it becomes interesting in times of high inflation. He substantiates this empirically by looking at the correlation across around 30 developed and emerging countries between excess money growth (the difference between the change in a broad money aggregate and the change in real GDP) and inflation for various inflation regimes. The relationship becomes tighter the higher inflation is. This is key. This would suggest that once inflation had been tamed in the 1980s in all developed economies, to move within a tight “tube” around 2%, there was little point in looking at money aggregates for guidance. Of course, we are now in one of those “high regime” situations, combining, in response to the pandemic, a massive acceleration in money supply followed by the ongoing inflation spike (see Exhibit 1). Borio shows, looking at vintages of economists’ forecasts of inflation, that the under-prediction errors of the current pace of inflation were the largest in countries which had experienced the largest rise in excess money growth, suggesting that adding measures of the money stock in models would have improved the quality of the forecasts.

Exhibit 1: Unusual gyrations in excess money since the pandemic

What we also find interesting in Borio’s paper is that he “follows the trail” and sets out to explain the various mechanisms through which this combination of excess money growth and inflation has just re-emerged. In principle, a fiscal stimulus does not trigger a rise in money supply, at least not directly. To transfer cash to non-financial agents, the Treasury issues debt, which forces investors to swap cash for securities (they change their asset allocation, but their total asset/liabilities don’t rise). This changes when debt issuance is funded by the central bank, crediting the government’s cash account with new money as they purchase the bonds (its assets and liabilities both rise). What we experienced during the pandemic was one of the purest historical examples of fiscal reflation. Inflation is then not the product of a rise in money creation by some “magic trick” but results at least partly from the fact that the fiscal push permitted by more quantitative easing drove the economy in a situation of excess aggregate demand – in a context of depleted supply at the time of the lockdown.

That helps to understand the recent past. The question is whether the current and expected path for money supply will add much information to predicting inflation in 2023 and 2024. The “fiscal reflation” mechanism we described above was exogenous. It was the product of a policy decision, by both governments and the central banks (it may have also taken the form of emergency bank loans to corporations, but as the response to a government incentive, not under as a result of a spontaneous behaviour by banks). But there can also be an endogenous phenomenon – the normal operation of money creation via bank credit without government intervention. Borio raises the question of the transition from one regime to another but does not explore it. This is where we think the endogenous/exogenous distinction can be operative. The high money creation/high inflation regime could become permanent if credit issuance were to build upon the initial signal from QE to perpetuate excess demand and excess money growth. Note that this failed to happen in the previous decade. For instance, there was no visible acceleration in excess money growth in the Euro area after the ECB finally opted for QE in 2015 (its pace remained below the pre-2008 trend), since the endogenous engine of money creation – credit – was weak enough to offset the mechanical impact of the bond purchases by the central bank (the softness in credit was precisely one of the reasons which drove the ECB into this extra step of extraordinary measures).

What are the risks this happens in our current configuration? It’s already questionable if money growth is still excessive. In the US, broad money is already growing slower than real GDP (hence the line falling into negative territory in the last part of Exhibit 1) while excess money growth stands at only about 2% in the Euro area, which looks small relative to inflation. We discussed last week how the tightening in bank lending standards was triggering a sharp fall in the Euro area’s credit impulse. Banks are not “prolonging” the effect of QE, which obviously is now being replaced by Quantitative Tightening, on both sides of the Atlantic.

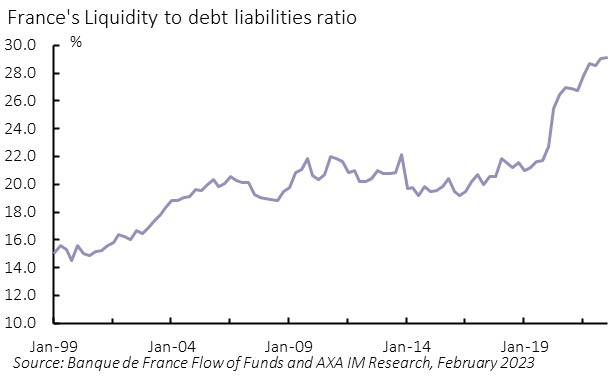

Moreover, a nagging issue in the inflation/money stock relationship is the velocity of money – how many transactions are executed with the same unit of money in a given time. As long as central banks’ digital currencies do not dominate, velocity cannot be directly tracked. Instead, it can be obtained at the macro level by dividing GDP – nominal this time, representative of the number of transactions at the given price level – by money supply. Velocity crashed during the pandemic, as the lockdowns paralysed cash holdings. A lot of the money creation of that period ended up sitting idle on current accounts. This is well known for households, but it’s true for businesses as well. This explains why their liquidity ratio – liquid assets, such as cash accounts and instant access savings, as a percentage of debt liabilities - has in general improved. In the US, firms have started to draw on their liquidity, but the ratio remains historically high. In France, which has the most leveraged corporate sector among the major Euro area economies, the liquidity ratio in the business sector has hit a historical peak (see Exhibit 2 and 3).

Exhibit 2: US firms have not yet spent all their liquidity buffers

Exhibit 3: French firms still cash-rich by historical standards

So, what do we know at this stage? We know that money supply has started to fall, thanks to the termination of QE, leaving way to Quantitative Tightening, and the new lending stance of commercial banks. This would suggest that, from a monetarist point of view, the risk of settling into a permanent high inflation scenario is low. Yet, there remains a question mark: what non-financial agents decide to do with their accumulated liquid assets in the near future. The existence of these buffers – bigger in the Euro area than in the US – could well impair the transmission of monetary policy: businesses can cope better and longer than usual to a restriction of credit. But we knew that already, without having to resort to monetarist mechanisms. It’s just another way to think about the absorption of the excess savings accumulated during the pandemic, a major theme of cyclical analysis since the middle of last year.

These considerations get us back to the sources of the demise of monetarism in the late 1980s/early 1990s: monetary aggregates do not provide precise enough indications for the actual conduct of monetary policy. Borios’s correlations were run over samples of 10 years, starting as early as 1951. Using shorter timespans, e.g., the 2-3 years ahead which is today the common “policy-relevant” horizon of central banks, the correlation would fall drastically. This helps explain why, from a practical point of view, targeting, or even following, monetary aggregates has fallen out of favour in the 1990s. All we know is that “at some point” the effect of money supply on inflation may materialise – although, as Borio makes a big point of stating, causality is not proved – but we can’t know when, or to which degree.

Related articles

Granolas Stocks: what they are and differences with the Magnificent 7

Granolas Stocks: what they are and differences with the Magnificent 7By RankiaPro Europe