‘Sell in May and Go Away’: A Balanced Perspective

By: Ernst Knacke, Head of Research, LeifBridge and Shard Capital

As investors gear up for the seasonal transition into the summer months, the recurring question arises: Should one adhere to the time-tested adage of "Sell in May and Go Away"? While this strategy has garnered attention for its historical trends, we believe it is imperative to approach it with a balanced perspective. Whilst acknowledging its potential efficacy, investors should recognise that market dynamics are multifaceted and influenced by a myriad of factors beyond seasonal patterns alone.

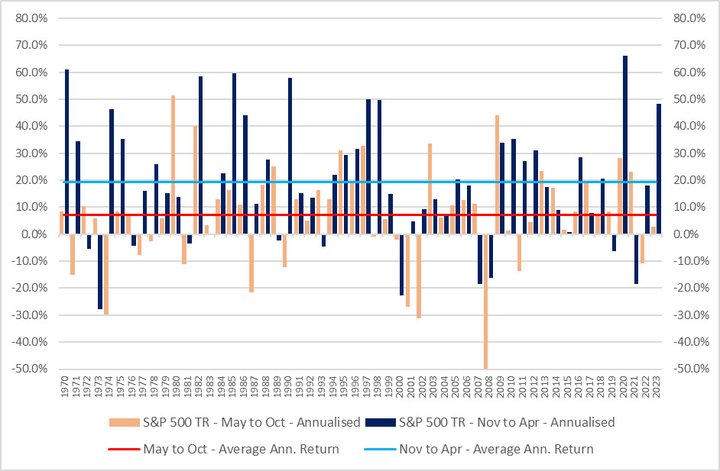

However, as the chart and tables below highlight, the historical evidence is rather conclusive. Since 1970, the average annual return of the S&P 500 between May and October has been approximately 7.2%, while investing capital at the end of October and holding until the following April has yielded a total return of over 19%. A remarkably large difference. The FTSE 100 in the UK yields surprising similar results following this very basic approach.

Whilst the "Sell in May" approach might offer a tactical advantage in certain market conditions, it's essential to exercise caution and avoid an over-reliance on historical precedents. Market environments evolve, and past performance is not an infallible predictor of future outcomes. Indeed, there is conclusive evidence that cognitive biases often pose significant barriers and lead to losses for many investors. Investors should supplement seasonal considerations with comprehensive fundamental analysis in order to make more informed decisions. Furthermore, prudent risk management is paramount, particularly with market-timing strategies like "Sell in May." While seasonal patterns present potential benefits, they also entail substantial risks.

Ultimately, the best investors through history did not ‘time’ the market. They spent time in the market. There is no replacement for high-quality, independent research, a robust and repeatable process, the insistence of a margin of safety, and patience. We believe in the alternative maxim “it is time in the market, rather than timing the market”.

A fundamental valuation-based analysis provides a robust framework for evaluating investment opportunities, offering insights into the intrinsic value of assets. By scrutinising valuation metrics and growth prospects, investors can assess the underlying fundamentals driving stock prices, irrespective of seasonal fluctuations. Investors should navigate the nuances of seasonal trends with more diligence and prudence, better and more informed research, a repeatable decision-making framework, and robust risk management, which collectively, might just support better outcomes in their investment endeavours.

Chart 1: Annualised returns for the S&P 500 between May and October vs annualised returns between November and April, since 1970:

| S&P 500 TR - May to Oct Annualised | S&P 500 TR - Nov to Apr Annualised | |

| Average Annual Return | 7.2% | 19.3% |

| Annualised Volatility / Standard Deviation | 19.0% | 22.7% |

| FTSE 100 TR - May to Oct Annualised | FTSE 100 TR - Nov to Apr Annualised | |

| Average Annual Return | 7.5% | 18.2% |

| Annualised Volatility / Standard Deviation | 19.0% | 21.3% |