Technology Investment Megatrends to Keep on the Radar

2 MAY, 2024

By Jose Luis Palmer from RankiaPro Europe

In the ever-evolving landscape of technology investments, staying ahead of the curve is paramount. As the digital age continues to redefine industries and reshape economies, identifying the key megatrends driving these transformations becomes essential for investors seeking sustainable growth. In this multi-voice article, we bring together insights from technological funds' portfolio managers. Experts from the industry shed light on the technology investment megatrends that warrant attention in the coming years. Join us as we navigate the dynamic terrain of technological innovation and investment opportunities.

AI: the next major compute wave

Richard Clode, Portfolio Manager on the Global Technology Leaders Team at Janus Henderson

The technology sector is embarking on the next major compute wave in AI. Each compute wave has been larger and more disruptive than the last and the sector is now anticipating the share gains of the economy driven by AI that will allow the tech sector to driver superior earnings growth for many years to come and create the new FAANG. We believe we are still very early innings in the innovation and disruption AI will deliver.

The Magnificent 7 was a false construct of a group of companies that have nothing in common in terms of AI positioning, valuation, growth, China exposure or regulation. It is a good example of why we think it is so important to be active managers in such a dynamic sector as technology. Major technology inflections have historically been a great time to be active given benchmarks are backward looking rewarding past success. That works when there are established winners in an existing trend but not at inflection points.

Another major change in the market has been the return of the cost of capital and that is resulting in a return to fundamental investing and more dispersion. That is evident in the return dispersion of the Magnificent 7 and again favours active, bottom-up stock pickers. Companies need to be profitable and on a reasonable valuation in this new market environment.

There are small caps like Impinj that dominate a more niche technology like RFID, mid-caps like Pure Storage that benefit from AI infrastructure requiring faster, lower power storage and also non-AI large caps like Uber and MercadoLibre. The unifying factor is all these companies are leaders in their field and are delivering significant profitability ramps that justify their share price appreciation.

New technology waves tend to be led by the US and often the US technology company is actually cheaper than its global peer given more choice versus the scarcity premium investors put on the rare AI stock in other markets. But there are still opportunities in Europe, for example on Besi and ASML who are key AI beneficiaries. However, that AI scarcity premium has made European leaders in this area challenging from a valuation point of view.

Undervalued Megacaps still exist

HyunHo Sohn, Portfolio Manager of Fidelity Funds Global Technology Fund

I don’t invest in so-called hot AI stocks because names that are big today may not be the winners of tomorrow. So, how am I currently playing the AI theme? Firstly, there are many indirect beneficiaries, or diversified businesses, where the benefits of AI may not be immediately obvious to investors. These include semiconductor foundries, packaging technology companies and memory companies. I am also looking closely at enablers in the software and services sector. Unlike consumers who can adopt new technology very quickly, adoption among businesses is much slower. This is where these companies can help, in areas such data, integration and governance services.

Mega cap stocks in general are well researched and richly valued. However, within the mega caps, I believe there are some stocks that are still underappreciated. For example, Amazon has a strong runway for growth in retail, long-term profit margin improvement potential and its cloud computing business will benefit from continued cloud migration of its customers. Alphabet is another stock which is relatively under-priced as there is some concern about its search business model in an AI era. However, we believe its position as a consumer internet platform remains relatively strong given its technology leadership and data advantage.

More generally, I believe tech valuations look stretched. There is huge polarisation, with some AI stocks showing signs of dot com bubble excesses. I am also a little concerned about earnings quality deterioration in cases where there is a lot of historical stock-based compensation (such as some US software businesses). In a tighter liquidity environment, earnings quality becomes an important differentiator and cannot be ignored. The other area of opportunity is in selected China technology stocks.

Within my portfolio, I have payment technology companies which are a critical building block in e-commerce. I am also looking at digitisation leaders and enablers in the manufacturing, industrial and construction sectors, where technology is still very under-penetrated. Design software companies have a significant role to play in the long term. Another area is video gaming which is essentially interactive media entertainment with a highly engaged customer base and is a highly monetisable business. I also see music as an under monetised asset. Whether this is music IP owners or digital streaming platforms, these companies have a long runway when it comes to improving monetisation.

Data Centers of the Future: The Rise of Liquid Cooling

Yan Taw (YT) Boon, Head of Thematic- Asia at Neuberger Berman

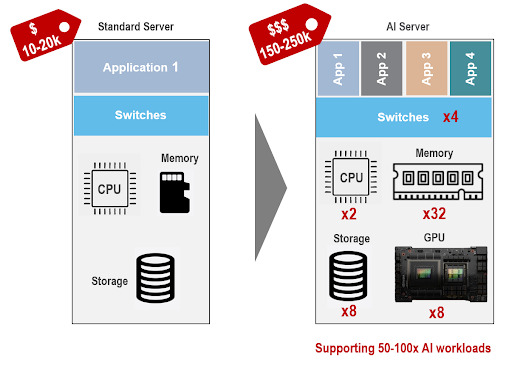

The ‘AI in everything’ trend is gaining significant momentum, as big tech investors globally pour hundreds of billions of dollars into the semiconductor industry, in a bid to gain a competitive advantage in the artificial intelligence race. Increasingly more powerful AI models are demanding record levels of computing power, putting pressure on the semiconductor industry to push the limits of physics and their customer’s wallets. Today’s AI servers are already able to support 50 – 100x the AI workloads of their standard counterparts, thanks to advances in semiconductors and packaging. These developments have come at a cost, with AI servers 10x more expensive than servers designed for serial processing (see Figure 1). And the increase in dollar content is expected to grow exponentially, with AI servers incorporating NVIDIA’s latest chip, the Blackwell B200 GPU, likely to fetch a price of 10x that of current AI servers.

Figure 1: The evolution of the server

The insatiable appetite for power is not just limited to AI models - running the servers that process them is incredibly energy intensive. With the increase in compute demand and further advancements in chip technology, power consumption by AI data centres is expected to increase by 10x between 2023 and 2026. While there is some concern about whether we will be able to supply this increase in energy, the biggest immediate challenge facing data centers is how to prevent them from overheating.

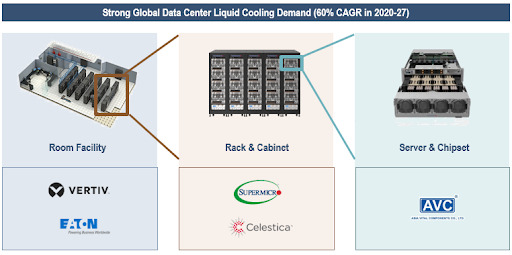

Consumption of such vast amounts of electricity is demanding new thermal management solutions, as record levels of heat in data centers tests the limit of traditional fan cooling. A new solution, liquid cooling, is rapidly being adopted by leading AI data center operators. There are many thousands of chips within each data center, and because of the massive amount of heat being generated right down to the chip level, these new cooling systems have to be designed from the bottom up. Starting with the chips, then the racks and cabinets, and finally the facility itself. The challenge for many existing data centers is that they were not designed to house the complex piping systems required to pump water around them.

The demand for liquid cooling is providing new opportunities for many companies, some of which have yet to benefit from the AI tailwinds sweeping across the technology sector. A number of Industrial companies like Vertiv and Eaton in the US are helping to retrofit data centers with these liquid cooling systems. US company Supermicro is working with customers to design and implement the latest liquid cooling technologies at the rack level. And Taiwanese leader, Asia Vital Components, has important partnerships with the likes of Nvidia to develop ‘cold plates’ to provide liquid cooling at the chip level (see Figure 2). Strong leadership positions combined with the massive amounts of investment being made in AI data centers means that many of these companies also benefit from very strong pricing power, and this is starting to be reflected in the latest earnings reports.

Figure 2: The latest thermal management solutions for data centers

Are breakthroughs in AI fuelled by hype? Are investors on time?

Polar Capital Global Technology Team

Ben Rogoff, Polar Capital Global Technology Team.

For us, generative AI represents one of the most exciting technological breakthroughs we’ve seen and could well be more important than the advent of the internet or cloud computing. However, we have not yet experienced the same overexuberance as seen in previous hype-driven cycles. Instead, valuations of key AI stocks have generally been backed up by robust earnings growth, while investors have been relatively selective rather than boosting the share prices of all firms riding on the sector’s popularity.

Moreover, there is a difference between so-called hype and genuinely backing a transformative technology. Just as the Bessemer process in the nineteenth century created an inexpensive way to mass produce steel, leading to the creation of myriad new industries, there is no telling what AI will facilitate from here. However, we are confident that the opportunity is vast given that AI is able to automate 25% of human tasks today with the potential to impact as many as 300m jobs globally.

Nick Evans, Polar Capital Global Technology Team.

Once it became clear that AI capability had begun to inflect, we introduced what we call an “AI lens” to our investment process. This means we now consider how AI impacts every business in each portfolio and whether stocks are enablers or beneficiaries of AI. This raises the bar for investment ideas that do not fit into that framework, because of our conviction that AI is the next big trend in technology. However, not all AI was born equal; there is obviously older machine learning (ML) for instance, meanwhile many companies will claim to be evaluating or deploying generative AI, but understanding where it can be utilised most effectively will be important. It is our job to sift through all of that and identify the real opportunities. Based on our definition of AI, 80% of the Polar Capital Global Technology Fund is now invested in companies that we believe are beneficiaries from or enablers of AI. While our remaining positions have exposure to other exciting (non-AI) technology themes, we are hopeful that none are losers from AI, or we would have exited them.

Xuesong Zhao, Fund Manager of the Polar Capital Artificial Intelligence Fund

I would paraphrase the old adage and say, “The best time to invest in AI was many years ago, the second best time may very well be today.” Very simply, we do not think investors have missed the AI boat. While there have been strong returns in some of the highest profile AI enablers, we think these moves have largely been supported by fundamentals, with many stocks still reasonably valued. In addition, we expect a broadening of the AI halo effect, as investors see robust demand benefitting a wide range of infrastructure stocks (the “enablers”). As we get further into 2024 and into 2025 we also expect to see a growing impact of AI led productivity gains and transformative change beyond the technology sector (the “beneficiaries”).

We are not saying the path is going to be smooth, there will of course be periods of volatility along the way, but the pace of innovation is such that we expect to see a bright future for AI as well as the opportunity for second-order themes in due course. One of the big benefits of AI is that it offers significant productivity gains, which could support a period of sustained non-inflationary growth leading to a stronger economic outlook than many believe is possible today. Importantly, we also expect to new commercial opportunities enabled by AI – just as the advent of the iPhone led to the huge global app economy today, something that few foresaw at the time.

A use case: Ai's role in drug discovery

On average, it takes at least 10 years to bring a drug from discovery to market at a cost of more than $2.5bn, with a failure rate of >90%; improvements to any part of that equation bring huge social and economic value.

Artificial Intelligence (AI) holds the promise of dramatically altering the speed and efficiency of drug development by allowing biopharmaceuticals to fail faster and earlier, or through improving the quality of drug candidates. The seminal success of the AlphaFold models in predicting protein folding and more recent success with healthcare-related transformer models such as Alphabet’s Med-PaLM, and NVIDIA’s GatorTron and BioNeMo, has triggered much greater buy-in from established biopharmaceutical companies and a wave of AI-based partnerships.

Studies suggest AI could yield time and cost savings of at least 25-50% in drug discovery up to the preclinical stage and large pharmaceutical companies have been signing collaborations and partnerships that focus on AI-enabled drug discovery at an increasing rate – the total value of these deals could already be up to $41bn. These deals typically combine a low upfront component of payment to the AI drug discovery company, and then much larger value on the realisation of success at various points, with milestone payments and royalty agreements upon commercialisation. This means they are a relatively derisked way for established biopharmaceutical firms to opt into the potential of AI.