Which asset classes should be most likely to benefit from lower rates?

27 MAR, 2024

By François Rimeu from La Française

Since the beginning of the year, there has been a repricing of the short end of the yield curve. Markets are now eagerly awaiting communication by major central banks as per the timing of the first rate cuts, which should begin in June. That being said, while June may be good in terms of timing, nothing is set in stone.

Central Banks continue to emphasize that their future decisions will depend on economic data and that they still need to be reassured about the future of inflation in general and wage inflation in particular. For the European Central Bank (ECB), European data will therefore be paramount but not only. US data will be equally important as the ECB appears reluctant to start a rate cutting cycle independently of the Federal Reserve (Fed).

This lack of confidence on the part of central banks is reflected in the volatility of rates, which are still very high even if they are falling, and is also reflected in investors' expectations. The option market indicates that while June is indeed the most likely date to begin to cut rates, there is still a wide dispersion of opinion. (Market Probability Tracker - Federal Reserve Bank of Atlanta (atlantafed.org)).

It is therefore important for certain types of investors, including asset managers, to see the rate cut cycle actually begin in order to be reassured about the direction of future investments and asset allocations.

Which equity markets could benefit from rate cuts?

With regard to equity markets, we believe that certain sectors which have suffered particularly since the beginning of rate hikes in 2022 could benefit from the coming rate cuts:

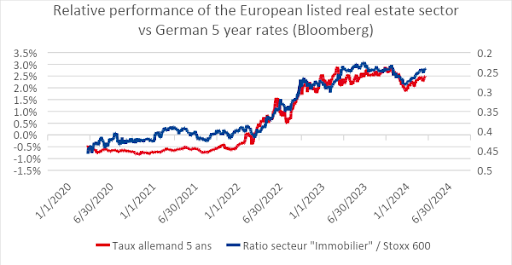

Listed European Real Estate

With a drop of 37% over the period from 5 January 2022 to 19 March 2024, while the index (Stoxx 600) was advancing marginally, the listed European real estate sector is probably the one that has suffered the most from the rise in bond yields. The chart below illustrates the sector's correlation to interest rate movements. For the sector, it is critical to witness the start of interest rate normalization as well as a decline in long-term rates. The terminal rate is now around 2.60% (EUR 5y5y swap rate) in the Eurozone. A return to 1.5-2% (what we consider as ‘neutral’ in the Eurozone) would be necessary in the medium term for the sector to outperform the market. As an asset manager, we believe this is a possibility, even if the moves are not linear.

Utilities

There has also been a notable underperformance since early 2022, with a decline of 10% over the same period as mentioned above; a logical decline for a sector with steady revenues. Beyond the disruptions linked to the war between Russia and Ukraine, the sector could benefit from the drop in future rates if the latter is the result of a decline in inflation risk.

Food and beverages

The sector was impacted by rising rates as well as weather events and the war in Ukraine. The underperformance was significant with an 18% fall over the same period. Given the sector's weak growth and historically high and stable dividends, this sector will probably benefit from a fall in long rates. However, rising rates are not the only factor behind its underperformance (for example, higher gas prices and fertilizer prices). Rate cuts from October to December 2023, for example, failed to lift market optimism, on the contrary.

Technology and healthcare

These sectors have not suffered from the rise in rates and paradoxically even stand to benefit! Often characterized as long duration sectors, technology and healthcare have benefited from the Covid crisis and the boom in artificial intelligence, attracting investments and generating profits. Valuations may be somewhat higher than elsewhere, but we see no reason why these companies would not also benefit from a future rate cut.

How will bond markets react to rate cuts?

Concerning Bond markets, everything will depend on why interest rates fall. If rates fall because inflation is declining, then the broader bond market should benefit from policy normalization. If rates, on the other hand, fall because the economy weakens significantly, then we are likely to see a widening of spreads (the difference in interest rates between a bond and a risk-free bond), which will obviously be negative for corporate bonds and especially for high yield bonds.

Conclusion

To sum up, monetary policy normalization is likely to be positive for commodities due to its positive impact on the economy. This will be even more true if the beginning of the economic recovery, which seems to be taking place in the eurozone, proves to be sustainable, as we believe will be the case.