Why China cannot be ignored when investing in batteries

15 NOV, 2023

By Mobeen Tahir from WisdomTree

In the fast-evolving landscape of battery technology, one historic fact that underscores China's

undeniable significance is the remarkable rise of Contemporary Amperex Technology Co. Limited

(CATL). What began as a modest venture in 2011 has transformed into a powerhouse, solidifying

China's pivotal role in the global battery market. CATL's ascendancy reflects not only its relentless

innovation and cutting-edge technology but also the country's strategic focus on becoming an

indispensable player in the world of batteries.

This meteoric journey from obscurity to dominance exemplifies why China's presence cannot be

ignored when making investment decisions in the battery industry.

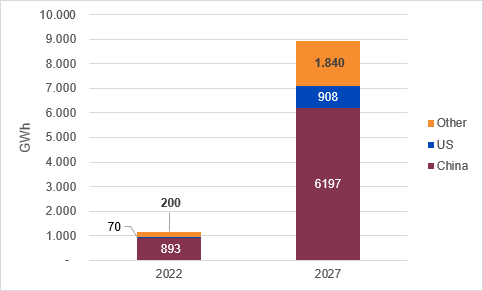

China’s market share

In 2022, China accounted for 77% of the world’s lithium-ion battery production capacity. Between

2022 and 2027, this production capacity is expected to rise from 1,163 gigawatt-hours (GWh) to

8,945 GWh, an eightfold increase in merely five years. And, although several countries including the US are expected to contribute to this capacity expansion, China is likely to maintain a dominant

market share of 69% in 2027.

Figure 1: China’s dominance in battery manufacturing 2022-2027

Source: Bloomberg New Energy Finance (BNEF) as illustrated by Visual Capitalist, January 2023.

China’s dominance is not just limited to battery manufacturing but extends to other links in the

chain including raw materials like battery-grade lithium, and battery components like electrolytes,

separators, cathodes, and anodes.

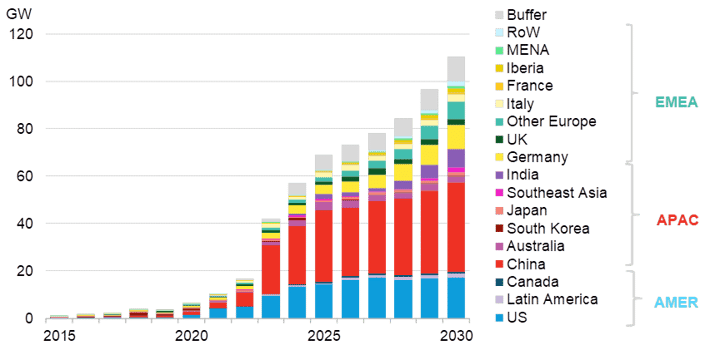

The energy storage market

Trends in energy storage can almost be used as a proxy for a country or region’s focus on renewable energy. According to Bloomberg New Energy Finance (BNEF), China’s top-down compulsory requirement to pair storage with utility-scale wind and solar is contributing to the notable expansion in China’s storage capacity which, in 2023, is expected to witness a notable uptick (see Figure 2).

Figure 2: Global gross energy storage capacity additions by key market

Source: BloombergNEF, as of 03 October 2023.

The electric vehicle battery market

According to consultants Wood Mackenzie, who partner with WisdomTree on the theme of battery

solutions, total energy storage demand from electric vehicles (EVs) over the next three decades is

expected to tower above other sources of demand. Based on their 2023 forecasts, battery storage

demand from electric vehicles could rise from 870GWh in 2023 to over 6000GWh by 2050.

It, therefore, makes a lot of sense to consider the state of global EV battery manufacturers when

determining the importance of any country in the battery market. According to Blackridge Research, 6 out of the top 10 EV battery manufacturers worldwide are from China. This includes names like Contemporary Amperex Technology Ltd (CATL), BYD, China Aviation Lithium Battery Ltd (CALB), and Farasis Energy, among others 2 .

CATL is a familiar name to most people around the world. One notable innovation from this battery

manufacturing behemoth was the launch of a battery swap solution EVOGO in 2022. The technology is comprised of battery blocks, fast battery swap stations, and an app. EVOGO is meant to be suitable for all types of vehicles including passenger cars and commercial vehicles and is designed to reduce range anxiety as well as upfront costs of vehicle ownership. At WisdomTree, we believe battery swapping is an exciting emerging technology that can complement other advances in battery manufacturing and could work well for public transport like buses as well as cars when they are used as taxis or rentals.

One of the biggest obstacles for battery swapping technology has been replacing large and heavy

batteries. CATL’s EVOGO solution is ideal as it is designed with modular blocks allowing individual

blocks to be replaced quickly and easily.

BYD (short for ‘Build Your Dreams’), is another company that is capturing people’s attention around

the world. It certainly did for Warren Buffet’s Berkshire Hathaway which bought BYD shares back in BYD has done incredibly well in expanding its presence across the battery value chain, from

being a prominent battery manufacturer, to one of the biggest EV selling brand worldwide. In August 2023, global sales of plug-in electric cars exceeded 1.2 million units, the third best monthly number ever. 6 out of the top 10 models sold were BYD, thanks largely to the company’s strong local presence in China 3.

The macro story

2023 has clearly not been a year for Chinese stocks. As of 23 October, the S&P China 500 Index is

down over 13% while the S&P 500 Index is up 10% year-to-date (both in USD terms) 4 . China’s

performance has been marred by disappointment over China’s economic recovery which had

investors around the world excited at the start of 2023 when the country was emerging from COVID-19 lockdowns.

This negative sentiment has also hit the Chinese battery market. As of 23 October, the WisdomTree Battery Solutions Index (WTBSI) is down 16% year-to-date, with Chinese stocks making the biggest negative contribution to returns 5 . WTBSI, which caps the weight of all countries except the US at 25% (with the US capped at 50%) at each six-monthly rebalance, currently allocates its highest country allocation to China (at just shy of 25%) 6.

Given its dominance in the battery industry, China holding a high weight in a battery value chain

portfolio is not unreasonable. Recently, between the start of 2020 and end of 2021, WTBSI was up

113% and China 7 , on account of its large weight even back then, made the biggest contribution to

this return among countries.

The current macro headwinds in China have created a stark divide between stock market

performance and the underlying fundamentals of the battery industry. At WisdomTree, we also

believe that the negative sentiment towards China’s economic fortunes this year may have

bottomed out. Most recently, China’s economy grew 4.9% year-on-year in the third quarter of 2023,

beating market forecasts of 4.4%. Similarly, the all-important manufacturing purchasing managers’

index (PMI) was in expansionary territory for both August and September 8 . While these numbers

don’t necessarily demonstrate a clear new uptrend in economic activity, they do paint a more

encouraging picture.

China is a powerhouse in the world of batteries and its dominant position is represented by an array of rapidly emerging companies. Investors looking to build an exposure that is truly representative of the space will be remiss to ignore China’s significance. At WisdomTree, we believe markets have punished China enough based on their disappointment over the country’s macroeconomic performance this year. The weak performance of Chinese battery stocks this year is inconsistent with the strong underlying trends in the industry. It is such dislocations that could create potential opportunities for investors.