After a storm comes a calm

3 JAN, 2023

By Elisa Belgacem, seniore credit strategist at Generali Investments.

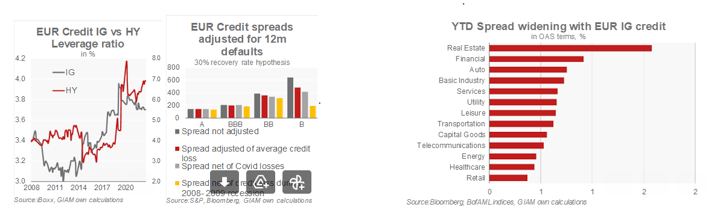

2022 was the worst year in history for EUR IG total return performance, allowing 2023 to start on more attractive levels. Valuations metrics among the credit universe are currently showing that the European IG space is the cheapest compared to US IG and both EU and US HY. Technical should be relatively neutral in EUR IG, with QT starting on the negative side in the first half of 2023 but supply should also be limited especially in non-financials. As rates should also be more stable, the carry of the IG space coupled with extremely low historical defaults should help flows stabilise. In HY the picture will likely be more challenging. Supply has been almost inexistent in 2022, forcing HY corporates to issue more next year in a challenging market environment.

Higher carry but higher defaults

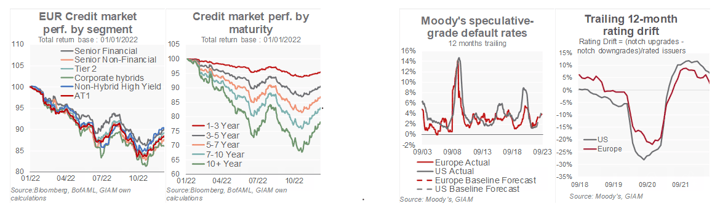

Rating agencies will logically start with the most at-risk companies. As they did in 2020, we expect rating agencies to revise in priority the notations of companies at the lower end of the rating spectrum. Indeed, nearly 50% of HY-rated companies were downgraded by at least one notch, while IG has been mostly put on a negative outlook. Predicting defaults in this context is also a rather complex exercise. On one side, Europe's gas situation will command a recession that could vary according to winter temperatures. And on the other side, the government support that helped contain defaults to 5% in Europe during Covid will be smaller due to lesser fiscal leeway from governments. Also, we expect smaller companies to be the most at risk. Hence banks' asset quality should also deteriorate, which leads us to remain underweight financials versus non-financials in spread terms. However, as the carry is now higher in the financial space as spreads have substantially diverged over the course of 2022, we expect the total returns of the financial index to surpass the non-financial one. Hence, we do upgrade financials in our tactical asset allocation.

Prefer long IG and subordination risk to pure HY

The dispersion of total return performances across the various credit segments, has been relatively low. The true discriminant factor in 2022 has been duration. The 10Y+ segment of EUR IG is closing the year with nearly 25% of negative performance. We think 2023 will be different, although credit curves are relatively flat after the 5Y point, but for a good reason. With rates likely plateauing, in a context of high uncertainty regarding defaults in the HY space, it makes sense to go long IG to enhance returns in credit. Similarly, subordinated bonds are mostly compensating for extension risk and coupon risk. At current level we do estimate that the former is well compensated for, while coupon risk is very low as most of those bonds are issued by solid IG rated companies. We even see upside in spread terms as we do expect more companies to call their bonds than what the market is expecting in corporate hybrid and in AT1s.

Strong influence of climate profile in valuations

ECB just started to tilt its corporate purchases according to climate criteria. While this is a crucial step for the ECB, the fact that the quantitative tightening is fast approaching, potentially reducing the reinvestments in the APP already in Q123, may reduce the market impact initially envisaged. That said, as most private investors are concomitantly attempting to improve the carbon footprint of their portfolio, we are still expecting the “E” component of the ESG scores to further feed into credit market valuations, mostly in the most polluting sectors (Energy, Utilities). Also we do expect the labelled ESG issuances to account for 40% of the 2023 supply.

Decompression trade still on

Overall, we do prefer IG to semi-core and peripheral sovereigns, and we prefer Europe to the US on valuation grounds. In Europe IG levels are currently incorporating a severe recession scenario. We expect spreads to trade around current levels over the course of next year. For HY, we think that positioning is already very short, but risks remain elevated and current levels do not reflect for the downside risks to our economic scenario. Consequently, we expect spreads should widen nearly 100bp in the first half of 2023 before ending the year 50 -60p wider compared to current levels.