AI’s second life comes through robotics

17 JUL, 2026

By Jeffrey Cleveland, Chief Economist at Payden & Rygel

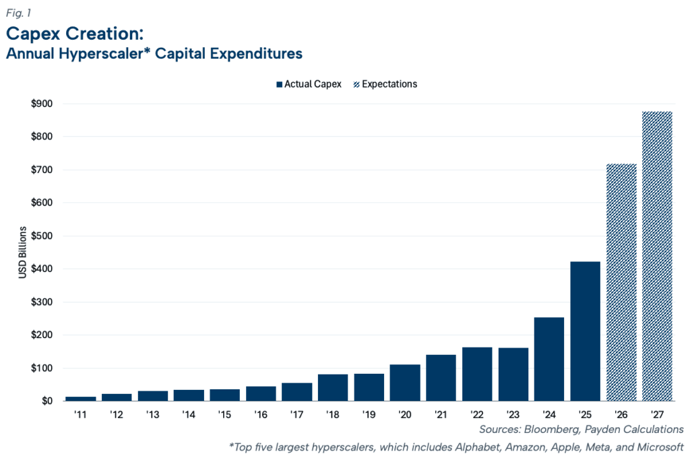

The launch of ChatGPT in November 2022 triggered a wave of investment in AI and data centers: last year alone, major hyperscalers invested $422 billion and plan to increase spending by nearly 60% by 2026 (Figure 1). While skeptics argue that chatbots won't generate enough revenue to justify these investments, the next wave of AI could come from robotics.

Progress in this field has already been significant in recent years: robots, once limited to repetitive tasks, are gaining planning capabilities thanks to LLMs. In 2023, Google DeepMind connected them to knowledge available on the web; in 2024, Physical Intelligence developed a model capable of controlling eight different types of robots; and in early 2026, Nvidia unveiled a system able to learn by observing simple videos of humans.

Large-scale adoption will certainly take time, as shown by the experience of autonomous vehicles: Waymo only achieved a meaningful presence in 2025, and in just a handful of US cities. For robots, the challenge is even more complex, since they must operate in unstructured environments – such as homes and hospitals – and require training data that is far harder to collect.

Performance and cost also remain limiting factors. The most advanced models today achieve 80–90% accuracy in specific tasks – still insufficient to replace human labor at scale. Moreover, according to McKinsey, the cost of humanoid robots will need to fall by 80–90% from the current $150,000–$500,000 range to enable widespread industrial adoption. As a result, the market for autonomous humanoids was worth less than $250 million in 2025, compared with over $40 billion invested in generative AI startups.

The spread of physical AI does not necessarily require humanoid robots capable of replicating every human activity. The history of innovation suggests that, rather than adapting machines to existing environments, it is often more effective to redesign the environment around their capabilities. The same principle could apply to autonomous robots: warehouses and factories, being controlled environments, lend themselves more easily to automation, while less structured settings are more likely to see the rise of robots specialized in single tasks. For example, after acquiring Kiva Systems, Amazon redesigned its warehouses around robots, now deploying over one million of them.

Whatever path physical AI takes, the spread of autonomous robots will significantly increase computing power demand. Estimates already indicate that the computing power required to train chatbots and AI agents will grow 166% over the next five years. The impact of robotics could be even greater. Current models use just one-hundredth of the computing power required to train the most advanced LLMs, suggesting a sharp increase in resource needs as the technology evolves. Additionally, while a chatbot only uses computing power when it receives a request, a robot must process data continuously to perceive its environment, plan actions, and execute them in real time. Technical requirements are also more stringent. Robots need dedicated GPUs and extremely low latency: if a humanoid risks falling, it has only a few milliseconds to react, unlike chatbots, which can take a few seconds to respond.

Quantifying future demand remains difficult, but a preliminary estimate suggests that running an autonomous robot for one hour using the latest Nvidia GPUs requires computing power equivalent to roughly 1,000 ChatGPT requests. If every manufacturing worker were replaced by a robot operating 24 hours a day, the computing capacity needed for inference would exceed today's ChatGPT demand by more than tenfold.

In conclusion, chatbots may represent only the first phase – the next wave of AI is likely to be physical. In this scenario, investments in developing increasingly advanced models, dedicated hardware, and new data centers may prove not to be excess capacity, but a necessity. The spread of physical AI could push computing power demand well beyond current expectations.

This material reflects the opinion of Payden & Rygel as of the date of this document and is subject to change without notice. The sources on which it is based are believed to be reliable but cannot be guaranteed. The article is for illustrative purposes only and should not be construed as tax, legal, or professional financial advice, nor as an offer to buy or sell securities. Past performance is no guarantee of future results. This material has been approved by Payden & Rygel Global Limited, a company authorized and regulated by the UK Financial Conduct Authority, and by Payden Global SIM S.p.A., an investment firm authorized and regulated by Italian CONSOB.

Related articles

From Hormuz to healthcare – the overlooked supply chain risk in pharmaceuticals

From Hormuz to healthcare – the overlooked supply chain risk in pharmaceuticalsBy Invesco

Better times ahead? Analysing Germany’s new macroeconomic reforms

Better times ahead? Analysing Germany’s new macroeconomic reformsBy Felipe Villarroel