Contrarian Investment: what it is, how it works, and why it interests the professional investor

26 JUN, 2026

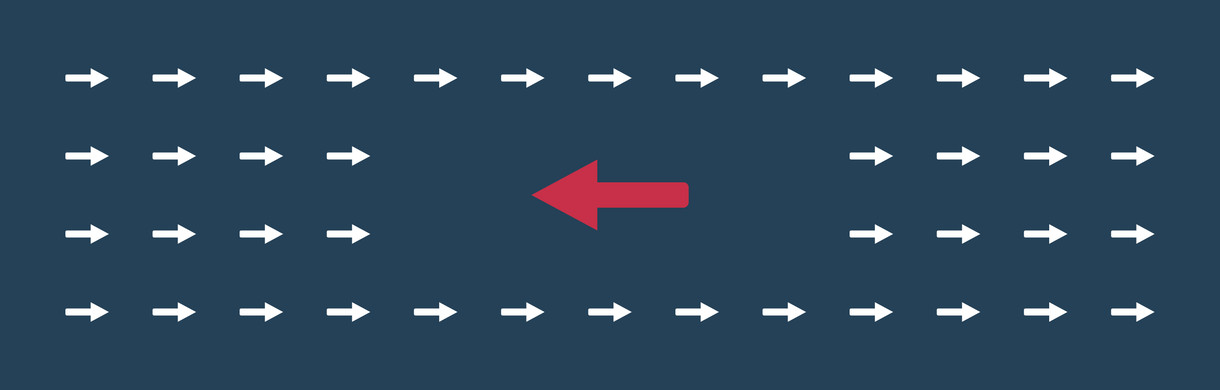

The contrarian investment is a strategy that consists of taking positions contrary to the dominant sentiment of the market: buying assets when the majority rejects them and reducing exposure when optimism becomes widespread. The contrarian investor starts from a central premise: prices tend to move away from their intrinsic value when emotions —fear and greed— dominate the decisions of the masses, and these inefficiencies end up being corrected.

It's not about being contrary for the sake of it. The phrase attributed to Nathan Rothschild —buy "when there's blood in the streets"— sums up the spirit, but the professional approach requires grounding each position in analysis, not in mere opposition to consensus.

What is contrarian investment and what is it based on?

The approach rests on two conceptual pillars. The first is mean reversion: the tendency of valuations, business margins, and returns to return to their historical average after periods of excess, both upwards and downwards. The second is behavioral finance, which documents how biases such as herd effect, loss aversion, or overconfidence generate systematic overreactions in prices.

When an asset, sector or entire market accumulates bad news, pessimism can push quotes below their reasonable value. The contrarian investor interprets this indiscriminate punishment as an opportunity, as long as the price deterioration exceeds the actual deterioration of the fundamentals.

It should be distinguished from value investing, with which it shares roots. The value focuses on the gap between price and intrinsic value; while the contrarian approach adds an explicit layer of market psychology, deliberately positioning itself against the prevailing sentiment. Both usually converge, but they are not identical: a value can be cheap without being hated, and a despised asset is not always undervalued.

How to identify contrarian opportunities

The professional investor does not guide himself by intuitions, but by sentiment indicators that allow measuring the emotional extremes of the market. Among the most used are the inflows and outflows of funds, sentiment surveys (such as the AAII in the US), the put/call ratio, the levels of the VIX volatility index and the positioning of institutional investors.

To these are added the classic fundamental analysis —depressed valuation ratios compared to their historical average, discounts on book value, high dividend yields— and the qualitative reading of the dominant narrative in the media and among analysts. The most valuable signal appears when a negative narrative becomes unanimous: capitulation usually coincides with market bottoms.

The risks that the professional investor should not ignore

Contrarian investment is not without dangers, and the main one is confusing a cheap asset with a value trap (value trap): companies whose price falls not due to excess pessimism, but because their fundamentals are deteriorating structurally. Going against the market only makes sense when the consensus is wrong, not when it is right.

The second risk is timing. As the market maxim warns, these can remain irrational longer than the investor can maintain his solvency. An undervalued asset can continue to fall for months or years, which requires a broad time horizon, rigorous risk management and considerable emotional control to sustain unpopular positions.

Reference managers such as John Templeton, David Dreman or Howard Marks —the latter with his concept of second-level thinking— have built their careers on this philosophy. Their common lesson is clear: superior profitability comes from thinking and acting differently from the majority, but also from doing it rightly. In contrarian investment, having a different opinion is not enough; it must be well-founded and, above all, be correct.