How does the Fundsmith Equity Fund invest?

24 JUN, 2024

By Andrea Sepúlveda from LatamSelf

The Fundsmith Equity Fund is a global concentrated equity fund, launched in 2011, which has received recognition from its investors (good fund size) and from globally recognized financial information platforms. Thanks to its unique approach and the management company's philosophy.

In this article, we analyze this investment strategy.

Characteristics of the Fundsmith Equity Fund

The main features of this investment fund are:

- Investment philosophy: The investment philosophy consists of buying and holding high-quality companies that continuously increase their value. In this way, the central idea is: buy good companies, don't pay too much, and keep investments long term.

- Investment strategy: the fund's investment strategy avoids short-term trading and focuses on the careful selection of its concentrated portfolio of shares. An important point of the fund's strategy is that, in addition to being concentrated, it does not use derivatives nor does it hedge. This is closely linked to the vision of the management company, as Fundsmith declares to focus on offering a return at a reasonable cost and to have been created to differentiate itself from other management companies by doing things differently, in line with Sir John Templeton's axiom: "If you want to achieve better results than others, you have to do things differently from the crowd."

- Benchmark index: this strategy follows the MSCI World Index.

- Investment team: Terry Smith is a renowned fund manager and English entrepreneur, with a wide and varied experience in the financial world, as well as having received several awards and recognitions from the industry. He is the author of the 1992 bestseller "Accounting for Growth" in which he criticized the accounting techniques used by some listed companies that always reported growth

- Assets: At the end of May 2024, the strategy had almost 8.8 billion euros in assets under management.

- Investment company: Fundsmith is an asset management company based in London, founded in 2010 by Terry Smith. The management company has only three strategies that follow the same philosophy and investment process, but with different sets of opportunities: developed global large caps, developed global mid caps, and emerging global stocks. In addition to its well-defined philosophy, Fundsmith also stands out for its statement of not paying much attention to benchmark indices/parameters or tracking error.

Evolution of the Fundsmith Equity Fund

Given its history, the fund allows us to observe its long-term results, as suggested by the manager. By examining the annualized results up to the current date and from its launch, it can be seen that the fund has been able to beat its benchmark with a small group of companies in the portfolio.

In other shorter time horizons or in specific years, it is possible that the fund suffers a bit compared to the MSCI World Index, but this is something that the investment team signals since, given that the fund is actively managed and with a long-term view of quality companies, it may not maintain any of the components of the benchmark index or have significant differences (up to totals) with the same.

Therefore, short-term profitability may not be favorable in periods when the market prefers lower quality companies, so to speak. The fund team believes that limiting the set of opportunities and maintaining a long-term investment horizon is the right path.

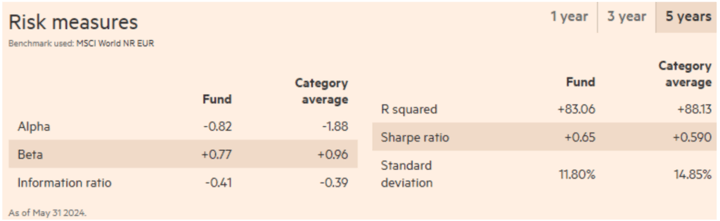

As for risk metrics, the management company does not show them in the fund's monthly card. Using an external information source, we will examine the 5-year data comparing it with the benchmark.

The first thing that catches the eye is the alpha, which corresponds to what was previously observed in the performance results. In recent years, the investment team has not managed to exceed the benchmark performance in two important time horizons for an institutional evaluation, 3 and 5 years. In relation to the market Beta, this is less than 1 in both 3 and 5 years, and here there is consistency. The team consistently takes less risk compared to the comparison market despite having a more concentrated and often aggressive selection in sectors or regions.

However, considering other ratios such as the Information Ratio, it can be seen that this has not necessarily brought benefits.

Conclusions

Advantages

- Manager with long-term commitment and low risk of changing PM.

- Low portfolio turnover that reduces transaction costs and allows to focus on long-term growth.

Disadvantages

- It is a concentrated fund with high conviction, which is not necessarily negative, but the investor must understand the manager's philosophy well to commit in the long term.