Monetary policy starts to bite – but the economy won’t slow yet

5 APR, 2023

By Julius Bär

The cracks in the growth picture are finally showing. Since the one-year anniversary of the first-rate hikes in the US in March, credit metrics have shown a serious tightening. However, this doesn’t necessarily point to the economy teetering off the edge in the coming weeks.

The US Senior Loan Officer Opinion Survey indicates that banks have started to hit the brakes. Given the turmoil in smaller US banks, there is added pressure for them to curb lending. The woes seem to be particularly centred around commercial real estate this time. Here in Europe, loan growth is also slowing, albeit with a lag given the delay in rate hikes and the slower pace.

However, ‘hitting the brakes’ and ‘slowing growth’ do not mean the economy is falling off a cliff anytime soon. Rather, we expect that the effects, in aggregate, will only be visible much later this year – or even only in 2024. The reason for this is the lower rate sensitivity of the US due to consumers who have cut their debt levels relative to their wealth by a large amount (as compared to 2007) and are still sitting on tons of cash post-Covid-19. In Europe, banking regulations are tighter and bank deposits are stickier than in the US, but the effect is similar, i.e. a more resilient economy. Even the panicky output cut by OPEC+ this week does not point to an immediate global recession but rather to well-supplied energy markets.

In stark contrast to these lags of monetary policy, investors around the world were already in a ‘falling off a cliff’ scenario by mid-March. The share of investors who are bullish on stocks is still close to its five-year lows, and fund manager surveys have triggered another contrarian buy signal as cash holdings there have skyrocketed. So there are many opportunities for the brave in the short term. We suggest buying quality businesses that have some turnaround potential, or straight growth names.

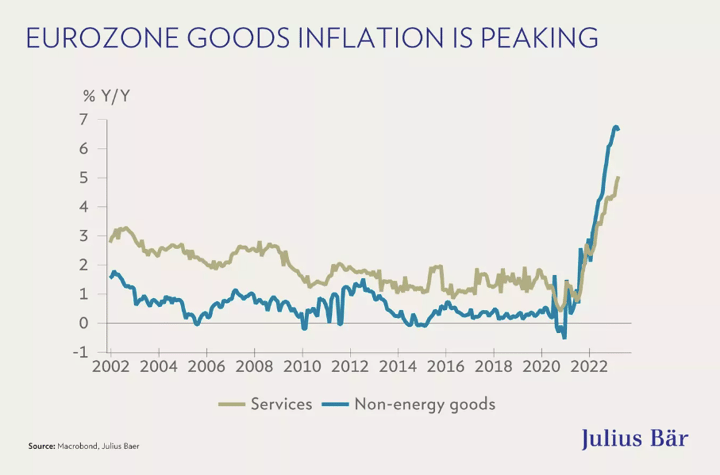

Eurozone inflation: Political pressure on the European Central Bank remains

Inflation is cooling, albeit more slowly than hoped. In the eurozone, inflation slowed overall in March thanks to lower energy prices, but food prices continued to surge and services price inflation remained uncomfortably high. Furthermore, non-energy goods price inflation has slowed only somewhat over the past months. As a result, the political pressure on central banks, particularly the European Central Bank (ECB), to do more in the fight against inflation is not diminishing.

In this chart, the rate of inflation non-energy goods is shown to have reached its peak level in the eurozone.

Looking at credit dynamics, which are showing a marked slowdown, central banks have already done enough. However, looking at currently reported inflation, the European Central Bank has not done enough to slow down infaltion. But this overlooks the fact that the transmission channel from higher policy rates to lower credit, weaker economic growth, and, ultimately, lower inflation is characterised by long lags of more than 12 months and is highly dependent on the shape of the banking system.

Recently reported loan and credit data for February 2023 suggests that overall loan growth has slowed across all categories, with three-month loan growth to businesses declining for the second month in a row. Loans to households, including mortgages, have also slowed markedly but are still expanding. This is a clear indication that the ECB is already conducting a restrictive monetary policy and that further tightening should be modest in order to avoid an overtightening of monetary policy.