Playing with Yields

18 DEC, 2024

By Vontobel

By: Gianluca Ungari, Vontobel's Head of Hybrid Portfolio Management & Sven Schubert, Head of Macro Research and Quantitative Investing at Vontobel.

Financial markets welcomed Donald Trump's re-election with optimism. Risk assets, particularly equities, extended their strong early November rally, despite rising inflation expectations and reduced hopes of Fed easing.

The S&P 500 is up 28% so far this year, driven largely by technology stocks. Historically, US equity markets have tended to perform better under Republican than Democratic administrations. Trump's pro-business agenda, including tax cuts and infrastructure investments, aligns with this trend, giving investors reason to remain optimistic.

Tariffs: A double-edged sword for markets

While the administration's growth-focused initiatives boost optimism, they also pose challenges. Rising inflation and reduced monetary support may test market resilience, but for now these obstacles appear manageable. The administration's pro-business stance continues to inspire investor confidence, setting the stage for optimism even amid uncertainty.

However, financing these spending proposals comes with complexities. Tariffs, described by Trump as ‘the most beautiful word’, are proving highly disruptive. These measures, targeting major trading partners such as China, Mexico, Europe and Canada, put pressure on markets around the world. In addition to dampening growth potential, tariffs introduce inflationary pressures that are difficult for markets to digest. In contrast to the ‘good’ growth-driven inflation, this tariff-induced ‘bad’ inflation poses a major challenge for investors.

Government bond yields near record highs

Rising interest rates and inflation expectations have created headwinds for fixed income investors, but there are signs that government bond yields may be approaching their peak.

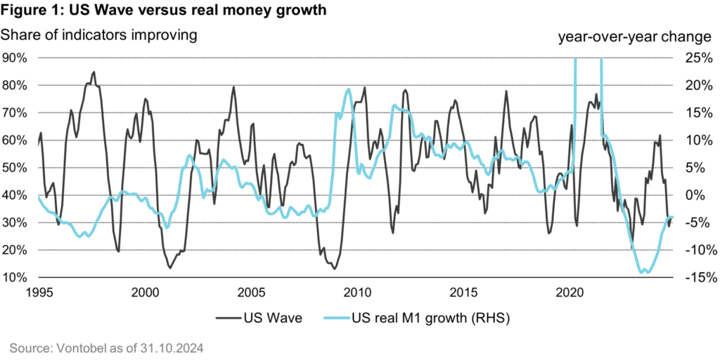

First, from the point of view of economic growth, the Federal Reserve has little reason to abandon its expansionary policy. Despite recent rate cuts, monetary policy remains tight. Real money growth (M1) is hovering around historical lows, and broader indicators, such as the US Wave2, point to rather weak economic growth, as shown in Figure 1. These conditions suggest that the Fed remains committed to further easing.

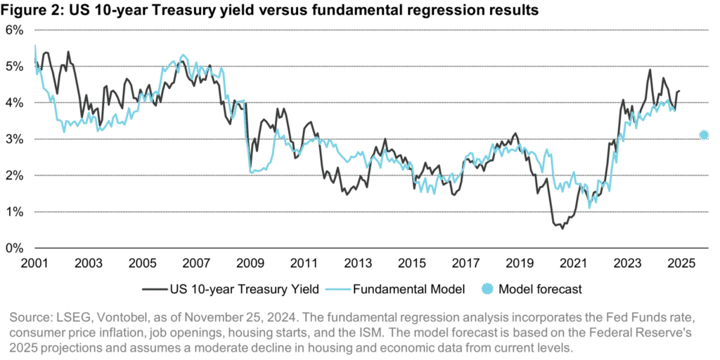

Second, markets appear to have priced in an overly pessimistic scenario for bonds. Current U.S. 10-year yields are overshooting levels justified by historical drivers of yields, as shown in Figure 2. Looking ahead, inflation expectations—if Trump’s first term is any guide—may ease slightly. Post-election uncertainty often brings an initial spike in inflation expectations, but these tend to recede as the dust settles. Incorporating this information into our proprietary model results in a 10-year yield forecast well below the current level.

While challenges remain, these factors offer a constructive outlook for fixed income investors navigating the current landscape.

How do we prefer a constructive view on duration?

Determining when government bond yields will peak is challenging, especially with the uncertainty surrounding US import tariffs. While a 10% across-the-board tariff and a 60% tariff on China could represent upper limits, historical experience suggests that Donald Trump could use tariffs as a bargaining tool, which could result in lower levels than currently proposed.

Given this uncertainty, we believe that taking a long duration position is not the most effective strategy, even with our positive medium-term outlook. What is certain, however, is that the reduced election-related uncertainty has contributed to lower government bond volatility, as shown in Figure 3. This is to be expected in the post-election period, as fixed income volatility historically declines in the months following election day, as shown in Figure 3.This approach allows us to profit from a possible decline in yields in 2025, while avoiding the risks associated with trying to time the fixed income market.