Rally fatigue: dichotomy between markets and economy too wide

3 MAR, 2023

By Amundi

Vincent Mortier, Group Chief Investment Officer, and Matteo Germano, Deputy Group Chief

Investment Officer at Amundi AM, give their views on how China's reopening and the trajectory of inflation will affect the markets.

The year started with a rally mood amid short covering and the return of retail investors’ risk appetite. There were some supporting reasons for the situation, at least in Europe and China, where lower gas prices and China reopening helped to remove some of the downside economic risks that were on the table last year. However, the rally has gone too far based on assumptions that inflation is falling fast, the job of central banks is done, and the economy is well on track for a soft landing, with no earnings recession.

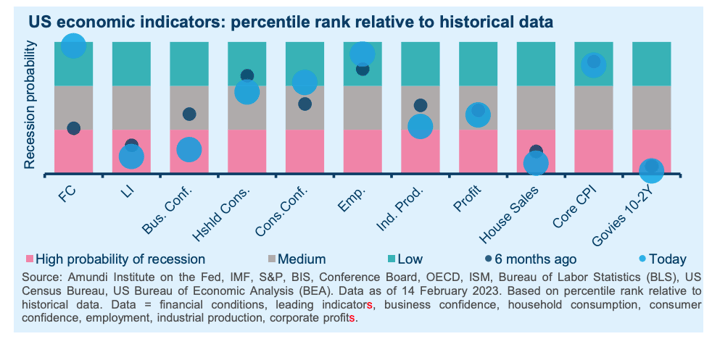

The tricky part for investors starts now. The bears may not arrive, but some caution from here is necessary. The dichotomy between loose financial conditions and tight lending standards for the real economy is striking. Markets remain priced for perfection, despite high uncertainty and divergences on the economic front. In particular, while we recently upgraded our forecasts for 2023, the devil is in the detail. Regarding the US, our GDP forecast is unchanged, but we see deteriorating quarterly dynamics for the second part of the year. For the Eurozone, we upgraded our GDP projections for 2023, but this was mainly due to carry-over from last year and growth expectations remain flattish. China reopening is clearly a positive for the global economy, but we believe this will mainly support the domestic performance.

Secondly, inflation is declining slowly, but markets see it falling rapidly and the path towards the 2% CB target appears to be long and bumpy. With regard to central banks, we see that the Fed is close to the end of tightening, but the ECB is still hawkish. Finally, appetite for emerging markets is returning, but regarding developed markets, caution prevails.

Against this fragmented backdrop, we think investors should remain cautious but recognise that uncertainty is high on both sides (upside and downside).

Consequently, we updated some of our main convictions as follows: