5 reasons to invest in fixed income being active

1 APR, 2024

Authors: Marco Giordano, fixed income investment director; Amar Reganti, fixed income strategist; and Adam Norman, investment communication director; Wellington Management

In recent years, many investors have moved from active strategies to basic passive fixed income strategies, considering that these markets offer fewer idiosyncratic risks than equities and are too efficient for active managers to generate alpha. However, passive strategies have often underperformed core plus active fixed income strategies and can expose investors to various forms of unintended risk. Active fixed income management not only offers the possibility of improving returns, but can also add value by aligning an investor's objectives with risks in several key areas - market structure, credit deterioration, dislocations and dispersion - where index tracking approaches may fall short.

Reason 1: Profitability Potential

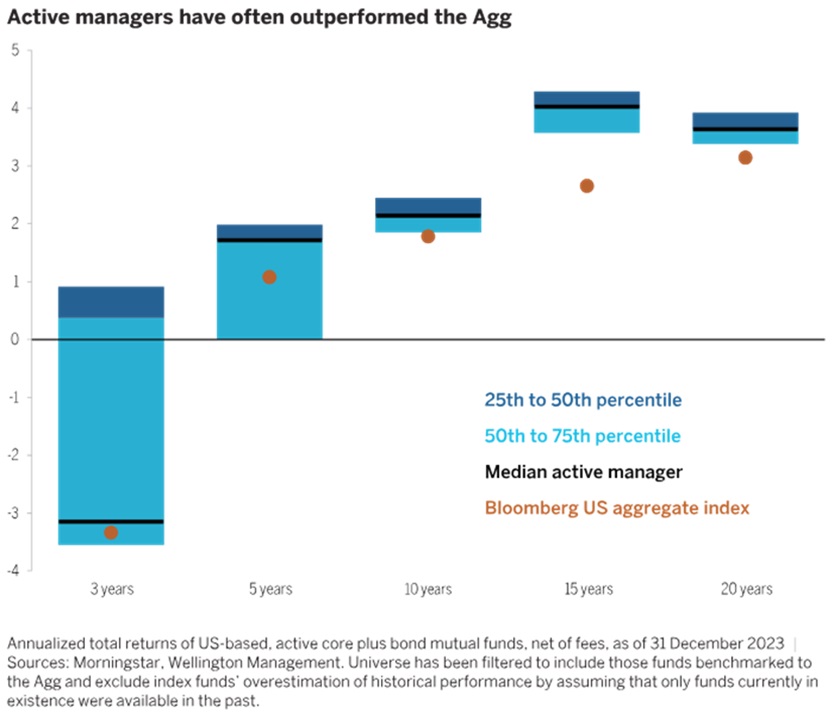

Advocates of index-replicating fixed income strategies argue that active managers cannot consistently outperform the Bloomberg US Aggregate Bond Index (the "Agg"), net of management fees. However, core plus active fixed income strategies have historically performed well against the index in most periods over the last 20 years (Chart 1).

The higher profitability of active strategies over such a prolonged period, which spans credit cycle turns, suggests the existence of factors that go beyond credit emphasis. In fact, investors have many other tools to try to generate alpha, such as sector rotation, allocations outside the benchmark index, duration positioning, security selection and (in the case of global strategies) country and currency selection. These non-credit tools can also mitigate downturns in adverse credit environments.

Having said that, the overweighting of credit has clearly contributed to increasing the excess return of investors in most periods; the major exceptions in the last 20 years have been the global financial crisis (GFC) and the COVID pandemic. The recovery of the widening spreads that emerged from these periods of reduction compensated for the deficits of active managers against index returns in 2008 and early 2020. Although the average return of active managers against the index tends to be positively correlated with credit spreads - outperforming the index when spreads narrow and lagging when spreads widen -, periods of negative return have often been of short duration and usually offset by longer periods of positive returns.

Reason 2: Market Structure

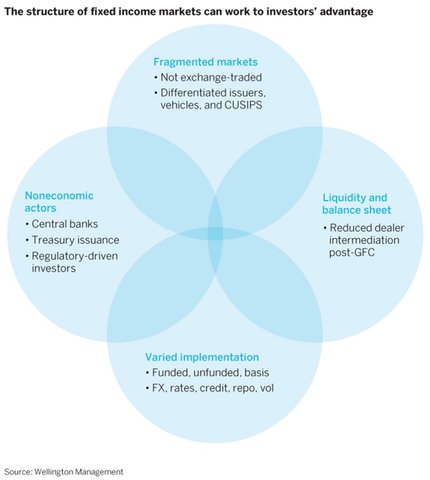

Fixed income markets tend to be fragmented and opaque, prone to experiencing volatile liquidity. However, these characteristics can benefit thoughtful investors by increasing the premiums they can earn through active management (Chart 2).

- Fragmented: Unlike equity markets, there is no "central" fixed income exchange. Instead, securities continue to be traded "over-the-counter" (OTC). This often requires a trading desk to strategically plan how it will buy or sell a bond, allowing the implementation aspect of the investment to potentially add value. In addition, issuers may have different bonds in various parts of their capital structure or in different currencies and maturities. A single corporate or government issuer may have numerous individual bonds, each with different terms and conditions. This can mean that risks and rewards also differ. Passive exposure does very little to distinguish between these individual bonds.

- Non-economic actors: Some key participants in fixed income markets pursue objectives other than a rate of return. These include central banks and the US Treasury, along with commercial banks and insurance companies that may be subject to investment restrictions imposed by the regulatory framework. Therefore, these counterparts usually do not trade based on valuations, leaving room for active investors to buy or sell bonds at opportune times.

- Liquidity and balance: The reduction of intermediaries' balances after the global financial crisis has made liquidity more variable in fixed income markets. Since there is no central fixed income market, investors rely on intermediaries to act as counterparties in transactions and maintain bond inventories. The reduced ability of an intermediary to "intermediate" or serve as a storage place for inventories means that bond prices can be influenced by non-economic agents, providing an opportunity for an active investor to supply liquidity when traditional intermediaries cannot do so and to do so more effectively than passive investment.

Execution: Fixed income markets offer a number of ways for qualified professionals to add value through implementation, many of which are not replicable in passive terms. The issuer, the CUSIP, and the maturity are important facets of a decision. In addition, active investors can decide whether exposure looks better in cash format ("funded") or through derivatives such as futures ("unfunded") and can try to exploit the spreads between the two. There is a similar dynamic in currency markets, where lending dollars through the cross-currency market can offer solid risk-adjusted returns. Over time, these and other tactics have often translated into superior results compared to passive exposure.

Reason 3: Credit deterioration

An important feature of credit is its asymmetric risk profile: the market value of a bond can fall much more than it is likely to rise. (In other words, credit spreads can widen much more than they can narrow). An active investor can play a vital role in anticipating turns in the credit cycle and avoiding downside risk. In particular, fundamental research can help managers identify a credit's deterioration or improvement before rating agencies do, and even before the change is discounted by the markets.

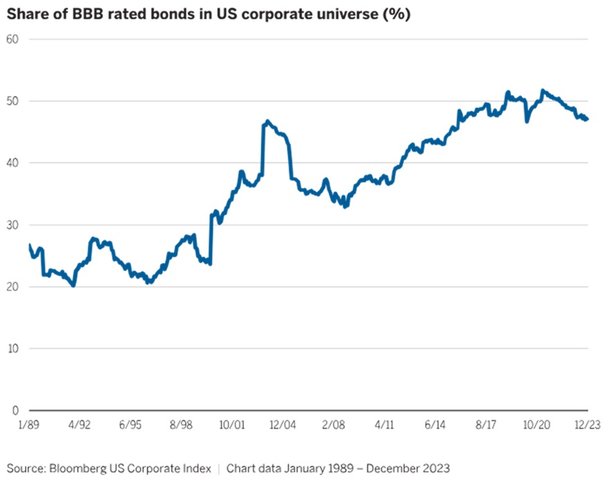

One of the main concerns of investors is that lower-rated credits now represent a larger proportion than in the past of the universe of investment-grade credits (graph 3). A deeper analysis of a company's leverage ratios is essential to understand if the company's ability to service its debt is negatively affected by higher debt levels. At a minimum, higher leverage should be a clear warning sign for credit teams to investigate a company's earnings and free cash flow, its asset sale and dividend plans, and the degree of commitment of its senior management to investment-grade ratings. An experienced portfolio management team that knows how to go beyond the headlines may be able to identify opportunities and risks.

The rules of index providers for credit rating downgrades can also cause passive strategies to lag behind active ones. In the Bloomberg Investment Grade Corporate Index, securities downgraded by at least two of the three major credit rating agencies (Standard and Poor's, Moody's and Fitch) must leave the index before the end of the month in which they have been downgraded. But deteriorated credits are often sold before their rating is downgraded, as investors anticipate the downgrade. As a result, indices are often forced to remove these bonds after they have dropped in price.

Reason 4: Dislocations

Dislocations can occur in all segments of the fixed income markets, driven by various structural imbalances (for example, the growth of debt volume versus the reduction of market-making activities) that leave securities from all sectors vulnerable to episodes of illiquidity. These dislocations - and the policy makers' responses to them - can create opportunities for active managers.

Dislocations are not a new phenomenon, and we believe they could be an omnipresent feature of fixed income markets. Over the last decade, we have witnessed an increase in the frequency and volume of dislocations caused by a growing number of structural imbalances in fixed income markets (Chart 4). These structural imbalances make fixed income assets very vulnerable in periods of market stress, both at the macroeconomic and microeconomic level. Although they can pose a serious challenge to traditional fixed income investment, these imbalances have created a vein of dislocation that adequately resourced core plus bond managers should identify and try to exploit.

In our opinion, the current and growing structural imbalances of the market should cause more frequent and severe disruptions in the future. We believe that investors with patient and opportunistic capital can take advantage of these market dislocations, creating the potential for attractive return outcomes. Active managers can try to generate returns from the periodic episodes of volatility that, in our opinion, are now endemic in fixed income markets.

Reason 5: Divergence

Opportunities change over time and risk stances should not remain static in the different phases of the economic cycle. Unsynchronized economic, interest rate, and credit cycles generate inefficiencies that often create these opportunities. The best way to identify and capture these inefficiencies is to use independent and diversified alpha sources.

Investors can find more opportunities to generate alpha when dispersion is high. At wider spread levels, indiscriminate investors may be rewarded simply by increasing the portfolio's beta, while when spreads are narrow, it is prudent to place greater emphasis on a judicious credit selection. This is especially true in the current environment, as durations have extended over the last two decades and spreads are at the narrowest end of their historical ranges. There is much less margin for error to cushion rate or spread increases or errors in credit selection.

But this does not mean that there are no opportunities. The recovery of all differential sectors has been quick compared to previous crises, but it is far from being uniform. Graph 5 illustrates our profitability forecasts for a set of basic bonds plus opportunities, which assumes that the spreads retreat 50% towards their long-term average during the following year.