The European electric vehicle market and the critical dependence on raw materials

15 MAY, 2026

Europe’s transition toward electric mobility is advancing rapidly. After a temporary slowdown in 2024, when electric vehicle (EV) sales grew by only +1%, the market rebounded strongly in 2025, with an increase of +34%. This recovery was driven by a broader range of entry-level and mid-range models, together with a regulatory environment increasingly focused on transport decarbonization.

This acceleration is transforming the value chains of the European automotive sector and highlighting the region’s strong dependence on critical raw materials. Addressing this challenge will require a coordinated combination of policies including demand support, selective reindustrialization, and greater supply security.

Structural growth

Sales of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) in Europe are expected to grow annually by 15% and 18% respectively between 2025 and 2030. By the end of the decade, BEVs could account for around 42% of the European passenger car market, compared with approximately 16.4% in 2026.

At the same time, the distribution of value within the vehicle is undergoing a profound shift. In a BEV, around 50% of the total value comes from the electric powertrain system, with the battery alone accounting for nearly 35%. By contrast, in internal combustion engine vehicles, the engine and transmission represent only about 18% of the total value. As a result, batteries — and the materials required to produce them — are becoming a strategic component.

A critical dependence

Europe — and its electric vehicle industry — remains highly dependent on imported raw materials. The region sources around 99% of its natural graphite, 96% of its manganese, more than 80% of its lithium and cobalt, and nearly 98% of its refined rare earths from abroad, mainly from China. This dependence is especially pronounced in the case of permanent magnets, which are essential for electric motors and whose global refining and production are controlled by China at around 90%.

Recent geopolitical developments underline the risks associated with this dependence. For example, on October 13, 2025, China announced new export controls on dual-use technologies. Although primarily aimed at defense-related applications, these measures could disrupt the automotive supply chain by restricting access to key materials for cathodes and anodes.

Importantly, this dependence is not due to a lack of geological resources. In the 1980s, Europe was among the leading producers of rare earth elements. However, stricter environmental regulations and lower ore quality gradually increased production costs, while China expanded its output, supported by lower labor costs, abundant reserves, and less stringent environmental controls. Today, reviving Europe’s mining sector will depend on several factors: deposit quality, speed of project development, access to financing, refining capacity, and social acceptance of mining activities.

Recycling: a partial solution, but 15 years away

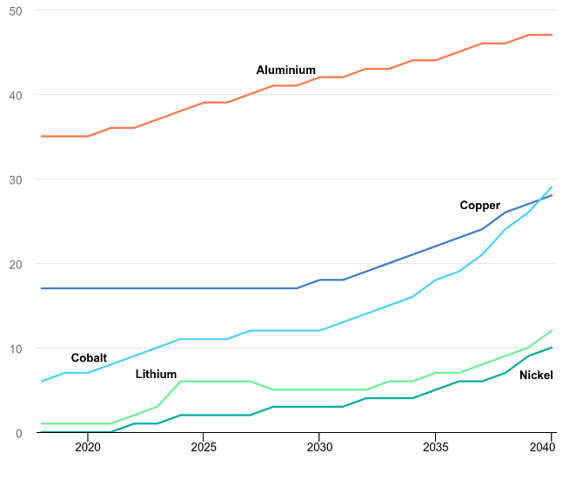

In this context, recycling represents a strategic lever. The Critical Raw Materials Act, adopted in 2024, sets a clear objective: to meet at least 25% of Europe’s annual consumption of critical materials through recycling by 2030. In the case of batteries, recycling could reduce the need for new extraction by between 10% and 30% for several key minerals under a net-zero emissions scenario.

Proportion of secondary supply relative to total demand for selected materials in the Net Zero Emissions Scenario, 2010–2040

Recycling also offers a double benefit. On the one hand, it secures domestic supply flows of lithium, nickel, cobalt, copper, and graphite while protecting against geopolitical shocks. On the other hand, it delivers environmental advantages: producing one ton of recycled aluminum generates up to 97% less CO₂ than primary production, with similar reductions for other metals used in batteries.

However, recycling rates remain highly uneven. While they are relatively high for steel and aluminum, they remain very low for rare earth elements, standing at only around 5% to 10% globally. There is also a time limitation: the approximately 15-year lifespan of batteries means that the first truly significant volumes of recycled materials will not become available before 2040. Until then, market growth will continue to rely heavily on primary extraction.

Europe’s policy response

To address these vulnerabilities, Europe has committed to a strategy of selective reindustrialization. The Critical Raw Materials Act sets ambitious targets for 2030: 10% domestic extraction, 40% processing within Europe, and a maximum dependency limit of 65% on any single third country.

The European Commission has already identified 47 strategic projects across 13 member states, representing total investment needs of approximately €22 billion. These projects cover extraction, processing, and recycling. At the same time, the ResourceEU plan, adopted in December 2025, aims to mobilize around €3 billion in public funding to de-risk projects, coordinate procurement, support strategic stockpiling, and accelerate investment decisions.

Despite these initiatives, it is clear that Europe’s supply security strategy cannot rely solely on domestic production. As a result, the European Union is multiplying cooperation agreements with countries possessing key resources or refining capacity, including Canada, Australia, several countries in Latin America and Africa, as well as Indonesia for nickel. These agreements aim to facilitate investment and harmonize environmental and social standards. In parallel, some member states are investing directly in mining or refining projects outside Europe in order to secure industrial supply contracts.

The rapid growth of the European electric vehicle market reflects a structural trend, but it also highlights vulnerabilities linked to the supply of critical materials. Securing access to these resources, together with developing recycling capacity, will be decisive in sustaining this transition. In this context, the energy transition is emerging both as an issue of sovereignty and as a long-term investment opportunity.