Euro money markets: calm under scrutiny

23 MAR, 2026

We speak with Daniel Bernardo, Co-Head of Money-Market Strategies at Ofi Invest AM, about the evolving macroeconomic landscape, central bank policy divergence, and how these dynamics are shaping money-market fundamentals and investment strategies as 2026 unfolds.

What is your take on money-market fundamentals as 2026 begins?

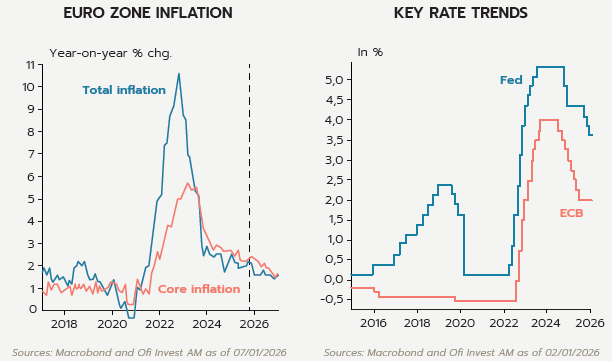

The European Central Bank (ECB) appears to have reached a point of equilibrium, with euro area inflation stabilizing close to the 2% target and an easing cycle that unfolded in 25-basis-point steps and ended in early June 2025. However, escalating geopolitical tensions are making macroeconomic assessment more complex. Inflationary pressures could resurface if the war in Iran persists, which is why market scenarios now factor in a first rate hike movement around mid-June. In this context, we are maintaining our cautious stance: controlled and contained interest-rate sensitivity, no hedging on short maturities, and an opportunistic approach beyond three months depending on carry.

In the US, market has postponed the first rate cut of the Fed. We share the view that rate cuts could be delayed or even compromised this year if a longer-than-expected closure of the Hormuz Strait, through rising energy prices, were to delay the return of inflation to target. Meanwhile, the Bank of Japan (BoJ) is likely to raise its rates further this year but while taking a characteristically highly cautious approach.

At this stage, steady growth and controlled inflation are not at risk, but a prolonged conflict could change the picture. In an alternative scenario of stagflationary environment, central banks would face a real headache in trying to manage the situation.

How are Ofi Invest AM’s money-market strategies designed?

Managing over €16 billion¹ in money market strategies, Ofi Invest Asset Management is positioned as one of the key players in this segment in France. We design our money-market funds with most geographical allocations above 50% for France for various reasons, such as the depth of the Bank of France’s statistics and greater liquidity. Other investments are allocated to other euro zone and OECD countries.

We are nonetheless keeping a close watch on changes in US Federal Reserve policy, as that could influence the ECB, but this has no direct impact on how we manage our investments on a day-to-day basis. The cash that we manage is in euros.

As for types of emissions, money-market funds generally track the market structure. According to the Bank of France, 60% to 70% of issues in the short sections of the curve are from the banking sector, 15% to 20% are from non-bank corporates, and 6% to 10% are from quasi-public issuers.

Banking sector yields are key to performance

So, yields on offer in the banking sector are the main driver of funds’ performance. When a fund is weighted more than 50% on France, this is due mainly to the predominance of French banking issuers. In practice, our banking investments are mainly in maturities of about 1 year and less so in the 1-3-month segment. Bank issuance is in very-short (1 to 3 days) and long (greater than 200 days) maturities. Non-financial issuers² fall between 10 and 100 days. Ultra-short paper (overnight/ tom-Next) ensures daily fund liquidity; longer maturities provide yield.

On each money-market fund, whether short-term or standard, we maintain a bond allocation of various sizes, as we have noted that during market stress, liquidity is sometimes better in bonds than certain money-market issues. Bond issues may amount to about 2 billion euros, making selling easier. If the premium is several basis points in favour of bonds, we lengthen the maturity to capture that liquidity and the potential yields.

As part of these strategies, it is important to keep in mind that investing in a money market or short-term fund differs from investing in deposits and may fluctuate in price. Bond investments are exposed to interest rate risk, credit risk, counterparty risk, and the risk of capital loss. Bonds that provide higher income generally carry a higher risk of default.

What role do extra-financial criteria play in your money strategies?

Extra-financial criteria have altered money-market managers’ scope of action. A few years ago, we invested more in US and Canadian banks, but our investments are now hinged on extra-financial ratings. At Ofi Invest Asset Management, we have long excluded exotic banks (Qatar, China, and Dubai/ Middle East) and securitisations.

In addition to our management strategies, we stand out in our determination to offer a money-market range in which all funds are certified by the official French ISR³ (socially responsible investment) label in its latest (V3) version. The V3 ISR is more demanding, with exclusions expanded from 20% to 30%, the switch to best-in-universe from best-in-class, and monitoring of Principal Adverse Impacts (PAI)⁴ indicators, which has discouraged some other market participants.

────────────────────

¹ Source Ofi Invest Asset management at end-2025

² A non-financial issuer is an issuer of short-term debt carried out by a non-financial company.

³ Established in 2016 by the French Ministry of the Economy and Finances, the ISR label aims to identify investment funds that are managed in accordance with ESG (environmental, social and governance) criteria.

⁴ Principal Adverse Impact (PAI) indicators are standardised measures defined by the European Union under the Sustainable Finance Disclosure Regulation (SFDR). They are used to assess and report the main negative impacts that an investment may have on environmental, social and governance (ESG) sustainability criteria.

IMPORTANT NOTICE

This marketing document has been produced by Ofi Invest Asset Management, a portfolio management company (APE code: 6630Z) governed by French law and certified by the French Financial Markets Authority (AMF) under n° GP92012, with EU VAT number FR51384940342. It is a société anonyme à conseil d’administration [joint-stock company with a board of directors] with share capital of 71,957,490 euros and its registered office at 127-129, quai du Président Roosevelt 92130 Issy-les-Moulineaux, France. It has been entered into the Nanterre, France Registry of Trade and Companies under number 384 940 342. This document is not to be construed as a form of prospecting, nor as any offer to buy or sell financial securities or instruments. It contains information and quantified data that Ofi Invest Asset Management regards as well-founded or accurate on the date they were produced. No guarantee is offered as to information or quantified data drawn from external sources. The analyses presented herein are based on the assumptions and expectations of Ofi Invest Asset Management as of the production date of this document. These may fail to be realized fully or partially on the markets. They do not constitute a commitment to returns and are subject to change. The value of an investment may fluctuate upward or downward and may vary with shifts in exchange rates. Because of the state of the economy and general market risks, no guarantee is given that the products or services presented can achieve their investment objectives. Past performances are not a reliable indicator of future performances. Ofi Invest Asset Management may not be held liable for any damages or losses resulting from the use of all or part of the information contained herein.

The portfolio management company may decide to terminate the provisions governing the distribution of the fund in accordance with Article 93a of Directive 2006/65/EC.

A comprehensive and detailed list of the risks associated with the funds mentioned in the above list can be found in the full prospectuses and key information documents, which are available in French and/or English on the website www.ofi-invest-am.com under the heading "Our Funds".

Further information on investor rights or complaints can be found on the "Investor Rights" page, available in English and French on the website https://www.ofi-invest-am.com/pdf/ofi-invest-AM_investors-rights.pdf .

For regulatory information please visit: https://www.ofi-invest-am.com/en/informations-reglementaires. These documents are available in English.

LU26/009183/300828 / FA26/0766/M