Finding the AI winners while others chase the hype. Nick Evans, Polar Capital on what’s currently crucial in the sector

12 JAN, 2026

Nick Evans, Partner at Polar Capital, has over two decades of experience investing in the global technology sector. He has led the Polar Capital Global Technology Fund since 2008 and is also a fund manager on the Polar Capital Technology Trust and the Polar Capital Artificial Intelligence Fund. Having managed technology strategies through multiple market cycles, Nick brings a deep, long-term perspective on disruption, innovation and value creation in technology. In this interview, he shares his views on navigating rapid technological change, identifying AI winners, and positioning portfolios for the next phase of the AI-driven cycle.

What is your approach to investing in the technology sector, given it is so fast-moving, and disruption is common?

Rapid technological change plays to our strength and experience as one of the largest technology investment teams globally, with 11 dedicated portfolio managers/analysts. We conduct around 1,000 company meetings a year, which speaks to the depth of our coverage. One of the most significant factors is we also have eight years unmatched experience managing a dedicated AI fund which has shaped our investment perspective and focus while giving us invaluable insights.

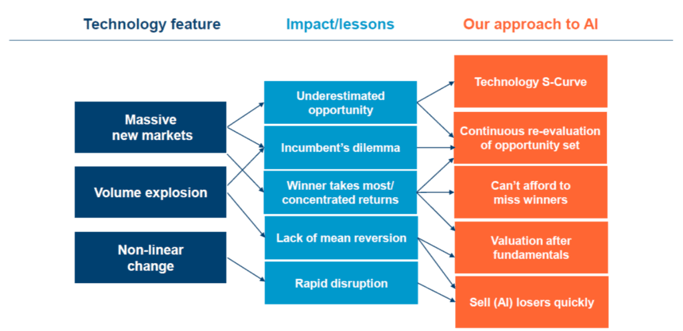

Our experience of previous technology cycles has allowed us to develop a blueprint for technology disruption. We look for technology companies exposed to structural, secular trends, which have long-term growth potential as disrupters. We seek those inflection points in adoption along the technology S-Curve, avoiding the hype stage and focussing on technologies with strong, growing demand which are creating widespread and non-linear change.

Given that we believe AI is poised to become the next General-Purpose Technology (GPT) – potentially disrupting all sectors and businesses – each theme and portfolio holding is now considered through an AI lens, to help identify potential winners (enablers and beneficiaries) and, equally importantly, avoid losers.

We are also increasingly leveraging AI in our own investment process in a way we feel is beginning to contribute to performance. We have enhanced our detailed quantitative screens and technical analysis with qualitative AI scoring models which analyse the filings and transcripts of 2,500 companies weekly – this is already adding new stocks to our investment pipeline. We are also extensively leveraging AI to make our investment process more efficient. The most exciting part is that as AI model performance has improved over the past three-six months we have seen much improved results. We plan to lean into this, investing materially more in AI to make this an additional competitive differentiator in 2026 and beyond.

You describe yourselves as ‘AI maximalists’ - can you explain how the Fund is currently positioned and how positioning has shifted over the last 18 months to reflect your conviction in AI?

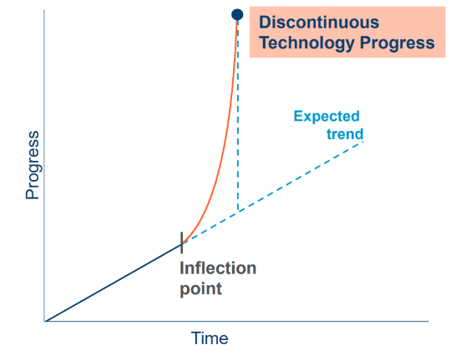

We believe Generative AI is a textbook example of discontinuous technological progress. These are extremely rare moments characterised by radical innovation that fundamentally change how industries operate, also leading to the creation of entirely new (current invisible, hard to imagine) market opportunities. These are typically underappreciated and unpredictable because decades of progress are packed into short time periods, but once proven, rapid adoption follows.

Discontinuous technological progress is the most important concept for investors to understand and is not widely discussed. It explains why the AI Bubble discussion is likely premature, because the majority of investors don’t appreciate just how quickly AI will transform almost every industry. It adds perspective to why those with the best perspective of the AI roadmap, particularly US hyperscalers, are investing aggressively. This is why AI capex has surprised materially to the upside the last two years and will likely do the same in 2026 and 2027 supporting robust growth for the enablers.

The nature of discontinuous progress

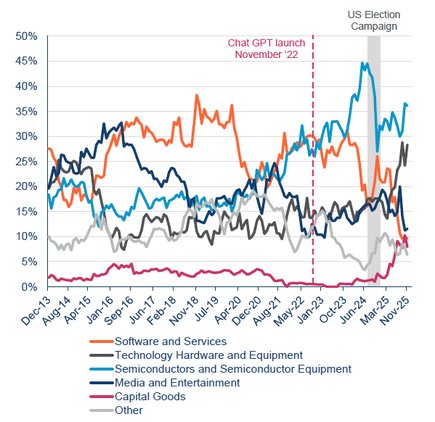

We know from previous cycles that avoiding losers is critically important. As a result, the Fund’s exposure to software (less than 10%) is the lowest it has been in a decade, given the existential threat that AI poses to software development. Instead of investing in software companies, we have been investing in broader AI enablers (compute, networking, fibre, memory etc.).

Sector breakdown (2013-25)

The Fund is also underweight the Mag-7 in aggregate as a two-way debate is emerging about which will be the winners from AI. That said, the risk of being materially underweight is partially mitigated through selected use of out-of-the-money call options.

The capex spending to support AI demand remains a key investment driver. Yet demand is still outpacing supply including beyond data centres. Our active, off-benchmark approach has led us to some secondary investment opportunities in power generation, grid expansion, cooling technologies and efficiency enablers.

AI is clearly going to disrupt the status quo; challenging the incumbency of Big Tech and changing subsector dynamics. How do you avoid the AI losers whilst identifying the AI winners, both at a subsector and company level?

Discontinuous technological change also explains the widening AI-led disruption that is occurring with many previous winners, quality growth or compounders in all sectors struggling. This is particularly obvious within tech with software companies having been under pressure for several years, but 2025 saw the pain expand into many other sectors. Those hoping that pressure will ease in 2026 will likely be mistaken because new AI models will drive improved performance and accelerate the pain for those on the wrong side of this trade.

Once you understand this, it becomes clear a new portfolio is going to be required. AI demand is exceptionally strong and while most companies are talking a good game, the market is rewarding those who are delivering.

Avoiding value traps is a key part of our investment process. Experience tells us it is too easy to underestimate the disruptive nature of new technology cycles and as a result generalist-investors often fail to appreciate the challenges facing many supposedly ‘cheap’ incumbents (often large constituents in cap weighted indices).

We think that ‘incumbents’ often appear most attractive on free cash flow or ‘value’ based metrics just before they go into secular decline – creating a significant challenge for generalist or benchmark orientated investors. We believe our growth-centric approach and experience through several market cycles can help us avoid value traps.

Given you are a single sector, thematic fund, how do you construct a diverse and risk aware portfolio?

A more selective approach is required as the market is starting to discern which companies are AI winners (enablers or beneficiaries) and which are at risk of being left behind. We believe active management is key to capturing the opportunities here.

We manage risk and volatility by delivering a diversified portfolio of profitable growth companies, rather than by measuring tracking error relative to an inappropriate benchmark.

The team use deep out-of-the-money NDX (NASDAQ) Index put options to soften the beta of the portfolio, which reduces the volatility of the Fund and the downside risk during a sharp (often unexpected) market sell off. This enables us to remain more fully invested and maintain our growth-centric investment approach even when the outlook for broader equity markets weakens.

Rapid pace of innovation requires a liquid portfolio, so the management of liquidity is an important part of our portfolio construction. In fact, in this market you do not just need active management, but rather ‘reactive’ management, that is an investment team used to quickly adjusting to change. If you have a low turnover approach, even if you do appreciate the scale of the AI-led change ahead, it will be difficult to react quickly enough. This is why we have always had a strong focus on liquidity, and it has allowed us to pivot the portfolios towards AI rapidly and materially contributed to the Fund’s recent performance.

Are you comfortable with current valuation levels within the technology sector?

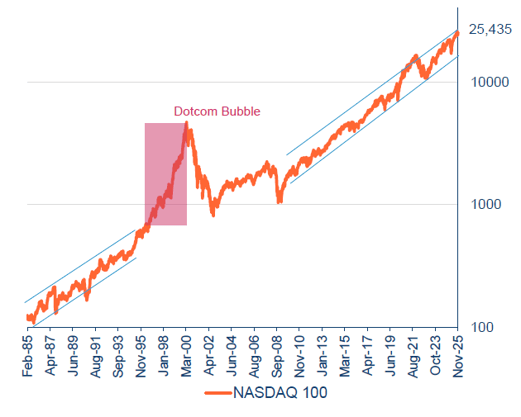

There are certainly pockets of exuberance in the market, but we do not think valuations are stretched versus history. In the dot.com bubble of 1999-2000, the technology sector traded at above 2x the market multiple. It is currently trading at around 1.3x. While valuations are not cheap, and further volatility should be expected (an uncomfortable but normal feature of new cycles), technology-related shares can still perform strongly if, as we expect, growth remains robust.

NASDAQ 100 performance

It is also important to remember that volatility is a normal feature of new technology cycles. Between 1995-1998 – the early years of the internet infrastructure build-out but before the dotcom bubble – the NASDAQ gained 354%. However, this strong period was punctuated by seven corrections of greater than 15% during the period. We believe the current backdrop remains highly reminiscent of the mid, rather than late 1990s.