Marie-Christine Lambin of Bolero Capital Sàrl is our Advisor of the Month

20 MAR, 2024

By Jose Luis Palmer from RankiaPro Europe

Marie-Christine is founder of a consultancy boutique providing proprietary macroeconomic research, global asset allocations models and fund selection to professional investors, including family offices and independent asset managers. With over 30 years’ experience in asset management, Marie-Christine has developed a strong expertise in multi assets portfolios. She started her career in Luxembourg where she served HNWI with major international banks (Banque Paribas, ING, Safra) and has been a main contributor to the step-up and development of centralized discretionary portfolio management and the launch of open fund architecture. She also worked for a family office in Geneva as investment strategist and lead fund manager of a Global Equity and Global Allocation fund. In 2013, she launched a multi-assets UCIT fund which she managed until May 2019 with a flexible and dynamic approach. Marie-Christine graduated from the Catholic University of Louvain-la-Neuve (Belgium) and received several recognitions during her career: Investment Manager of the Year 2015 (Luxembourg for Finance); Wealth Manager of the year 2016 (Luxembourg for Finance); Manager of the year Luxembourg 2016 (The European Magazine), she has been featured by Sharing Alpha as Top Fund Selector 2019 ,Top Allocator 2019 (bronze medal), 2020 (gold medal), 2021 (bronze medal).

What made you decide to go into the financial sector? Did you have any other vocations?

My journey into the financial sector was driven by a combination of curiosity, opportunity, and a desire for personal growth. Starting as a teacher and translator, I initially pursued a career path focused on education and languages. My transition to a job in a bank opened doors to an entirely new world: private banking. As I delved deeper into the private banking realm, I found a passion for financials markets and recognized the potential to leverage my analytical capabilities in this field. Driven by a desire to excel in a new domain, I embarked on a journey within asset management. My career pivot ultimately led me to a fulfilling and rewarding career in asset management, from discretionary portfolio management for HNWI to fund management. Two years ago, I set-up an independent research firm providing global macro analysis, investment strategy, asset allocation, model portfolios and fund selection for professional investors, including family offices and independent asset managers.

What does a typical workday look like for you? How do you organize your time?

My early morning dive into the world of financial analysis and asset allocation begins with a review of portfolios performances against relevant benchmarks and objectives. This critical assessment allows me to identify potential discrepancies or any areas requiring attention or adjustments.

Then I immerse myself in the global financial landscape with a review of Asian markets and the monitoring of European and US markets, including economic indicators, interest rate movements, corporate news and geopolitical events. With the LSGE/Refinitiv platform, I have access to all data and information necessary to shape my investment strategy. Simultaneously, I conduct a broad review of my fund universe consisting of over 300 funds, comparing performance, volatility, risk/reward, consistency of returns and ESG scores. The aim is to detect any deviations from market trends. Evaluating whether a fund behaviour aligns with its strategy. Understanding why a fund diverge from market trends is essential for effective risk management. This analytical process allows me to optimize the portfolio construction that best fit my asset allocations views.

My day also includes a series of meetings with fund managers, either through Zoom/Teams or in-person sessions. These engagements range from introductory discussions to follow-ups on ongoing collaborations. Additionally, I attend international conferences, maximizing opportunities to interface with multiple fund managers within condensed timeframes. These interactions are invaluable, enabling informed decision-making based on firsthand insights from industry experts.

Amidst my busy schedule, I maintain proactive communication with clients. Overall, my day as a consultant is characterized by meticulous analysis and proactive client engagement, all aimed at delivering one-stop solutions with optimal outcomes.

Which portfolio allocations are most interesting in the current market situation?

I believe that in 2024 equities should perform better than bonds. Baring a severe recession or a sharp increase in the US 10y Treasury yield (above 5%), equities should remain supported by resilient economic data and an uptick in corporate earnings. A soft-landing scenario is gaining steam, supporting the case for equities. The US economy has remained remarkably resilient despite the Fed's most aggressive tightening campaign in decades. A slowing but still strong labour market is underpinning consumer consumption and hence economic growth. In Europe, the worst of the economic slump is probably over although growth this year is likely to remain sluggish. Corporate earnings have globally been better than expected. Balance sheets have remained strong, margins have held up well as companies were able to pass on higher prices to customers. Still, downside risks persist. Recent speeches from central bankers confirming that rate cuts will be less pronounced than originally anticipated remains a source of potential disappointment and hence volatility in the markets. If inflation continue to surprise to the upside, the risk is rising for a delay in the start of the policy easing to September, with the central bank reducing the number of rate cuts in 2024 to two. This compares with 72 bps rate cuts priced in for 2024. A stabilization and convergence in market assumptions about rates anticipations should ultimately mitigate long term interest rate risks for equities.

With a 12 months view, a 65/35 portfolio should work well for investors with a moderate risk profile. A 100% equities portfolio look appropriate for less risk adverse investors.

I maintain a preference for developed equity markets (US, Europe, Japan) over emerging markets. Valuations in the US may appear expensive with the S&P 500 currently trading at a 12mth forward Q4 P/E ratio of 21.2x, above its 10Y average of 17.3x. However, there is a large disparity between a select group of mega-cap tech stocks (the Magnificent Seven”) and the vast majority of US large and mid-caps which are more fairly priced. Europe looks more attractive at an aggregate level with the STOXX 600 currently trading at a forward PE of 13.0x, below its 10y average of 14.4x. The average PE however is masking a huge disparity among sectors, with low PE in banks, utilities and autos and more elevated ones in Technology, industrials, consumer discretionary. Lower competitiveness and higher dependency global trade justify a lower valuation compared to the US in my view.

I maintain an Underweight in global emerging markets. As far as I am concerned, China has been un-investible for quite some time, not only from an ESG prospective but also from a fundamental point of view. China slowing economic growth and disinflationary trends are raising the prospects of “Japanisation”, a prolonged economic slump that afflicted Japan after an asset bubble imploded in the 90’s. Moreover, President Xi Jinping’s autocratic rules have undermined the trust of Western partners and customers of Chinese firms. India looks more attractive as the country is entering a period of self-sustaining expansion as prior reforms create a virtuous cycle of growth. A young population, the country’s trend towards urbanisation, improved economic management with greater corporate capital expenditure create huge potential. Demand is rising demand for financial services, infrastructure investment and the green transition.

Still, convictions may be tested this year as we still must figure out how the world will adapt to higher rates. Companies – and in some cases, entire countries -- will have to restructure their debt liabilities, as they can no longer afford to pay interest. A new era of higher interest rates will require tighter fiscal policies to address the gradual increase of the debt burden as debt is refinanced, which may weigh on consumption and hence growth. There is also much uncertainty about the impact of diversification of global supply chains on inflation and economic prospects. The energy transition will take years to play out with likely inflationary pressure over the near term and increased burden on households. Risks to the 2024 outlook also include two major wars, heightened geopolitical tensions that have put globalization firmly in reverse, and elections in several countries that could radically change the world order in unexpected ways. Higher rates underpin everything, from economic growth to the price and valuation of financial assets.

In the fixed income segment, I recommend being flexible in terms of credit quality and duration. I have long cautioned against excess optimism in the markets about central banks’ pivot. Resilient economic data are fuelling the risk of a resurgence in inflationary pressures and a delay in rate cuts, hence our cautious stance on the long end of the curve. Our prediction at the start of the year that the euphory triggered by hopes of swift rates was overdone, proved to be right. Yields on the 10y yields are creeping up again as markets are scaling back their bets on central banks’ rate cuts amid signs of stick inflation largely supported by strength in the services sector and rising wages. At the time of writing (a day before the March Fed meeting) the two-year Treasury yields stands at 4.72%, and the 10-year yields at 4.32%. Ongoing labour market strength could make the Fed worry of cutting rates in a re-accelerating economy with the potential for the 10YT yields to rise to 4.5%-5% again, hence my Underweight in long duration government bonds.

To mitigate the risk of higher rates, I continue to focus on short duration bonds, mainly developed corporate Investment Grade and High yield that offer attractive carry. In the emerging debt, I have an overweight in Corporate IG due to lower duration compared to sovereign bonds and higher credit quality.

Which sector do you consider particularly interesting at the moment?

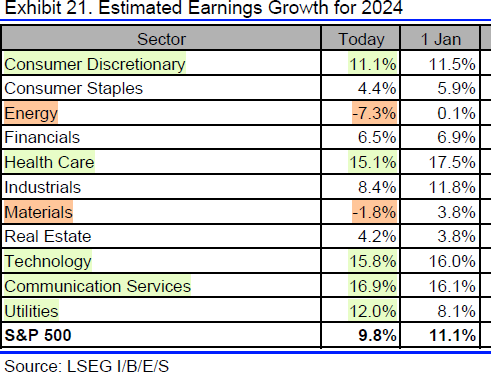

A soft-landing scenario looks favourable for late-cycle cyclicals such as industrials and healthcare. Consumer discretionary and communication services should also perform well. Higher rates for longer will continue to support low-leveraged stocks like technology. The Ai related stocks however look vulnerable to a correction after the dramatic run over the past 12 months. Long term potential however remains intact. Many strategists expect small caps to perform well this year after two years of underperformance. We remain reluctant to be constructive on this segment as long as uncertainty remains about central banks’ policies. Small caps tend to be high growth stocks with relatively high leverage. In green below, US sectors expected to deliver earnings growth above the S&P500 average.

How should investors orient their portfolios in the current environment?

Current economic conditions are part of a shifting trend from globalisation to regionalisation. Due to rising geopolitical risks around the globe, Western countries are perceiving the need for reshoring and securing supply chain from neighbouring and friendlier countries. In this context of rising fragmentation, I think it makes sense to invest in pure building block in terms of region/country and sector allocation in a bid to better identify opportunities and risks. In terms of style, a GARP (growth at reasonable price) approach looks appropriate in a soft-landing scenario.

What characteristics do you think a good financial advisor should have?

A good financial advisor, especially one servicing institutional and professional clients should possess a diverse set of characteristics to effectively meets the demands of the role, including technical expertise, solution-driven abilities, flexibility, communication skills and ethical integrity. Strong analytical skills are necessary to evaluate investment opportunities, assess risks, and develop appropriate financial strategies tailored to clients' needs and goals. A deep understanding of financial markets, investment products, risk management techniques, and financial planning strategies is essential. Understanding clients' goals, risk tolerance, and investment preferences is key to providing tailored advice and solutions. Consultants must be able to articulate investment strategies and rationale with clarity and confidence. Confidence in one's abilities is important, but it should be balanced with humility and openness to feedback and continuous improvement.

Flexibility is also key. Financial markets are dynamic and often present unforeseen challenges. A good consultant should be able to think critically to adapt strategies as needed and guide clients through periods of uncertainty. Continuous learning and staying updated with the latest trends and regulations in the financial industry are also crucial. Ethical conduct is paramount. A good financial consultant must act with honesty, transparency, and integrity, always putting clients' interests first and avoiding conflicts of interest.

When you have free time, what do you like to do?

My second passion next to finance is scuba diving and underwater photography. I discovered scuba diving in Egypt more than 20 years ago and have since travelled around the world in search of these uncredible creatures that inhabit seas and oceans. Whether big (like mantas, sharks, turtles, napoleon fish) or smaller (clown fish, nudibranchs, pigmy shrimps) they always provide exciting experiences, that I like to memorize with pictures and videos.

My deep dive into the blue goes hand in hand with my deep dive into macro analysis. Protection of the ocean and biodiversity preservation are key for the future of our planet.