Bond markets call a re-convergence of US and European monetary policy

9 MAY, 2023

By Gilles Möec

Christine Lagarde sounded non-plussed when asked during the Q&A about the diverging trajectories of the Fed and the ECB. The Governing Council seems to be comfortable with this, and the market is indeed – for the short-term – convinced that the two central banks will indeed diverge, at least when looking at forward contracts on the money market. In contrast with the US where rate cut pricing has gone in overdrive since last week, in the Euro area, a terminal rate between 3.50 and 3.75 for July followed by stability until the end of the year is expected.

This pricing is in our view completely justified by the signals coming from the ECB, and we mentioned in the first section of this note our own baseline of two more 25 bps hikes. But this is the result of our predictive analysis – what we think the ECB will do. From a normative point of view, what we think the ECB should do, we are circumspect about the absolute need of pushing policy rates higher, and we take the risk that they go too far seriously.

True, even if the ECB hikes up to 3.75%, the overall rise in policy rates from the trough would be smaller (4.25%) than in the Fed’s case if it stops here (5%). Yet, evidence of excess demand is more plentiful in the US than in the Euro area, which for instance is not dealing with a lingering labor supply deficit – the participation rate rose there – and was more measured in its fiscal stimulus efforts. A significant gap thus looks legitimate. A popular view considers that given the ECB’s extremely accommodative starting point – while the Fed never ventured into negative rates – it’s normal that it would still have more “ground to cover”. Our view on this has always been quite simple: the difference in potential GDP growth between the US and the Euro is routinely estimated at 0.5 percentage points (c.1.25% versus c.1.75%), which would be consistent with a gap in the equilibrium interest rate of also 50 bps. That at the worst of the deflation risk the ECB’s policy rate stood at -0.5% against 0-0.25% for the Fed would thus stand to reason and did not reflect a particular “dovish bias” at the time by the ECB which would need to be offset now.

The ECB’s clear preference for continuing to raise rates is deeply rooted in the absence of clear signs of deceleration in core prices, in contrast with the US. The root cause of the divergence in inflation dynamics across the Atlantic should however matter for monetary policy setting. Price stickiness can mean very different things. In one configuration, “sticky prices” reflect a low sensitivity of prices to changes in macroeconomic conditions. In another, they simply reflect a slow adjustment speed (in clear terms, it takes a while, but we will finally get there). The latter could merely be due to different modes of organization of consumer goods markets, or to the transmission lags of monetary policy.

In the first case, the policy recommendation is straightforward: monetary policy needs to be tougher, to bring about a large enough deterioration in aggregate demand which will finally bring inflation where it should be. This would be consistent with Christine Lagarde’s message on monetary conditions not being restrictive enough yet. The second case simply calls for patience, at least as long as long-term inflation expectations are not de-anchored. Deciding between the two cases is difficult in real-time, but it seems that for now, the ECB is more focused on case 1 than case 2.

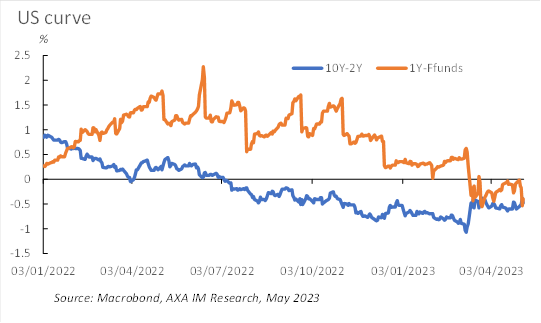

The ECB is worried, which makes it impatient, but if it’s only a matter of time before core inflation slows down, then the risk of policy overshooting is high. This is what the bond market may already be pricing. If instead of looking at forward contracts on the money market to gauge the market pricing of the next central banks’ decisions, we look at the bond market, then the gap between the yield on a one-year government bond and the ECB’s and Fed’s policy rate is intriguingly close, at c.50 basis points. It may come a bit later, but ultimately the market’s collective wisdom signals that the ECB will be forced to cut rates in a context of recession. Further, into the curve, we note that the 10-year to 2-year spreads have also become very similar across the Atlantic. This is normally associated with the market pricing during a recession.

Exhibit 9 – The shape of the yield curve…

Exhibit 10 – …is getting very similar across the Atlantic

What the bond market may be simply reflecting is that if a recession is now very plausible in the US, it would be very difficult for the Euro area – which has become even more reliant on net exports these last two quarters – to avoid one as well. With a US recession, global disinflationary forces will be at work – e.g., on the energy front – helping to dampen domestic inflationary forces in the Euro area.