The ECB meets this week. What can we expect?

Updated:

16 DEC, 2025

By Joanna Piwko from RankiaPro Europe

This week's meeting of the European Central Bank is shaping up to be crucial for investors and markets. The market appears to be in agreement that the ECB will keep rates unchanged.

Konstantin Veit, Portfolio Manager at PIMCO

At its next meeting on Thursday, we expect the ECB to keep the deposit rate unchanged at 2% for the fourth consecutive time. This level is widely regarded as the midpoint of a neutral policy range in the euro area by the majority of Governing Council members.

Inflation remains close to target and growth is resilient, supporting the decision to leave monetary policy unchanged.

Governing Council members broadly agree that the risks to the medium-term inflation outlook are balanced, although views differ on the short-term policy implications. While some members see upside risks over the medium term, others emphasize downside risks over the next two years, leaving the Governing Council divided between those who consider the rate-cutting cycle to be over and those who remain open to further cuts.

We believe the ECB will prioritize preserving conventional policy space and will look past modest deviations from the target, rather than engaging in fine-tuning of monetary policy.

In our baseline scenario, we expect policy rates to remain unchanged in the near term.

Martin Wolburg, Senior Economist at Generali AM (part of Generali Investments)

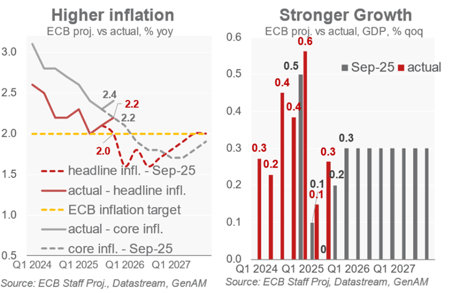

The ECB considers itself to be in a “good position” after cutting its policy rate to 2.0% in June, but markets have been speculating about whether below-target inflation in 2026 could trigger another rate cut. However, at the December 18 meeting, the Governing Council (GC) is facing a surprisingly resilient economy and higher-than-expected inflation.

The latest indicators point to a continued recovery, and President Lagarde suggested that the growth forecast (1.2% / 1.0% / 1.3% for 2025/26/27) could be revised upward. Together with comments from ECB’s Schnabel that the next policy move could be a hike, markets have begun to price in higher interest rates in 2026.

That said, in Q1 2026, strongly disinflationary energy prices and moderating wage growth throughout the year are expected to keep headline inflation below target. In addition, a stronger euro and the diversion of Chinese exports toward Europe will exert disinflationary pressure.

In their remarks, Executive Board members have repeatedly stressed the need to look through inflation volatility. In our view, it is unlikely that the macroeconomic projections extended to 2028 will show a persistent inflation shortfall.

Therefore, we believe the ECB continues to view the policy rate as being at a “good level”, namely at the center of the neutral policy range. We agree and expect the ECB to remain in hibernation for the time being.

Annalisa Piazza, Fixed Income Research Analyst at MFS Investment Management

It is unlikely that the ECB will alter market expectations at its December meeting, as the economic backdrop has shown signs of stabilization. While GDP growth across the major euro-area economies remains uneven, the overall picture is less sluggish than previously feared. Medium-term inflation is expected to stabilize around the 2% target, with projections for 2028 slightly above this level. The ECB appears ready to maintain its current policy stance, with no immediate changes to interest rates. Given that the euro-area economy is showing signs of resilience and inflation is on track to reach its medium-term target, the central bank is likely to adopt a “wait-and-see” approach.

Nevertheless, risks to growth and inflation persist. Trade uncertainties with the United States and China, together with their potential impact on lower investment and more cautious consumer spending, could weigh on the outlook. Recent data, such as the contraction in German exports to the US and China, highlight the fragility of trade dynamics. Markets have also experienced notable volatility in recent weeks, exacerbated by tighter liquidity conditions. The euro-area yield curve is expected to remain steep, reflecting short-term volatility due to tight market positioning. In addition, upcoming pension fund reforms could influence the shape of the curve as 2026 approaches. A rate cut in early 2026, while not the base case, could materialize if economic growth falters. As the year draws to a close, the possibility of further short-term market fluctuations cannot be completely ruled out.

On the other hand, there are reasons for optimism. Lower policy rates are continuing to filter through to the real economy, and Germany’s fiscal stimulus package is expected to provide a much-needed boost to cyclical activity. In addition, the strength of the labor market and low inflation are supporting real disposable income, which could help GDP growth move closer to its potential in the coming quarters. Recent economic developments have somewhat eased downside risks, supporting the outlook for stable interest rates in the foreseeable future.

The coming months will be critical in determining whether external shocks or unexpected data could tip the balance and prompt a policy shift. For now, the ECB appears comfortable staying the course, navigating a delicate balance between growth risks and inflationary pressures.

Kevin Thozet, a Member of the Investment Committee at Carmignac

Unlike the Fed, markets do not expect the ECB to cut interest rates at Thursday’s meeting. The prevailing narrative is that the rate-cutting cycle has largely run its course and that Europe’s growth momentum now lies primarily in fiscal policy. Some even suggest that the ECB could begin raising policy rates again by the end of 2026.

On 18 December, Christine Lagarde is expected to reiterate the ECB’s data-dependent, meeting-by-meeting approach. The new set of growth and inflation projections to be released at the meeting will likely reinforce this stance.

The forecasts strike back: hawks stretch their wings

The new forecasts will now include 2028 and are expected to show that growth is above potential, closer to 1.4%, and that inflation is at 2% (i.e. at target).

Such projections send a dual message. First, that the region is moving in the right direction. Second, that investors should anticipate a more hawkish policy path ahead.

Growth forecasts are likely to be revised to reflect recent data. Q3 came in stronger than expected, and leading indicators for Q4 have been well oriented. On the inflation front, the final October print and the November flash estimate suggest that projections may be revised around 0.2% higher for the quarter.

By construction—and somewhat paradoxically—both sets of projections are backward-looking, yet they both point towards an improving macroeconomic trajectory. Inflation is still expected to undershoot in 2026, initially due to energy base effects and later due to the long-awaited decline in services inflation. However, wages remain a key source of uncertainty and debate. While ECB and Indeed wage trackers point to a slowdown in wage inflation, Eurostat’s compensation-per-employee data indicates stronger realized outcomes.

The one-year postponement of the new emissions trading system (ETS2) merely delays its upward impact on prices (estimated at +0.25% as allowances extend beyond heavy industry to transport and heating) from 2027 to 2028.

As a result, no major shift is expected in the “ECB is in a good place” narrative. With the periphery holding up and France showing resilience despite limited visibility, the key variable will likely be the Bundesbank projections, which previously (in June) suggested a modest 0.7% real GDP growth for 2026.

Implications for fixed income markets

Given this balanced outlook, we do not expect the ECB to cut—or hike—on 18 December. Inflation for 2026–2027 is expected to remain below target (1.7%–1.8%), while policy rates at 2% sit in the middle of the estimated neutral range.

This configuration leaves the ECB with a policy “put”, which can be readily activated should growth falter or markets shift toward a risk-off stance.

Against this backdrop, euro short-term bonds appear attractive. They offer modest carry and asymmetry, namely capital appreciation potential should policy rates be cut at a time when markets are pricing very little on that front.

Michael Krautzberger, Global Chief Investment Officer for Fixed Income at Allianz Global Investors

We do not expect a rate cut at the ECB’s next meeting on 18 December.

The pickup in growth and inflation very close to target currently place ECB monetary policy in an appropriate position.

In this context, we maintain a short position in the euro against a basket of pro-cyclical Asian currencies.

Euro-area central bankers continue to enjoy a “comfortable position.” Unlike their counterparts in the United States, the United Kingdom, and Japan, who face persistent inflationary pressures, or the Swiss National Bank, which is dealing with inflation that is too low, European inflation has remained close to target for several months. Growth has also surprised to the upside: euro-area GDP rose by 0.3% in the third quarter, well above the ECB’s 0.0% forecast. In addition, the labor market remains strong, suggesting that the economy is operating close to potential.

Against this backdrop, we do not anticipate a further rate cut at the upcoming ECB meeting. The October minutes show that several Governing Council members favor looking through small deviations from the inflation target and reserving monetary policy adjustments for more significant shocks. Even traditionally dovish voices, such as Fabio Panetta (Bank of Italy) and François Villeroy de Galhau (Banque de France), have refrained from calling for rate cuts recently. While adjustments cannot be ruled out, the ECB also appears unwilling to contradict market expectations, which currently view a rate hike as more likely than a cut.

That said, there may be room for a rate cut in the first half of 2026. Headline inflation could fall to around 1.5% in the first quarter, largely due to energy base effects. Wage growth has declined below the 3% threshold, consistent with the 2% inflation target, and both ECB indicators and our own analysis suggest it will remain at these levels. From a structural perspective, the euro-area economy remains about 5% below its pre-pandemic trend, raising questions about weak demand and long-term growth potential.

Despite this, short-term prospects show some improvement. The effects of recent shocks—such as the energy crisis and the ECB’s tightening cycle—are fading, and Germany’s ambitious infrastructure investment plan could extend the EU-funded investment impulse from the periphery to core economies. In Spain, the best-performing economy in Europe, signs of a potential inflation rebound are beginning to emerge, although this is likely to be offset by persistent price weakness in France. Absent new external shocks—such as major changes in US trade policy or episodes of financial market volatility—the window for another rate cut could close quickly, reducing the likelihood of a rate cut in 2026.

As investors, we currently hold a short position in the euro against a basket of pro-cyclical Asian currencies (AUD, NZD, KRW). China is exporting disinflationary pressure to Europe, weighing on competitiveness and limiting expectations for ECB policy easing in 2026. At the same time, resilient global growth, reduced tariff risks, a supportive political environment, and the undervaluation of these currencies create a more favorable backdrop for Asian currencies over the coming year.

Nomura

We expect the ECB to leave the deposit rate unchanged at 2.00%.

We expect the ECB to keep its quantitative tightening guidance unchanged for the APP and PEPP portfolios (i.e., full runoff).

We expect President Lagarde to emphasize that the ECB is well positioned with rates at their current (i.e., neutral) levels to deal with the current uncertainty stemming from US policy.

We do not expect the ECB to provide any guidance on the interest-rate path, but rather to continue emphasizing data dependence and its well-communicated reaction function: (1) the assessment of the inflation outlook; (2) underlying inflation dynamics; and (3) the strength of monetary policy transmission.

In the Q&A session (13:45 London time), President Lagarde is likely to be asked about the rate path beyond December. We expect her to suggest that data or economic developments would need to materially lower the ECB’s 2028 HICP inflation forecast for the ECB to cut rates again. Recall that the ECB focuses on the end of the projection horizon: while in September this was 2027, starting from this meeting it will be 2028, and it will remain so until 2029 is added in December 2026.

Lagarde is also likely to be asked about the market repricing following Schnabel’s Bloomberg interview, in which she said she would be comfortable with markets viewing the next move as a rate hike. We expect Lagarde to reiterate that the ECB is in a good place with policy at its current (i.e., neutral) level, that the ECB’s next move will be data-dependent, and that the next move could be either a rate hike or a rate cut. Ultimately, the ECB will take whatever actions and steps are necessary, meeting by meeting, based on the data, to ensure it remains well positioned. We believe markets will interpret this as a hawkish stance.

François Rimeu, Senior Strategist at Crédit Mutuel Asset Management

It is unlikely that the European Central Bank’s (ECB) message will change significantly at its upcoming meeting this week. The ECB is expected to keep monetary policy unchanged and to repeat a message similar to that of previous meetings.

Recent comments by Isabel Schnabel, a member of the ECB’s Executive Board, have reinforced the view that a near-term rate cut is very unlikely. She appears comfortable with current market expectations, which point to no changes over the next 12 months and even assign a low probability to a rate hike.

Our expectations for this meeting:

- The deposit facility rate should be kept at 2%, supported by resilient growth and contained inflation.

- Christine Lagarde is expected to temper market expectations regarding a possible rate hike in 2026.

- She is likely to refer to the ECB’s new macroeconomic projections.

- These projections should point to better-than-expected growth in 2025 and 2026, without signaling inflationary pressures in 2026–2027.

- Lagarde should reiterate the ECB’s meeting-by-meeting, data-dependent approach.

The ECB is expected to highlight a growth outlook that is stronger than anticipated three months ago and to confirm that monetary policy is currently in a good position. Any immediate market reaction following the meeting should be limited, as Schnabel’s comments are already largely priced in. Over the longer term, however, we believe current monetary expectations remain somewhat high given the euro area’s growth potential.

Josefina Rodríguez, Economist at Vanguard

The ECB is expected to keep the deposit facility rate unchanged at 2% at Thursday’s meeting, marking the fourth consecutive decision to maintain a stable monetary policy stance. Stronger-than-expected growth and persistent services inflation have closed the window for a preventive rate cut and reinforced confidence in the current stance. Our baseline projection is that the ECB will keep rates at 2% throughout 2026, a level we consider neutral. However, falling energy prices and the likelihood that inflation will remain below target for much of next year tilt the risks more toward policy easing than tightening.

- Recent data: Euro-area GDP grew by 0.3% in the third quarter, with employment rising by 0.2%, driven by Spain and France, while Germany remains stagnant as fiscal stimulus measures have yet to take effect. Inflation followed a similar trend, rising from 2.1% in October to 2.2% in November, mainly due to sticky services prices. Real GDP growth is 0.4 percentage points above the ECB’s September projections, reducing the scope for near-term easing.

- Survey data: The composite PMI reached a 30-month high in November, supported by strong services activity. German manufacturing remains weak, but services continue to offset the drag.

- Global trade: The EU’s trade surpluses increased significantly in September following the trade agreement with the US, pointing to sustained momentum in international trade.

- Energy prices: TTF gas prices continue to fall due to increased US supply and mild winter conditions, while Brent oil prices are also lower. We expect energy prices to decline by 6% year on year in January, contributing to inflation remaining below the 2% target throughout 2026.

- ECB communication: Recent remarks from Governing Council members have reinforced the message that monetary policy is in a “good place.” President Lagarde noted that growth forecasts could be revised upward and emphasized the euro area’s resilience amid global uncertainty. Schnabel said she is comfortable with market expectations that the next move could be a rate hike, while stressing it is not imminent. Nagel described current rates as “almost neutral” and appropriate given stabilizing inflation trends, while Villeroy de Galhau and Simkus echoed the view that keeping rates unchanged remains appropriate for now. Overall, the tone is slightly optimistic, reflecting confidence in the current stance, though members remain alert to downside risks from a potential inflation shortfall.

- Inflation expectations: The 5-year euro inflation swap currently trades between 2.0% and 2.1%, slightly above September levels but below those seen in the summer. Persistently below-target inflation in early 2026 could weigh on expectations, although recent activity strength suggests the window for a preventive rate cut is largely closed.

- Our view: We expect the policy rate to remain at 2%—our estimate of neutrality—through the end of 2026. The ECB appears comfortable with its current stance, supported by solid activity and labor market data. Nevertheless, the risk of a prolonged inflation undershoot means the bias continues to point toward easing rather than tightening.