The fall in oil prices and what it means for credit markets

24 NOV, 2025

By TwentyFour AM

Felicity Juckes, Portfolio Manager at TwentyFour AM

Oil prices have dominated headlines in recent weeks. After falling below $60 per barrel, the price of West Texas Intermediate (WTI) rebounded strongly following newly announced sanctions against two Russian giants, Lukoil and Rosneft. Oil prices matter for several reasons: they drive CPI and PPI inflation, signal aggregate demand, and have a geopolitical component. From the perspective of high-yield investors, rising oil prices can pressure the margins of certain industrial issuers or even trigger a default cycle in regions with a high concentration of exploration & production (E&P) companies.

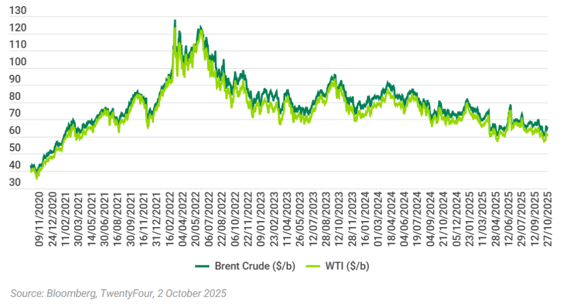

As the chart below shows, oil prices have been declining for some time, and most analysts expect them to remain stable or continue falling through 2026. The global economy is expected to grow a modest 3% this year, but industry remains weaker than services, meaning oil demand is still subdued. The U.S. Energy Information Administration (EIA), for example, expects global supply to exceed demand at a record pace. Weak industrial activity in Europe since Russia’s 2022 invasion of Ukraine has weighed on demand, compounded by China’s slow post-pandemic recovery. In the U.S., tariffs have raised concerns about weaker economic prospects, particularly in manufacturing, and with the typical seasonal winter demand drop, prices could continue to fall.

Chart 1: Falling Oil Prices

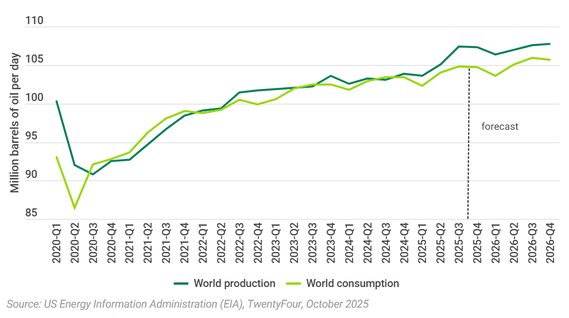

On the supply side, production is rising as OPEC has relaxed production restrictions and several producers have increased activity. The U.S.—under President Trump's “drill baby drill” agenda—along with Brazil, Canada, and Guyana, has contributed to oversupply. The EIA expects global crude oil and liquid fuel production to rise by about 2.7 million bpd in 2025 and 1.3 million bpd in 2026, versus demand growth of only 1.1 million bpd in both years. As a result, global inventories are forecast to increase by 2.6 million bpd in Q4 2025 and 1.9 million bpd in 2026. Banks such as Morgan Stanley and Goldman Sachs forecast Brent at $55–60 in 2026.

Chart 2: Global Liquid Fuel Supply Expected to Outpace Demand

Persistent price weakness would pressure producers’ margins. Below certain break-even thresholds, extraction becomes commercially unviable, leading companies to delay production. Break-evens vary widely across producers and regions: major integrated companies have lower thresholds, while smaller, less diversified operators are more vulnerable. For example, Shell can maintain dividend payments as long as oil stays above $40 per barrel. Ithaca Energy, a BB-rated North Sea producer, targets a break-even range of $30–50, suggesting reduced investment if prices fall below $50. In the U.S., break-even levels differ significantly: the best parts of the Permian Basin have thresholds at or below $40, while more expensive operations like deepwater Gulf of Mexico require over $60 per WTI barrel to stay profitable.

In European high-yield credit, direct exposure to oil remains limited (≈2% of the Euro HY index). This includes both producers and service providers, the latter offering equipment rental, logistics, and maintenance. While upstream profits are highly sensitive to price swings, service companies benefit from more stable demand and longer-term contracts, helping absorb volatility. By contrast, the U.S. HY market has greater exposure (≈11% of the index), reflecting the U.S.’s role as the world’s largest oil producer and potentially looser ESG constraints.

In theory, lower oil prices should help energy-intensive industries. European chemical producers, for example, might enjoy relief after years of pressure from high energy costs, as discussed in a recent blog: Is There Value in the Troubled European Chemical Sector? However, because weak oil prices also reflect weak industrial activity, the net benefit is likely limited—cost savings are offset by weaker revenues.

Given today’s uncertainty and the likelihood of new geopolitical or policy shocks—such as tariffs or supply disruptions—we prefer to avoid pure-play oil producers, whose futures depend heavily on commodity prices beyond their control. The E&P sector behaves more like equity than fixed income: shareholders enjoy the full upside when oil rises, while bondholders face significant downside since many issuers cannot operate profitably below certain price levels. Instead, from a fixed-income perspective, we see more value further down the value chain, in areas like midstream pipelines and select oilfield service companies with business models more insulated from short-term commodity price swings.

We do not forecast oil prices, but it is easy to envision default rates rising in this sector if prices stay low for too long. The last such episode occurred in the U.S. between 2014 and 2016. It was a challenging period for HY bond investors, but widespread contagion also created opportunities to buy names unrelated to oil that had been unfairly punished. Time will tell whether a similar episode unfolds next year.