Frankenstein: US banks and the unintended consequences of the Fed’s monetary experiment

12 APR, 2023

By Michael Cembalest

Creating life in inanimate body parts from deceased criminals using energy from a lightning storm sounds great on paper and was inspired by 18th-century Galvanism experiments. However, Dr. Frankenstein’s invention ended up having negative unintended consequences that he didn’t anticipate. Same for the Fed; ten years of negative real policy rates followed by sub-1% 10-year Treasury yields and a doubling of the Fed’s balance sheet from $4.5 trillion to $9 trillion in just two years, the largest monetary experiment in US history, has negative unintended consequences as well. Like the townspeople fleeing Frankenstein’s Monster, some depositors are now wary of banks with substantial underwater loans and securities whose yields the Fed had manipulated.

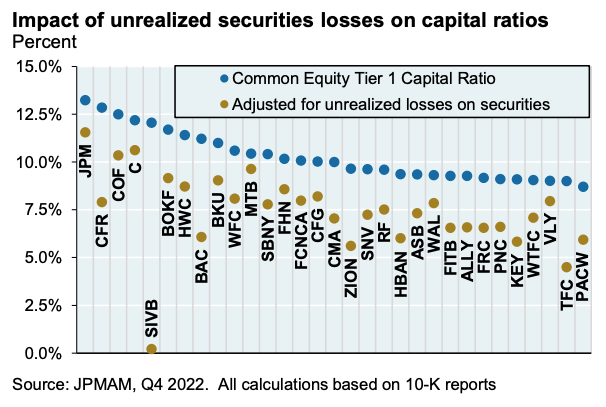

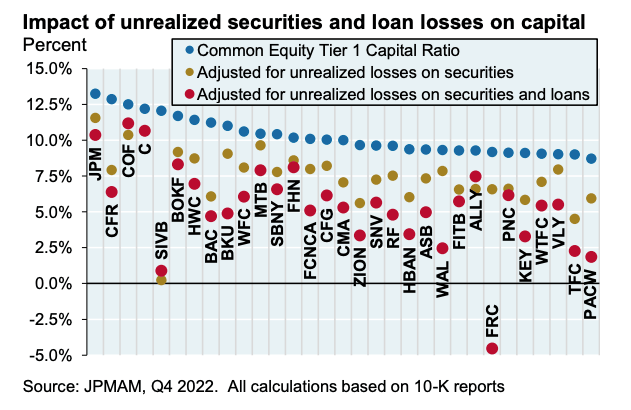

In our March 10 piece, I included a chart on the Pro-forma impact of unrealized securities losses on bank capital ratios (above). In the rush to write on the day of the Silicon Valley Bank (a.k.a. Silicon Venture Bank) failure, I neglected to mention another Fed casualty: residential mortgage and other loans underwritten at reasonable loan-to-value and debt to income/cash flow, but at very low coupon rates. Now that mortgage rates have doubled from 3% to 6%, there’s another issue to consider: unrealized loan losses due to higher rates. The second chart shows the impact of this additional adjustment on capital in red.

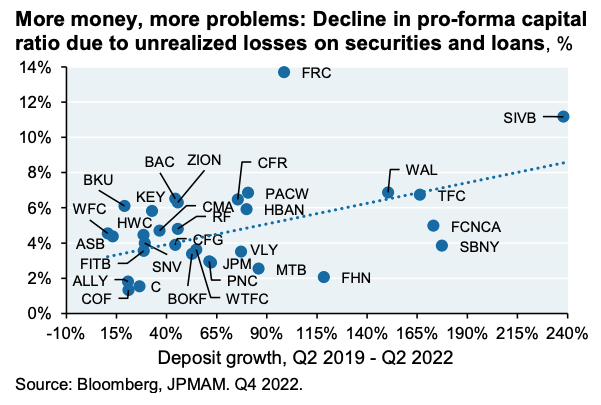

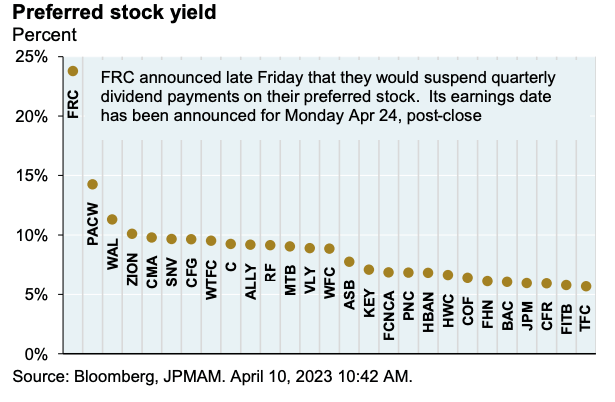

To be clear, some banks did a better job than others in navigating the Fed’s monetary experiment. But as shown in the third chart, being flooded with COVID-era deposits made navigating that monetary experiment much harder to do. Some banks with the largest pro-forma capital adjustments due to rising interest rates have seen their preferred stock yields rise sharply, as shown in the fourth chart.

The presence of unrealized losses on bank balance sheets is not abnormal and is entirely consistent with a rising interest rate cycle. The problem this time: some banks were flooded with so many stimulus-related deposits at a time of low rates that their balance sheets are stuffed with low-yielding assets. And to reiterate, this is only a problem when large deposit outflows cause unrealized losses to be realized.

The Fed’s new rules for the Discount Window allow banks to borrow against securities at book value rather than market value, so that should help. But it doesn’t address banks with underwater, high-quality loans or the flood of deposits departing for higher money market fund yields. Here’s what we know about the big picture. Many system indicators are now stabilizing, but one news story, one rating agency action, or an announcement from a single bank could reignite market/depositor concerns.