¿Qué le espera al oro?

9 DIC, 2024

Por L&G

Autor: Aude Martin, ETF Investment Specialist de Legal & General Investment Management

El futuro del oro ha sido ampliamente debatido tras un periodo de volatilidad, en el contexto de una trayectoria ascendente sostenida que ha llevado al oro a subir más del 35% este año1.

En este artículo, consideraremos los factores detrás de los últimos movimientos de precios, las influencias estructurales que podrían afectar el panorama a medio plazo, y finalmente cómo los inversores podrían acceder mejor a los cambios en el precio del oro.

¿Por qué cayó el oro tras las elecciones?

Inmediatamente después de la victoria electoral de Donald Trump en EE. UU., los precios del oro disminuyeron. Esto se debió a la retórica previa de Trump sobre recortes fiscales y aranceles.

Si estos planes se materializan (aún una incógnita importante), se podría esperar un aumento en los tipos de interés en EE. UU. y un fortalecimiento del dólar. Como un activo sin rendimiento, cuyo precio está en dólares, esto podría pesar sobre el oro. Sin embargo, hay advertencias importantes a considerar.

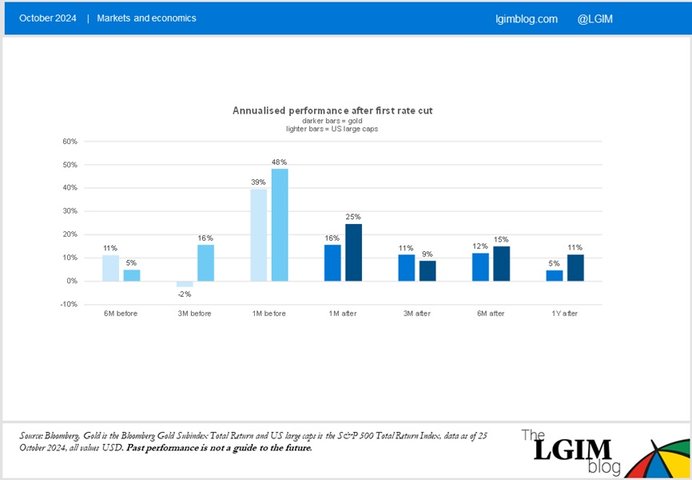

Lo que nos dice la historia sobre el oro en esta fase del ciclo económico

Es crucial poner estos movimientos a corto plazo en un contexto más amplio. Recordemos que aún estamos en un entorno de recorte de tipos, con la Reserva Federal de EE. UU. apenas comenzando este ciclo en septiembre, y el impacto potencial de las políticas de la administración Trump sigue siendo desconocido.

Históricamente, el oro ha generado rendimientos anuales fuertemente positivos antes del primer recorte de tipos en EE. UU., lo que coincide con el aumento del precio del oro observado en el último año.

Más importante aún, el oro también ha continuado registrando rendimientos positivos seis y doce meses después del primer recorte, lo que sugiere más margen para alzas.

Una visión a largo plazo

Factores estructurales también podrían influir en el camino de los precios del oro en 2025 y más allá.

Analistas de Goldman Sachs (GS) señalan que la relación histórica entre tipos de interés y precios del oro se ha alterado en los últimos años2. Mientras que los tipos bajos siguen favoreciendo al oro, la relación se "reinició" desde 2022 debido al aumento de las compras de bancos centrales de mercados emergentes, impulsadas por preocupaciones sobre posibles sanciones financieras tras la invasión rusa a Ucrania3.

Como resultado, GS pronostica que el precio del oro alcanzará los $3,000 para fines de 2025.

Analistas de Panmure Liberum coinciden en que el riesgo geopolítico elevado sigue siendo un factor fundamental para los precios del oro, ya que los inversores buscan activos refugio4.

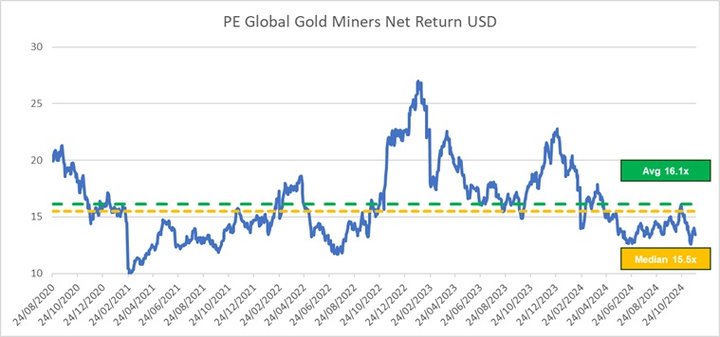

¿Oro o acciones de mineras?

Para inversores potenciales, hay dos opciones principales:

- Comprar el metal (o, más probablemente, obtener exposición a través de un fondo de oro físico). Esta opción puede ser adecuada como forma de seguro en un portafolio multiactivo.

- Acciones de minería de oro, cuyo precio está estrechamente ligado al oro. Estas acciones tienden a tener una beta más alta en comparación con el oro físico y pueden ser una opción atractiva para expresar una opinión sobre la dirección del precio del oro.

Valoraciones de las mineras

Otro factor es comparar las valoraciones actuales de las mineras con las medias históricas. Si las previsiones de GS sobre el aumento del precio del oro se confirman y persiste la beta histórica, las valoraciones bajas podrían ofrecer un impulso adicional para los inversores.

Para saber más, visite nuestra web.

1 Fuente: Bloomberg a 27 de noviembre de 2024

2 Fuente: Gold predicted to climb higher than expected as records shatter | Goldman Sachs

3 Fuente: https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q1-2024

4 Fuente: Gold suffers worst week in 3 years as investors weigh Trump victory

Key Risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Important Information

The views expressed in this document are those of Legal & General Investment Management Limited and/or its affiliates (‘Legal & General’, ‘we’ or ‘us’) as at the date of publication. This document is for information purposes only and we are not soliciting any action based on it. The information above discusses general economic, market or political issues and/or industry or sector trends. It does not constitute research or investment, legal or tax advice. It is not an offer or recommendation or advertisementto buy or sell securities or pursue a particular investment strategy. Past performance should not be taken as an indication or guarantee of future performance and no representation, express or implied, is made regarding future performance.

Certain of the information contained herein represents or is based on forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, undue reliance should not be placed on such forward-looking statements and information. There is no guarantee that Legal & General’s investment or risk management processes will be successful.

No party shall have any right of action against Legal & General in relation to the accuracy or completeness of the information contained in this document.The information is believed to be correct as at the date of publication, but no assurance can be given that this document is complete or accurate in the light of information that may become available after its publication. We are under no obligation to update or amend the information in this document. Where this document contains third party information, the accuracy and completeness of such information cannot be guaranteed and we accept no responsibility or liability in respect of such information.

This document may not be reproduced in whole or in part or distributed to third parties without our prior written permission. Not for distribution to any person resident in any jurisdiction where such distribution would be contrary to local law or regulation.

© 2024 Legal & General Investment Management Limited, authorised and regulated by the Financial Conduct Authority, No. 119272. Registered in England and Wales No. 02091894 with registered office at One Coleman Street, London, EC2R 5AA.

LGIM Global

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes:

European Economic Area: LGIM Managers (Europe) Limited, authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011 (as amended) and as an alternative investment fund manager (pursuant to the European Union (Alternative Investment Fund Managers) Regulations 2013 (as amended).