BofA Global Fund Manager Survey: Investors pile back into defensives

28 APR, 2023

By Constanza Ramos

The Bank of America (BofA) has published its latest survey: April Global Fund Manager Survey (FMS). This is the most bearish FMS of 2023 as the credit crunch causes a double-dip in global growth & highest bond allocation since March 2009.

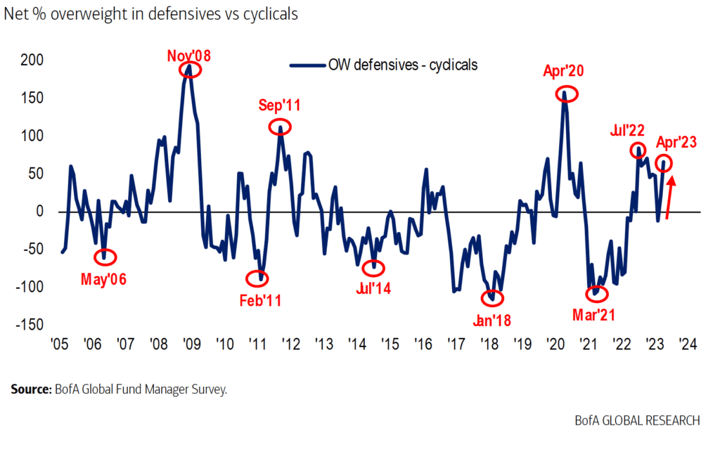

The survey also shows that investors moved back into a defensive (utilities, staples, healthcare) vs. cyclical (discretionary, banks, energy, materials) driven by big rotations out of banks & materials and into healthcare & utilities. This is the FMS most OW defensives vs. cyclical since October 2022.

Moreover, FMS sentiment dipped in April as investors brought down equity allocation (down 2ppt MoM to net 29% UW) and growth expectations worsened to December 2002 levels. April FMS showed a net 63% of investors expect a weaker economy, up 13pptMoM to the most pessimistic since December 2022.

Economic growth expectations continue to hover near historical lows while the S&P 500 has yet to catch up with the weak macro outlook. Net 84% say global CPI heading lower while net 58% predict lower short-term rates, the most since November 2008. Note that a gross 72% share of FMS investors sees short-term rates lower within the next 12 months.

35% of FMS investors expect the Fed to start an easing cycle in Q1'24, while 28% say in Q4'23, 14% say in Q3 23, and 10% say in Q2'24. These expectations are in line with bond markets, which currently price 12bps of cuts in Q3'23, 37bps in Q4'23, 36bps in Q1'24, and 47bps in Q2'24.

On the other hand, a large majority of FMS investors (80%)believe that the US debt ceiling will be raised by Sep'23.

Regarding real estate, FMS investors are the most bearish on this sector since July 2009. Investors have been net UW the asset class since September 2022. The report states that concerns over commercial real estate continue to weigh on the sector.

On the Macro side, net 63% expect weaker global growth (reversing 4 months of improvement) & net 84% say CPI heading lower = 72% predict lower short-term rates, most since Nov'08.

European Fund Manager Survey

Growth pessimism increases due to monetary tightening

A net 75% of participants think European growth will weaken over the coming twelve months, up from a low of 33% in February, in response to monetary tightening, while the proportion expecting a European recession remained broadly stable, at a net 55-60%. A net 59% expect a stronger Chinese economy over the coming twelve months, the lowest level since December. Globally, a net 63% project growth to slow over the coming twelve months, up from a low of 35% in February, with expectations for a global downturn up from a net 24% to 48%.

Investors expect disinflation as demand destruction bites

A majority of 58% expect demand destruction in response to deteriorating credit conditions to be the dominant macro theme over the coming months, leading to:

A majority of investors are now bearish on European equities

70% of investors expect downside for the European market over the coming months in response to monetary tightening (up from 66% last month) and 55% project downside over the next twelve months (up from 42%). Sticky inflation leading to more central bank tightening is seen as the most likely cause of a correction (30% of respondents), followed by weakening macro data (25%). A plurality of 38% consider not having enough defensive hedges as the key risk for their portfolio, though 25% worry about reducing their equity exposure too much and missing out on a continued rally.

Doubts on cyclical grow and capitulation on banks continue

57% of respondents see a downside for European cyclical relative to defensives in response to slowing growth, up sharply from 34%. A net 78% expect high-quality stocks to outperform low-quality stocks (up from 66% last month), while a net 15% think value will underperform growth (last month 11% expected value to outperform). Tech remains the most popular sector overweight in Europe, having regained the top spot last month for the first time in a year, while real estate remains the most disliked sector. Capitulation on banks continues, with the sector slipping to an underweight position, having been the largest consensus overweight as recently as February.