A new era for emerging market bonds

2 DEC, 2025

By Patrick Zweifel, Chief Economist at Pictet Asset Management

On global financial markets, emerging markets have arguably been the biggest surprise of 2025: their local-currency bonds have risen by about 16%, and their dollar-denominated debt by 12%, far surpassing the modest 3% gains of the global fixed-income universe.¹ This outperformance is particularly significant because it comes after a “lost decade”, marked by disappointments that led many investors to doubt whether emerging markets could still be considered a conventional asset class.

The strong performance of EM debt reflects several fundamental trends. In our view, the asset class’s returns rest on five key factors: the trajectory of interest rates, the strength of the US dollar, global trade conditions, commodity prices, and China’s economic growth. Of these, four are now positive, creating the most favorable environment in twenty years for EM bonds.

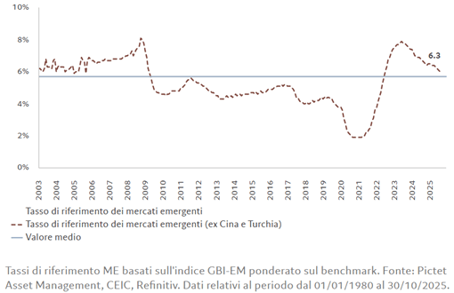

Monetary easing

Emerging-market central bank policy is restrictive but in the process of normalizing—a combination that generally supports EM bonds. Although the average weighted policy rate has fallen to 6.3% (its lowest level since 2003–2008), it remains well above the estimated neutral rate of around 5.5% (Fig. 1). Economic growth close to potential (about 4%) and inflation returning to 3% lead us to expect a gradual normalization of monetary policy, which bodes well for fixed income. Moreover, real interest rates, adjusted for inflation, remain above 3%, a level historically linked to periods of strong performance for emerging markets.²

Fig. 1 – Rate Cuts Ahead

A weaker dollar

Since the start of the year, the US dollar has depreciated by 9% against a trade-weighted currency basket—a weakening we expect to continue amid both cyclical and structural pressures. US growth is slowing, the Federal Reserve is cutting rates, and risk premia are falling. The dollar is also being undermined by structural shifts.

The world is moving from a US-dominated system to a multipolar one, causing the dollar to lose some of its supremacy. Since 2014, the US dollar’s share of global FX reserves has fallen from 66% to 58%, as the use of US assets as a geopolitical tool has reduced their appeal and prompted especially developing countries to seek alternatives.

Economic sanctions and threats of exclusion from the SWIFT payment system have diminished the perceived safety of dollar reserves. Recent policies under President Trump have exacerbated this trend—with threats of taxes on foreign assets, widening fiscal deficits, and openly hostile rhetoric toward institutional independence (including the Fed).

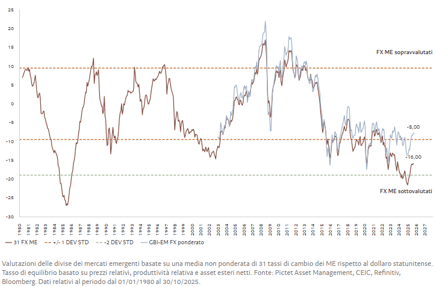

In this context of economic populism and institutional instability, the dollar may even be overvalued: according to our analysis, it trades at nearly two standard deviations above its fair value, while EM currencies remain undervalued by 8% to 11% (Fig. 2). Further dollar weakness therefore seems likely—a clear benefit for EM assets.

Fig. 2 – Poised for Appreciation

Global trade holds up despite tariffs

Tariffs and geopolitical tensions have cast a shadow over the outlook for international trade. Yet these concerns have so far proven unfounded: global exports have surpassed pre-COVID levels. This is partly because US imports account for just 13% of global trade—not enough to shift the overall trend.

According to our forecasts, raising average US tariffs to 18% will reduce the volume of US imports by only 2 percentage points.

This decline is even less meaningful compared with the growth in trade between emerging markets: nearly 46% of EM exports now go to other developing countries (vs. 23% in 2000). Equally encouraging is the growing number of free-trade agreements, led by the European Union, which recently signed one with Indonesia and is negotiating others with India, Mercosur, and several Southeast Asian countries.

Global trade is therefore reshaping itself rather than shrinking.

Commodities are recovering

Commodity prices are rebounding, up roughly 5% year-on-year, driven mainly by precious and industrial metals. The trend is supported by a weaker dollar, a recovery in global manufacturing, and the energy transition (copper, for example, remains in high demand for solar panels, electric vehicles, and more).

Large investments in energy- and metal-intensive infrastructure—particularly to support the boom in Artificial Intelligence—further reinforce this trend.

For commodity exporters, many of which are EM countries, the environment is doubly favorable: rising prices improve trade conditions, while economic diversification efforts in the Gulf (Saudi Arabia, UAE) are reducing dependence on oil and lowering macroeconomic volatility.

The unresolved factor: China

China is the only one of the five previously mentioned factors that remains neutral rather than positive for EM bonds—though there are signs of optimism here as well.

The Chinese economy is normalizing after a strong first half. Industrial investment is intentionally slowing due to “anti-involution” policies, aimed at reducing excess capacity and restoring corporate profitability. Although the immediate impact is slower growth, the medium-term advantages are clear: an economy less dependent on subsidies and potentially able to sustain higher wages—and therefore higher prices.

This shift, modest as it is, could relieve pressure on South Korean producers and other Asian economies exposed to Chinese competition, with positive spillovers for global markets.

Furthermore, China is expected to benefit from fiscal support for households, with some measures already announced and others hinted at in the latest Five-Year Plan.

Opportunities in emerging-market fixed income

Within EM fixed income, we are currently particularly optimistic about local-currency bonds and corporate credit. We appreciate the reform efforts in countries such as Argentina (where President Javier Milei’s party won a sweeping midterm victory, paving the way for more positive changes), Nigeria, and Côte d'Ivoire.

For local-currency bonds, we see strong potential in regions where real rates are high and central banks have room to significantly ease monetary policy, such as in parts of Asia, Latin America, and South Africa.

In EM corporate credit, we are especially interested in companies with solid fundamentals and exposure to domestic-growth opportunities. Examples include:

- communication-tower operators in Sub-Saharan Africa

- Mexican utilities and banks

- gas producers and gold miners in Uzbekistan

Emerging markets are finally emerging from a long period marked by difficulties. Their recent outperformance is not a technical rebound, but a reflection of deeper shifts in underlying dynamics. This could mark the beginning of a new world order, in which emerging markets cease to mirror the developed world and once again become its driving force.