A Tag-Team Effort: Battery & Hydrogen Fuel Cell EVs Both Needed to Reduce Emissions

26 MAY, 2022

By Madelina Ruid

EV adoption is accelerating as governments and corporations work towards meeting climate change-related emissions reduction targets. Globally, 6.5 million EVs were sold in 2021, accounting for just under 9% of annual total car sales. While the EV segment’s share remained small compared to ICE vehicles, 2021 marked a significant increase from the 3.3 million EVs sold in 2020 and the 2.3 million sold in 2019. The EV momentum continued into January 2022, particularly in major markets such as China and the United States.

Industry forecasts have EVs reaching a 36% penetration rate by 2030, representing a $1.4 trillion opportunity. Over 135 countries have economy-wide net-zero emissions targets, with many aiming for 2050 or earlier. Additionally, many countries have established support mechanisms and allocated funding to encourage EV adoption and the expansion of supporting EV charging infrastructure.

Original equipment manufacturers (OEMs) are also committed to electrifying their fleets and transforming the sector from majority ICE vehicles to EVs. General Motors, Kia Corporation, Jaguar Land Rover, Mercedes-Benz, Volvo, and Volkswagen are among the large list of OEMs that plan to spend billions on EVs to hit electrification sales targets.

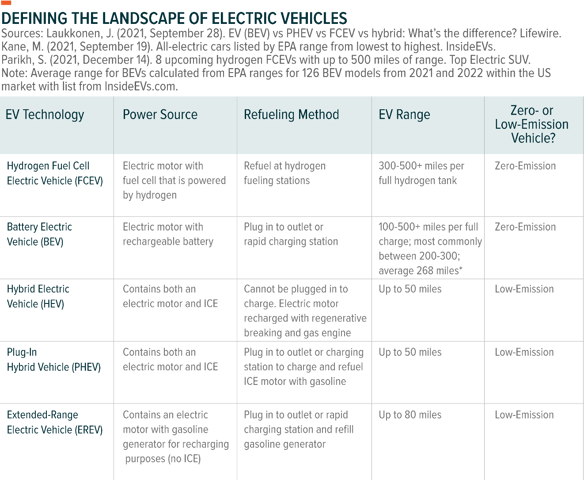

EVs classify as either zero-emission or low-emission in relation to their greenhouse gas emission outputs. Governments, companies, and consumers are focused on zero-emission vehicles. The two zero-emission vehicle technologies are battery electric vehicles and hydrogen fuel cell electric vehicles.

Battery Electric Vehicles (BEVs) are clearly the passenger car of choice among EVs, accounting for 71% of sales in 2021, while hybrid EVs made up roughly 28% and FCEVs less than 1%.8

BEVs come with the potential benefit of lower scheduled maintenance costs due to fewer parts than ICE vehicles, the potential for sizeable fuel savings, as well as an advanced charging infrastructure network. As BEV growth increases, we expect significant growth opportunities to emerge throughout the entire BEV supply chain, including in EV lithium-ion battery production and lithium mining. Europe is becoming the fastest-growing region for EV battery production outside of China. Conversely, the lithium market faces its largest-ever shortage in 2022, due to delays in new mining projects from the COVID-19 pandemic. Lithium mining needs to ramp up even more quickly over the coming years than currently planned to avoid a long-term deficit, higher EV costs, and weakened EV demand.

Hydrogen Fuel Cell Electric Vehicle (Hydrogen FCEVs) technology offers several benefits over BEVs that make it an attractive zero-carbon emission option for long-haul and heavy industrial vehicles specifically, including a higher energy storage density, shorter refuel time, and less loss of performance in cold weather conditions.

On the heavy industry side, the mining sector stands out as an early adopter of FCEVs, with companies like Anglo American, Fortescue Metals Group, and Antofagasta all working to implement FCEV technology.

Sparse hydrogen fuelling networks globally will remain the primary barrier to the widespread adoption of FCEVs in the near term. However, we expect more fuelling stations as hydrogen gains acceptance, particularly in the long-haul trucking industry.

We believe that BEVs and FCEVs are on track to increase their market share as part of the global effort to slow climate change, given the segment’s increasing share of total car sales and the growing momentum for EV adoption. For investors, the growing number of BEV passenger car models for sale and under development and the rapidly expanding BEV charging network can create investment opportunities throughout the BEV supply chain. Critically, lithium mining and battery manufacturing will need to ramp up to meet demand and for BEV growth to materialize. For long-haul trucking and heavy-duty vehicles, FCEVs offer benefits such as lighter vehicle weights and shorter refuel times. Demand for FCEV technologies, particularly in support of fuel infrastructure, appear set to materialize over the long term, creating additional opportunities for differentiated exposure in the EV space.

If you need more information, visit our page.