Artificial Intelligence: from promise to widespread adoption

22 JUN, 2026

By Daniel Ernst from Robeco

Markets are increasingly being driven by a powerful combination of strong earnings and rapidly accelerating technological innovation. Despite ongoing macroeconomic and geopolitical uncertainties, the current environment is characterized by the strength of the technology cycle, with artificial intelligence (AI) at its core.

In 2026, advances in artificial intelligence continued to accelerate. AI models have not only become smarter but also more useful. Following a pattern similar to previous computing eras – from mainframes to the cloud – as technology has progressed, AI adoption has expanded well beyond the technology sector. From defense to healthcare, AI is spreading across the entire economy.

The growing adoption of AI has led to accelerating revenues throughout the ecosystem. In the first quarter of 2026, leading AI model developers nearly tripled their revenues, helping drive cloud-computing revenues for the three largest hyperscalers up by 39.1% year-over-year, accelerating from the 33.2% growth recorded in the fourth quarter of 2025. Supporting this growth, capital investment in AI infrastructure continued to rise, which in turn contributed to a record 78% year-over-year increase in global semiconductor industry revenues during the quarter.

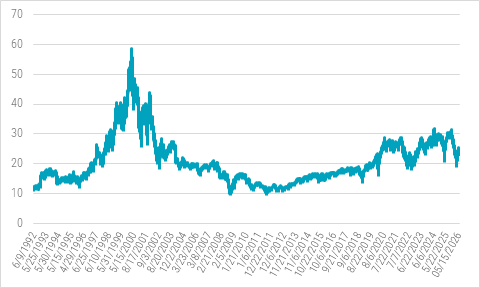

While concerns have resurfaced that enthusiasm for artificial intelligence may be fueling a market bubble, valuation multiples remain below previous peaks, and earnings forecasts continue to improve. The U.S. technology sector is currently trading at 23 times forward earnings (see Figure 1), in line with its ten-year average and below its five-year average of 26 times. For comparison, at its peak in 1972, the Nifty Fifty index traded at 42 times earnings, while in March 2000 the U.S. technology sector traded at 58.7 times earnings and the Nasdaq 100 at 75 times earnings.

Figure 1 – Forward Price-to-Earnings (P/E) Ratio of the S&P Technology Sector Index

Importantly, valuations are being supported by earnings growth. For example, in the first quarter of 2026, companies in the S&P index reported earnings growth of 28.6%, the strongest increase in the past five years, driven largely by the technology sector, where earnings grew by 54.8% year-over-year.

Although AI-related market gains have so far been concentrated in the semiconductor sector, signs of broader participation are beginning to emerge. After a prolonged period of significant underperformance, the S&P Expanded Software Index surged 18.8% in May, while the sector continues to trade at valuation multiples below pre-pandemic levels. Furthermore, despite concerns about potential AI-driven disruption, software-as-a-service (SaaS) companies recorded their strongest new revenue growth in more than five years during the first quarter of 2026.

Looking ahead, innovation remains the key driver of long-term growth, with artificial intelligence at the forefront. However, elevated expectations following a period of strong performance represent a potential short-term risk.

Against this backdrop, the focus remains on innovative, high-quality companies capable of translating technological leadership into sustained earnings growth, positioning themselves to capture the long-term opportunities presented by the age of artificial intelligence.