Artificial Intelligence investment and productivity

12 JUL, 2024

How does Artificial Intelligence affect investment strategies? What are the investment trends within the AI field? How does Artificial Intelligence influence business productivity and economic growth? Is passive investment profitable when it comes to the AI sector?

Matthew Bullock and Jeremiah Buckley, specialists at Janus Henderson, discuss how Artificial Intelligence is affecting investment strategies and how it is impacting business productivity.

Authors: Matthew Bullock, EMEA Head of Portfolio Construction and Strategy at Janus Henderson & Jeremiah Buckley, portfolio manager at Janus Henderson.

Investing in AI? It's no place for passive

By Matthew Bullock

The complexity of artificial intelligence demands an active investment approach to effectively identify opportunities and offer genuine market exposure to investors.

Index providers have begun offering up passive products at super low cost on the premise that investors can get exposure to all the upside potential of AI, but without the costs of active management.

This is very much “theme washing” and we remain concerned that investors are being sold a marketing story rather than the exposure to AI they expect due to primitive methodologies being applied to a highly complex market.

How passive strategies work

Before I explain why passive isn’t the place for AI, it’s important to take a step back and look at how an index exposure works.

An index is created by using a mathematical formula to allocate between securities in a particular market segment. These market segments can cover a broad range of areas including country, region, sector, theme, style.

There are two points to note here:

- The rules/formula around the index are determined before the index launches and do not change

- The criteria for determining the market segment (i.e. what’s in / out of scope) is also set prior to launch and does not change

While the companies that are included in the index will change over time –the criteria for selection will not.

This can work well in large, established markets where structural changes are gradual (e.g. gaining exposure to the S&P 500, MSCI ACWI). It doesn’t work in rapidly changing markets where the sector or industry can look significantly different over the next 12 months let alone the next 5-10 years. This is where AI index products fall flat.

Road-testing AI ETFs

To draw this conclusion, as a team we put ourselves into the seat of our investors and started trawling the market to see what was available. Being based in Europe, we came across three exchange traded funds (ETFs) that were offering AI index exposures.

This brings us to the first challenge:

Problem 1: There is no single definition of AI

What became particularly clear, was that index providers all had a completely different take on what should be included in an AI index, blending the AI story with a broader technology allocation. For example, AI was being blended with Big Data (which can mean many things), Robotics, Autonomous Tech, and in one instance, the Technology category as a whole.

This isn’t saying such blends are inappropriate investments, but they are not AI indexes.

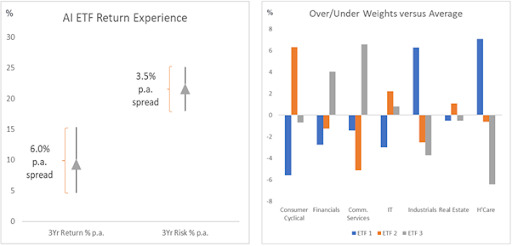

What was particularly extraordinary was how the returns differed between the three AI ETFs (exhibit 1) over a reasonably short period of time – in this case three years. The cumulative difference between the best and worst AI ETF performance over this time was 25%!

Exhibit 1: AI ETF passive investing return spread/asset allocation

Why was this? All were marketed as AI passive ETFs – even if the compositions were different.

Further, factor drivers (in this case value vs growth and large vs small cap) vary so differently between the ETFs. They are generally growth oriented, but some have more value, and the market capitalisation changes materially.

This is important because the perception of passive investing is that you’re getting exposure to a broad market. Yet we can see from the returns and factor drivers provided by each AI ETF give completely different outcomes.

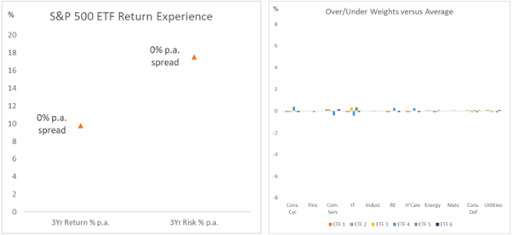

This compares with say an S&P 500 ETF where we know exactly the exposure provided irrespective of the ETF provider used. This is evident if you take the top five ETF providers by assets under management and compare the returns to the S&P 500 Index (exhibit 2).

Exhibit 2: S&P500 passive investing return spread/asset allocation

Problem 2: Questionable purity

Aside from the definition of AI, one of the key causes for this divergence in returns comes from a lack of purity from the companies selected in an index. AI in its truest form is quite a narrow market and there are very few companies that generate the vast majority of their revenue from AI.

As such, the AI indexes have a relatively low minimum threshold for what constitutes an AI company to ensure a sufficient population of securities exist.

Going back to our three AI ETFs and looking at their top 10 holdings, global conglomerates such as Bank of America, Amazon, Samsung and Apple all featured prominently. These are companies that utilise AI, but you would be hard pressed to make an argument why they are AI dominant businesses.

Problem 3: Forcing fixed rules on a dynamic market

The AI market is constantly changing, with it likely to play a major role in reshaping the global economy, leading analysts to expect the industry to grow to over US$ 1.8 trillion by the end of the decade, according to data provider Statista.

In a constantly evolving market, no set of rules can capture what the future of AI looks like and, therefore, while it is an exciting sector to invest in, we’re only at the very early stages of understanding what it can do.

What we know for certain, however; is that we cannot rely upon a simple set of rules and broad-based exposures for investing in such a dynamic vertical.

Productivity: The next propeller of a bull market?

By Jeremiah Buckley

At the conclusion of a strong first quarter earnings season for U.S. companies, we believe two factors will be increasingly important to the future path of earnings in a higher rate environment: productivity and innovation.

Recent gains in U.S. labor productivity are providing some optimism for market participants, especially in today’s higher inflation environment where productivity improvements serve as a welcome driver of economic growth without further stoking inflation.

The productivity rebound

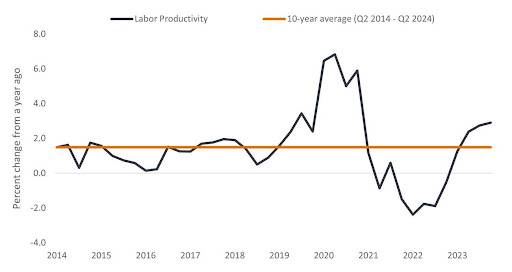

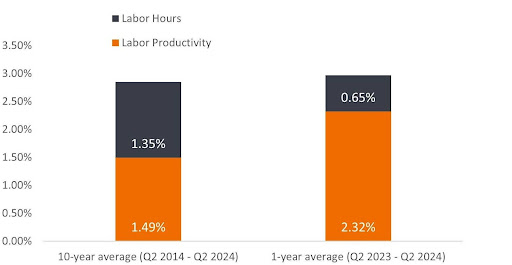

U.S. labor productivity, measured by nonfarm business output per hour, has rebounded after five consecutive quarters of year-over-year declines. For the past four quarters, productivity has averaged 2.3% growth, well above the 1.5% 10-year average (see Figure 1). This rebound accounts for 77% of real GDP growth since Q2 2023, while labor input explains only 23%, indicating companies are finding greater efficiency even with full employment (see Figure 2).

Figure 1: U.S. Labor Productivity (2014 – 2024)

U.S. labor productivity has rebounded to above average growth.

Figure 2: Contribution to Real GDP Growth

Labor productivity has been the primary driver of real GDP growth in the last year.

This productivity resurgence can be attributed to two key factors. First, pandemic-era inefficiencies and labor shortages have normalized, particularly in the retail, restaurants, and service industries. And those companies that initially overstaffed as economic activity resumed have since rightsized their workforces. Many companies, including a leading online retailer and cloud platform provider, are attributing a portion of productivity gains to resuming appropriate staffing levels.

Second, massive technology and digital spending during the pandemic are now bearing fruit across industries. Productivity tailwinds are particularly evident among tech and internet firms. These companies made significant investments in digital tools and software-as-a-service (SaaS) capabilities and then streamlined operations while reducing headcounts. Now, they are realizing the benefits through leaner sales, marketing, and research costs while maintaining or growing revenues.

Early AI productivity payoffs

Moreover, we’re witnessing early examples of AI impacting productivity, though it may be too soon to show up in data. There is widespread belief that we are on the cusp of a structural AI productivity boost akin to the dotcom era (1995 – 2004). AI’s true impact is still unfolding as the general-purpose technology continues to evolve and adoption spreads throughout the economy. Opinions vary on when it will materially impact productivity data, from as soon as one year to as late as the 2030s. In our view, the recent breakneck pace of spending on computing power and data centers by mega-cap companies suggests this timeline is closer than initially anticipated.

In terms of employment, generative AI (gen AI) has not yet had a significant impact. However, the percentages of firms anticipating AI-related employment increases (6.5%) and decreases (6.1%) for the next six months more than doubled from February 2024. Gen AI is still in relatively early adoption but steadily gaining traction, with a projected 6.6% of surveyed firms leveraging the technology by September 2024, up from 3.7% in September 2023.

By automating manual and repetitive tasks, gen AI can improve worker performance by as much as 40% according to a 2023 Boston Consulting Group study. Tangible use cases are already emerging, like software engineers using AI co-pilot assistants to significantly reduce build times and allow for more rapid iteration and code output.

Outside of the tech industry, a leading oilfield service company has implemented AI and machine learning tools to reduce oil and gas exploration and drilling cycle times to a fraction of the months previously required. In healthcare, AI algorithms are speeding up the discovery process and lowering the cost of bringing new drugs to market.

Indicators of productivity

Measuring company-level productivity gains can be challenging, as firms are cautious about revealing technology’s impact on human labor. However, examining indicators like operating leverage, revenue per employee, R&D spending, and technology investments can provide insights into efficiency and future productivity gains. Companies investing heavily in these areas, particularly those with scale and financial health, typically signal a commitment to innovation and productivity.

Positioning for productivity trends

Rising productivity allows businesses to generate more output without needing added labor or materials that could trigger higher inflation and restrictive central bank policies. This powerful economic driver could underpin a bull market by reducing inflationary pressures while enabling sustainable wage growth and consumer spending.

For investors aiming to capitalize on productivity trends, focusing on companies providing the enabling infrastructure will be key. Firms in semiconductors, software, and enterprise platforms working on AI and automation solutions should be direct beneficiaries as adoption grows.

In terms of companies adopting new innovative techniques, those with the scale and resources to invest heavily in research, testing, and implementation appear best positioned. Healthy corporate balance sheets are a prerequisite for the capital investment required to stay ahead of the productivity curve. Companies without sufficient size or investment capabilities risk falling behind and losing market share over time.

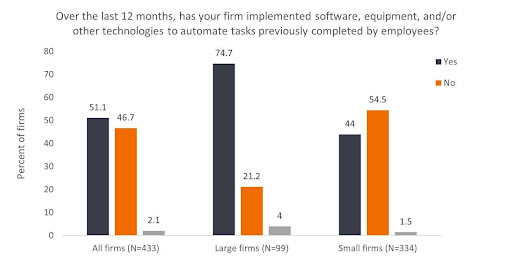

Figure 3: CFO survey suggests half of firms are implementing tech to automate employee tasks, including 75% of large firms

Ultimately, we think it is important to identify companies paving the way, those boosting productivity operationally now and developing solutions that will drive productivity gains for decades.