The attractiveness of small and medium-sized private equity funds

30 AUG, 2024

By Schroders

According to a report published by Schroders Capital, within the private equity segment, small and mid-sized funds have outperformed large funds and have proven to be more resilient through economic cycles.

Schroders Capital has analysed more than 64,000 private equity funds and 400,000 buyout, growth and venture capital deals since 2000.

Viswanathan Parameswar, Head of Asia Private Equity Investments; Eufemiano Fuentes Perez, Data Analyst; and Verity Howells, Private Equity Investment Research Manager; of Schroders Capital share the findings of the research.

As the private equity market has grown over the past decades, large funds have attracted an increasing share of global limited partner (LP) capital. Investors have gravitated towards large private equity funds on the assumption that they offer better performance and resilience due to their scale and stability.

Our analysis shows that, in fact, small and mid-sized private equity funds have outperformed their larger counterparts with stronger and more persistent returns over time. Moreover, given that the small and mid-size segment represents the vast majority of opportunities in private equity, we believe investors should not ignore this valuable portion of the market.

Small and mid-sized funds: favourable fundraising dynamics

We have analysed data from over 64,000 private equity funds and 400,000 buyout, growth and venture capital deals between 2000 and 2023 (for the purposes of performance analysis, we have excluded fund campaigns after 2017, where performance is not likely to be stable. Excludes single deal funds and funds of funds. Deals below $1 million are excluded). We classify the small and medium segments as funds of less than $500m and $2bn, respectively, and deals of less than $50m and $200m, respectively. The data presented below covers all regions and strategies, unless otherwise indicated.

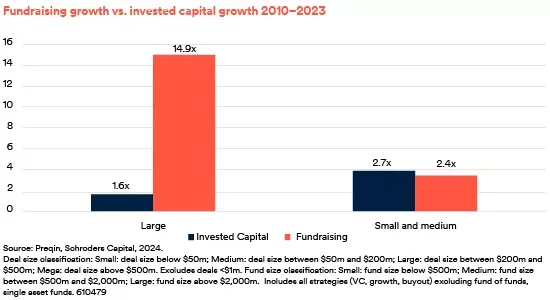

Over the past decade, fundraising by large funds has far outpaced deal flow, resulting in increased competition and hence entry multiples for large deals. Large deal flow has grown at 1.6 times, while fundraising by large funds has grown at 14.9 times. Small and medium-sized funds, by contrast, have experienced a 2.7 times growth in annual deal flow over the last decade, while annual fundraising has grown by only 2.4 times.

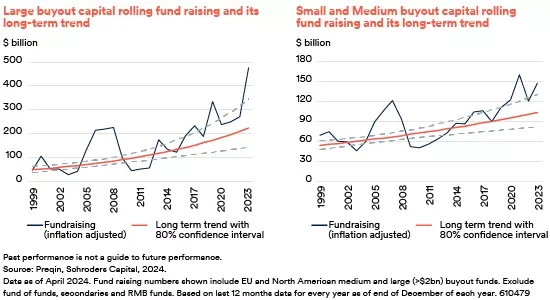

Not only is the pace of fundraising growth much higher in large funds, but fundraising levels are already well above the long-term trend, according to Schroders Capital's Fund Raising Indicator (FRI). The FRI is Schroders Capital's proprietary model that shows which areas of the private equity market are above or below long-term fundraising levels. The long-term trend is based on inflation-adjusted fundraising levels and excludes economic cycles. Too much capital leads to more competition for deals, higher prices and ultimately probably worse results.

We currently observe that fundraising in large European and North American buyout funds is 100% above the long-term trend, compared to only 40% in small and medium-sized buyout funds.

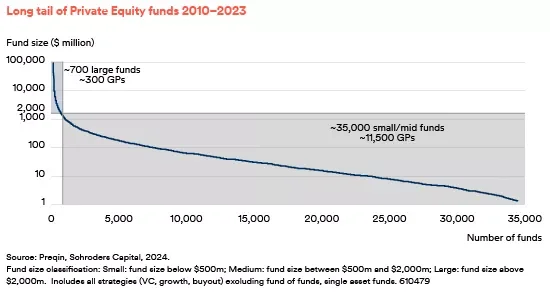

The long tail of private equity

Historically, the small and mid-market segment of the market has offered many more investment opportunities, both in terms of funds and deals.

According to Preqin data from 2010 to 2023, there have been 50 times more small and mid-sized funds in the market than large funds, and 17 times more small and mid-sized deal opportunities than large deals. In other words, the small and mid-sized segment makes up the majority of the private equity long tail, accounting for 98% of all funds in the market and 94% of all deals.

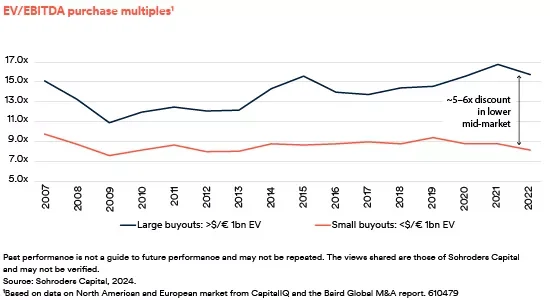

Entry multiples are more attractive for small and medium sized deals

Tracking long-term EV/EBITDA multiples shows a systematically wide discount between mid-size and large buyout deals (currently around 5-6 times).

This can be partly explained by the more favourable cash reserve situation in the mid-market. But it is also due to the higher perceived risk in small and medium-sized transactions, as smaller companies may be less diversified and professionalised. In addition, small and medium-sized operations tend to be conducted through proprietary networks rather than through competitive auctions.

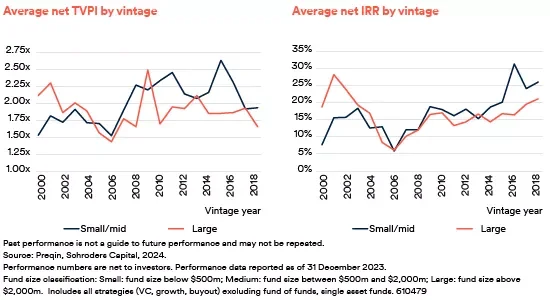

Small and mid-sized funds have outperformed large ones

On average, small and mid-sized private equity funds have outperformed large private equity funds in terms of total net value paid out (TVPI) in the years after 2005 and in terms of net internal rate of return (IRR) in the years after 2009.

Outperformance is also consistently demonstrated across different geographic regions and investment strategies. In Asia, North America and Europe, small and mid-sized funds achieved higher net returns than large funds between 2000 and 2018. Small and mid-sized venture capital, growth and buyout funds also outperformed their large counterparts.

Despite their attractive return profile, small and mid-sized funds have a different risk profile than large funds. To assess this, we compared the interquartile ranges (IQR) of small and mid-sized funds with those of large funds. Small and mid-sized funds showed a wider IQR, with higher returns in the top quartile and lower returns in the bottom quartile than large funds. A practical implication of this finding suggests that LPs should apply a rigorous process when conducting due diligence and fund selection for portfolios of small and mid-sized funds.

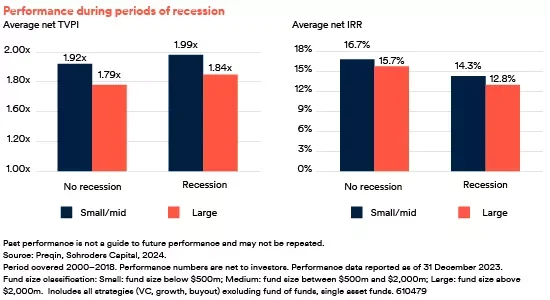

Performance of small and medium-sized funds: more resilient to economic cycles and more persistent over the years

We evaluated returns by fund size during two recessionary periods: the Great Financial Crisis (2007-2009) and the dotcom bubble (2001). We found that small and medium-sized funds offered higher returns than large funds, both in terms of net TVPI and net IRR.

The research showed that return persistence is highest among small funds, strong and significant among mid-sized funds, but weak among large funds. Specifically, 36% of small and mid-sized private equity funds that ranked in the top quartile in one vintage, ranked in the top quartile in the next GP vintage. This represents only 22% among large funds.

A broader and more attractive opportunity set

Traditionally, investors have favoured large private equity funds. However, small and mid-sized funds have outperformed their large counterparts across different regions, investment strategies and economic periods. This can be partly attributed to the fact that companies targeted by small and mid-sized funds tend to trade at lower valuation multiples. They also offer greater potential for operational value creation and are attractive to large private equity funds or strategic buyers looking to absorb typically smaller companies into their own platform (known as ‘tuck-in investments’). Especially at a time when large private equity funds are awash with capital, we believe the small and mid-cap segment offers a broader and more attractive set of investment opportunities.