Beijing’s relaxation came in slower than expected

27 JUN, 2024

Beijing becomes the latest major city to introduce property relaxation measures. The Beijing government announced (on 26 June) a set of supportive measures for the local property market, becoming the latest major city in China to introduce policy relaxation against the backdrop of continued weakness in the property sector.

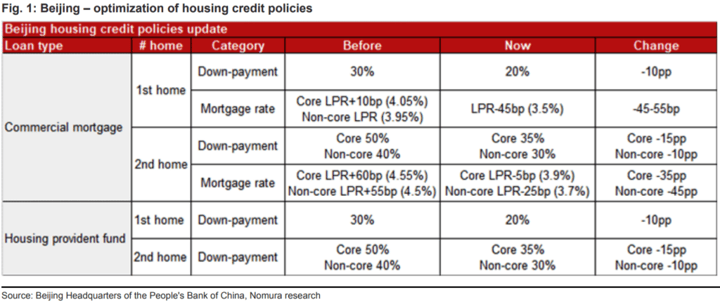

On the one hand, Beijing’s policy moves have been similar to the relaxations announced by another tier 1 city – Shanghai – from the perspectives of down-payment ratio (reduced to 20% from 30% previously, for first-time home purchases) and mortgage rates (cut to 3.50% from 3.95-4.05% previously, for first-time home purchases). On the other hand, Beijing did not make major adjustments to the local home-purchase restrictions (HPRs) – unlike Shanghai – indicating Beijing government’s more conservative stance on relaxing policy for the local property market, in our view. Details of Beijing’s policy relaxation are summarised in Fig. 1 .

More importantly, we believe that Beijing’s most-recent property easing measures came in slower than capital market expectations, given that they were announced roughly a month after Shanghai introduced its property relaxation package on 28 May. Notably, Beijing’s move also came more than a month after the central government’s 517 property easing .

Considering the absence of major easing of HPRs by Beijing, we see the new policies having limited impact on local property sales sentiment.

Physical property market continues to deteriorate

Overall, we have not observed any material recovery of the physical property market over the past month, since the central government rolled out 517 property easing; based on data from the National Bureau of Statistics, the property sector still experienced a 20-25% y-y decline in sales volume and a 25-30% y-y decline in sales value in May 2024.

We believe the effect of the central government’s and local governments’ follow-up policy support has not been reflected in the physical market yet. Even if the policy easing is effective, it would take a considerable period of time before any improvement is reflecte in the actual property sales and activities data, due to the sharp sector downturn that is i place for the past three years, in our view.

Developers’ share prices likely to remain volatile

We maintain our view that there are two key data points to monitor over the next few months, namely: (1) whether property sales in tier-1 and top-notch tier-2 cities can regain some meaningful momentum, and (2) whether the central government will introduce more measures to address other important issues of the property sector, such as sold but unfinished projects and old-home trade-in programs.

In the meantime, we could see further share price volatility of property developers and property value-chain companies in the next few weeks. We therefore reiterate our preference for quality names, such as CRL (1109 HK, Buy), Longfor (960 HK, Buy) and Beike (BEKE US, Buy).