Between Tech Giants and the Longest U.S. Government Shutdown: Market Nervousness

7 NOV, 2025

By François Rimeu from La Française

François Rimeu, Senior Strategist at Crédit Mutuel Asset Management

Tensions between the United States and China have flared up again after China halted the export of rare earths, prompting threats of steep tariff hikes from the U.S. Once again, fear outweighed the damage, as negotiations seem to have avoided the worst — at least for a year. Markets have grown accustomed to trade disputes between the world’s two largest economies and assume that, in theory, the worst-case scenario will always be averted, as shown by the market’s mild reaction to this episode.

On the domestic political front, Democrats and Republicans remain at an impasse, and the government shutdown continues. Historically, the macroeconomic consequences of a shutdown are minor, but it’s not impossible that this could add to current market jitters if it persists. Indeed, this time the previous record of 35 days under Trump’s presidency has already been broken, and the situation seems stalled for now.

Periods of U.S. Government Shutdown

1976 – Gerald Ford – 10 days

1977 – Jimmy Carter – 12 days

1978 – Jimmy Carter – 17 days

1979 – Jimmy Carter – 11 days

1981 – Ronald Reagan – 2 days

1982 – Ronald Reagan – 1 day

1983 – Ronald Reagan – 3 days

1984 – Ronald Reagan – 2 days

1986 – Ronald Reagan – 1 day

1990 – George H. W. Bush – 3 days

1995 – Bill Clinton – 5 days

1996 – Bill Clinton – 21 days

2013 – Barack Obama – 16 days

2018 – Donald Trump – 3 days

2019 – Donald Trump – 35 days

2025 – Donald Trump – 36 days

Why Are Markets Nervous?

Despite a generally positive earnings season for companies both in the United States and the euro area, markets are now punishing bad news sharply. Since the start of the season, share prices of companies that disappointed on both revenue and profits have fallen by an average of 6% at the time of publication (in the U.S.). According to UBS, this is the worst “penalty” suffered by underperforming companies since 2005.

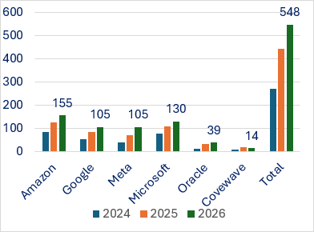

The causes of this nervousness are multiple. Geopolitical uncertainty plays a role, but the concentration of returns in technology and artificial intelligence — and doubts about AI investment profitability — seem more decisive. Meta’s results, weighed down by massive AI spending, illustrate investors’ current fears. The large bond issues from Meta (over $30 billion) and Alphabet (over $20 billion) may also signal overexuberance.

Still, it’s too early to panic. Hyperscaler investments should continue at least through the end of 2025. Nvidia reports a full order book for six quarters ahead, and results remain strong.

Investment by Hyperscalers (in billions of dollars)