Big tech’s AI spending test: when growth turns into a capital allocation challenge

5 MAY, 2026

For the past two years, the AI debate has been framed mainly as a growth story — who has the best model, the strongest cloud, or the fastest integration into search, software, advertising and enterprise workflows. Those questions still matter, but the latest Big Tech earnings show a clear shift: AI is no longer just a revenue opportunity. It has become one of the largest capital allocation tests in modern corporate history.

The key investor question is moving from “Who is spending the most on AI?” to “Who can turn that spending into durable margins, free cash flow and return on invested capital?” This shift matters because AI is transitioning from narrative to financial reality. The scale of infrastructure investment now directly influences valuation, resilience and long-term competitiveness.

Cash flow vs. capex: the new AI discipline test

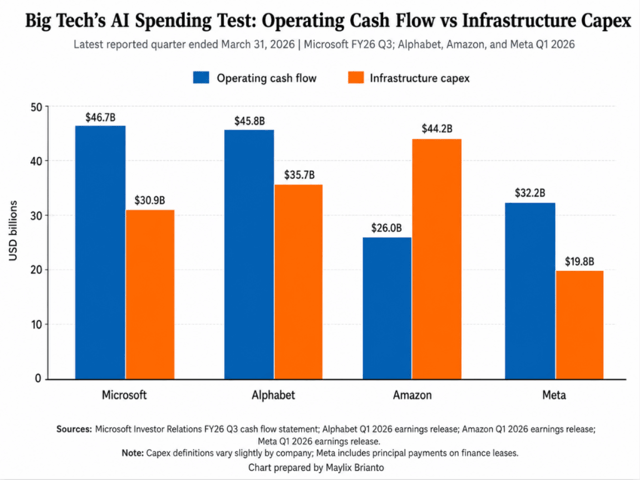

The latest quarterly results from Microsoft, Alphabet, Amazon and Meta highlight how massive the infrastructure buildout has become.

In the quarter ended 31 March 2026:

- Microsoft generated ~$46.7B in operating cash flow and spent ~$30.9B on property and equipment.

- Alphabet generated ~$45.8B and spent ~$35.7B.

- Amazon generated ~$26.0B and spent ~$44.2B.

- Meta generated ~$32.2B and spent ~$19.8B.

Infrastructure capex as a share of operating cash flow reached:

- 66% for Microsoft

- 78% for Alphabet

- 170% for Amazon

- 61% for Meta

This is not a temporary spike. It is a structural shift in how the largest technology companies deploy capital, driven by AI models, data centres, networking, energy requirements and semiconductor intensity.

Microsoft: cloud strength meets infrastructure intensity

Microsoft remains one of the clearest beneficiaries of enterprise AI adoption. Azure and the broader cloud ecosystem delivered strong growth, with Microsoft Cloud revenue reaching $54.5B (+29%). But with infrastructure capex at 66% of operating cash flow, the question becomes: Can AI-driven demand continue to support recurring revenue, margin resilience and high ROIC?

Alphabet: scale, acceleration and the cost of AI

Alphabet’s AI positioning is equally strong, with Google Cloud growing 63% to $20B. Yet the company also spent 78% of operating cash flow on infrastructure. The market is now watching whether Alphabet can convert AI infrastructure into sustained cloud profitability, advertising resilience and free cash flow strength.

Amazon: ambition, scale and cash flow pressure

Amazon is the outlier: infrastructure capex reached 170% of operating cash flow. This does not imply misallocation — Amazon has historically invested ahead of monetization. But it raises a key question: How much future AI monetization is already priced in? The investment case now hinges on timing, execution and payback, not just scale.

Meta: strong margins, different monetization path

Meta shows the lowest ratio at 61%, yet remains deeply engaged in AI investment. With a 41% operating margin, Meta’s AI monetization is less about cloud revenue and more about advertising efficiency, recommendation systems, engagement and AI assistants. The returns may be substantial — but less linear than cloud-driven models.

The investment implication

AI is entering a new phase:

- Phase 1: Narrative

- Phase 2: Adoption

- Phase 3: Capital discipline

Big Tech is no longer purely “asset-light.” These companies are becoming infrastructure-heavy platforms running one of the largest capex cycles in modern markets. That does not make them less attractive — but it requires a sharper analytical lens.

Key variables now include:

- Cloud growth

- Margin resilience

- Free cash flow conversion

- Capex discipline

- Return on invested capital

- Visibility of AI monetization

Final thought

The winners of the AI race may not be the companies spending the most. They will be the companies that turn infrastructure investment into durable economic returns. Big Tech earnings are no longer just quarterly updates — they are signals about the capital architecture of the AI era.