‘Black Monday’ 2024, what comes next?

8 AUG, 2024

By Jose Luis Palmer from RankiaPro Europe

On Monday, 5 August, we experienced a day in which global stock markets underwent a significant correction due to factors such as the US employment data, the Bank of Japan's interest rate hike, and geopolitical tensions, among other reasons. This day, already being referred to as a new "Black Monday," was marked by great volatility in global markets, with the hottest parts of the equity markets being the most affected. International fund managers have reacted to this and shared their views on what may come next.

While the current volatility may be painful, a readjustment following a period of excessive optimism could pave the way for a healthier market for the remainder of 2024, potentially creating a favourable environment for stock pickers and reinforcing the importance of active management. High levels of market volatility can create opportunities to identify and invest in the winning companies of the future.

Navigating market volatility

Adam Hetts, global head of Multi-Asset, and Oliver Blackbourn, portfolio manager at Janus Henderson Investors

With investors reacting to the worst global stock market sell-off since the early days of the COVID pandemic in 2020, Portfolio Manager Oliver Blackbourn and Global Head of Multi-Asset Adam Hetts consider the all-important question – what next?

What happened?

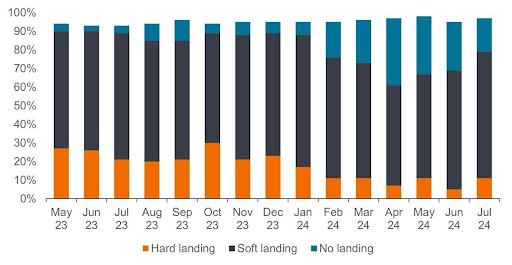

After a highly volatile moment in global markets, it is important to take stock of what has been happening. It now seems very clear that markets got ahead of themselves. Sentiment indicators, valuations and surveys all showed significant complacency about the outlook for the global economy. Many different types of investors had become very bullish on the back of good earnings results and the expectation for interest rate cuts, creating a fragility to the market rally.

Valuations had priced in the softest of economic landings, in line with expectations (see chart), and a weak labour market report was the catalyst for many to come to the realisation that there is still a reasonable chance of recession. That said, it still seems too early to make a decisive call, with a lack of glaring financial weaknesses creating resilience in the US economy and a stronger Institute for Supply Management services release showing that it is not all doom and gloom. The magnitude of market moves is perhaps as much about the lower liquidity we see at this time of year as the scale of any reset in sentiment or economic outlook.

Have expectations for a soft landing contributed to complacency?

Those surveyed were asked what they believed was the most likely outcome for the global economy over the next 12 months to 30 June 2024.

The equity rotation persists

It is notable that the worst volatility has been in the hottest parts of the global equity market, such as the so-called Magnificent 7, the NASDAQ 100 and certain Asia stock markets (eg, TOPIX). However, it is also important to note the areas that have held up better over the last couple of days and the last month, namely US value shares, US midcap stocks and the FTSE 100 Index in the UK. This suggests that there is an ongoing market rotation against the backdrop of a reset from over-enthusiasm. Lower interest rates, in the absence of a hard landing, have historically been good for risk assets overall, but some had already perhaps more than priced this in. A reset could create a more solid foundation for a push higher over the rest of the year, assuming the US labour market holds together.

A focus on Japan

The most significant volatility has been seen in Japan, where the export-sensitive stock market had previously benefited from continued weakening of the yen. The rapid strengthening of the currency in recent weeks likely pushed leveraged investors to unwind their positions. With interest rates having risen so much elsewhere and having barely moved in Japan, the yen has been an obvious candidate for funding foreign exchange carry trades.

However, the rapid currency unwind seems to have bled into equity market sentiment as a strengthening yen brought into question assumptions about Japanese export earnings. For those less committed holders, such a clear short-term headwind may have overpowered the longer-term argument of improving shareholder friendliness. The market may remain volatile in the short term as investors react to unprecedented market moves – Japan’s TOPIX rallied sharply on 6 August, a day after its second-worst single-day fall since 1950.

What’s next?

The silver lining is that, while the current volatility might be painful, a reset after a period of excessive optimism could lead to a healthier market. However, even if widely expected, a market reset of this speed and magnitude is unnerving for most any investor. It’s important to understand that a soft landing is being questioned but is not out of the question, meaning economic resilience and declining interest rates could ultimately help to lift risk assets again.

At the same time, these events are a critical warning that the market is relatively expensive and likely will remain extremely sensitive to any more negative economic news for the time being. Further, U.S. household stock ownership is at an all-time high, so stock market performance is likely to affect consumer confidence more than ever before.

While we continue to closely monitor the economic data, we see this as a favourable environment for active managers to benefit our asset allocations – the relative resilience of some areas of global markets shows that there are opportunities for those willing to look for them.

Expect global volatility and dispersion to continue

Marc Seidner, CIO Non-Traditional Strategies, and Pramol Dhawan, Portfolio Manager, at PIMCO

It’s been an unusually hot summer across much of the world, and an even hotter time for divergence and dispersion across financial markets.

For starters, developed market central banks are pivoting to rate cuts, but on widely varying schedules. The European Central Bank, Bank of Canada, Swiss National Bank, and Bank of England have all cut rates in recent months and will likely cut further in 2024. The U.S. Federal Reserve hasn’t cut yet but is expected to start soon, particularly given emerging signs of labor market weakness. Meanwhile, the Bank of Japan (BOJ) just raised interest rates in late July.

The increasingly asynchronous paths of economic growth, inflation, and central bank policy among nations would create elevated volatility and attractive investment opportunities across global bond markets.

Lately, the divergence theme has been playing out in real time, extending beyond sovereign debt to affect credit markets and stocks as well. Some examples:

- An encouraging inflation report after successive disappointing ones caused Australian 2-year bonds to rally on 31 July. That same day, the Bank of Japan raised interest rates by 25 basis points (bps), and Japan 2-year yields rose. The moves produced an immediate 30-bp differentiation between Australian and Japanese front-end rates.

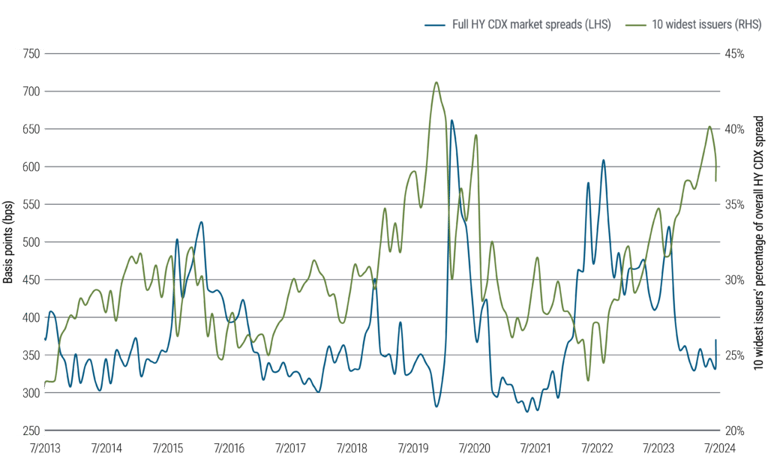

- Spread dispersion in the high yield CDX index is near all-time highs. As of 2 August, 37% of the overall credit spread of the widely followed market gauge came from the 10 constituent issuers trading at the widest spreads (see Figure 1), reflecting elevated default risk and depressed recovery prospects for the lowest-rated bonds. For much of the rest of the high yield market, spreads have been unusually tight.

Figure 1: High yield spread dispersion from 10 widest issuers

- The equity market has experienced outsize divergences between high-growth tech companies and small-cap stocks. Large tech stocks have tumbled lately due to lackluster earnings and concerns about returns on AI investment, while small caps have rallied. This rotation followed months of strong outperformance and crowded positioning in tech stocks. The Nasdaq 100 had outperformed the Russell 2000 by 21.7% in 2024 as of 10 July. Since then, the Russell has outperformed the Nasdaq by 13.6% as of 2 August, including a record 5.8% outperformance on 11 July.

- Stocks sold off and bonds surged in early August after a disappointing July jobs report rekindled U.S. recession fears that had seemed dormant for months. Not only dispersion but illiquidity is at play: For example, on 5 August, Japan’s Nikkei stock index fell a whopping 12.4%, putting it in negative territory for the year before recovering almost all those losses in the very next trading session.

We expect continued global volatility and dispersion as tight monetary policy and elevated sovereign debt levels threaten economic growth, particularly in a year of major elections in countries making up 60% of world GDP. Thankfully, this sort of volatility can create engaging trading opportunities for active investment managers.

The recent market swings have been a wake-up call for many investors who had enjoyed favorable returns in stocks and cash for much of this year.

More economic risks ahead

Central banks did well to tame the post-pandemic inflation spike with coordinated interest rate hikes. Inflation across many regions rose to painful levels for a brief period, but it continues to retreat thanks in large part to policymakers’ quick actions. Rates have also remained relatively contained and have been on a downward path of late, providing a tailwind for bonds.

Signs of weakening in other developed economies had for months contrasted with resilient U.S. growth, but lately even the U.S. appears vulnerable.

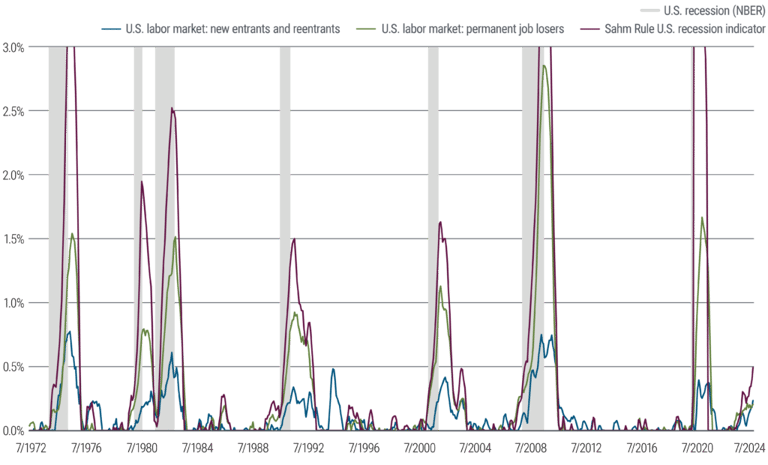

The July jobs data reached the cusp of triggering the Sahm Rule, a Fed gauge (based on employment data) that in the past has been a reliable indicator of U.S. recession. It’s worth noting that this rule has historically been triggered when actual levels of employment are declining, which hasn’t happened in a material way yet – recent weakness has more to do with labor supply as increasing numbers of job seekers enter the market (see Figure 2).

Figure 2: Decomposing the Sahm Rule: New job seekers vs. permanent job losers

Still, labor market strain could warrant an accelerated pace of rate cuts once the Fed starts easing policy. That would be consistent with prior cycles. Since the 1980s, when the Fed was hiking, only 25% of those hikes were by increments of more than 25 bps. By contrast, when the Fed cut, it did so by increments greater than 25 bps about half of the time. History also shows forecasters regularly tend to underestimate how aggressively central banks cut rates.

Amid this incipient policy divergence, we find bonds in countries such as the U.K., Canada, and Australia attractive due to downside economic growth risks, an improving inflation outlook, and how interest rates more directly affect the economy there through home mortgage structures. We also like trades that position for potential outcomes of this global dispersion, such as steeper yield curves in the U.S. versus flatter ones in Japan.

The recent market swings also serve as a reminder of the hedging properties of bonds, which tend to shine in these conditions. The diversification offered by an actively managed global bond allocation can serve as broad-based ballast, generating the potential for attractive income and capital appreciation, particularly in volatile times. Think of a bond fund allocation as an attractive option to help keep portfolios cool and comfortable on a hot summer day.

Macroeconomic data will drive global volatility until the Fed meeting in September

Charlotte Daughtrey, Equity Investment Specialist at Federated Hermes Limited

We have seen a mixture of both positive and negative data points from the US over the last quarter. The most recent employment data released at the start of August has concerned the market, however it is important for investors not to extrapolate one data point into a trend. Fundamentally, we still believe that the backdrop for the US remains reasonably robust with many valuations (ex Mag 7) unchallenging. It is also worth remembering that softening data is a pre-requisite for the Federal Reserve to cut rates; following more dovish rhetoric at the Fed’s last meeting, we expect several rate cuts between now and the end of the year. This should shore up our central thesis of a soft landing (or a very shallow, technical, recession).

Under this scenario, our outlook for small caps hasn’t changed: we see market leadership changing and a broadening out of performance funded by profit taking from the now crowded AI trade. Investors with volatility concerns should consider portfolios with a quality bias, which should help provide downside protection in an unsettled market.

Lewis Grant, Senior Portfolio Manager for Global Equities at Federated Hermes Limited

Volatility spiked this week as recession fears stalked global markets, and while the VIX has retreated from its highs, negative sentiment still dominates. The phrase “policy mistake” is back on the table as a US recession looms. Investors question whether the Fed’s focus on controlling for sticky inflation has brought us to the hard landing that we once thought had been expertly avoided. Friday’s jobs figures prompted many to suggest an emergency interest rate cut was needed to stave off recession, although this seems unlikely while the credit markets are sound.

Markets have whipsawed since, with Japan feeling the brunt of a sell off on Monday, driven by a fear the BOJ was making its own mistake, increasing rates at the wrong time and prompting a massive unwind in the Yen carry trade. These moves have felt knee-jerk – underlying fundamentals are largely unchanged – but reiterate the fragility of investor sentiment. We expect macro data – particularly that coming from the US – to drive global volatility into mid-September’s FOMC meeting. However, there is now a down-side skew hanging heavy over the markets: bad news will be punished very harshly, good news will receive a muted shrug.

From overheating to recession without transition?

Benjamin Melman, Global CIO at Edmond de Rothschild Asset Management

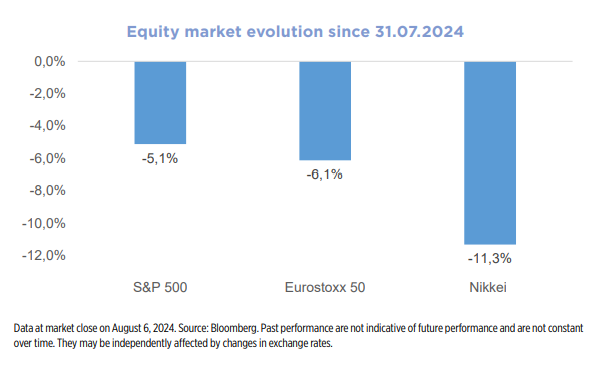

Equity markets have almost corrected in just three days. The fall does not seem to have been triggered by a single factor, but rather by a new environment: the (finally) hawkish turn initiated by the Bank of Japan (with a surprise rate hike) that sent the yen soaring; rising US unemployment; and heightened geopolitical risks in the Middle East. The trigger, however, was weak US labour data.

Are we heading to a recession?

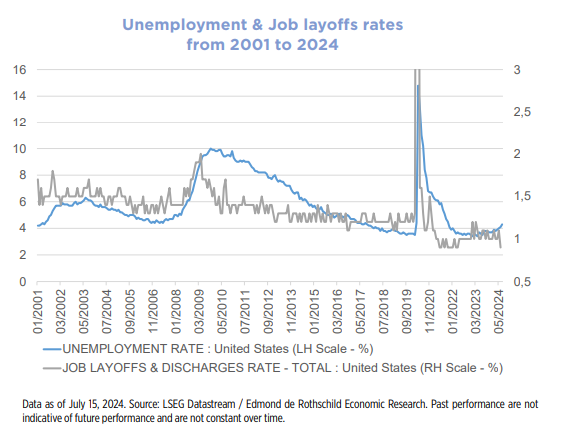

Investors are increasingly interested in the SAHM rule, which has noted without fail that the initial phase of a recession begins when the three-month moving average of the US unemployment rate is at least half a percentage point above the 12-month low, and according to the most recent labour data, this is currently the case. However, it is important to put these figures into perspective. We have not seen a pick-up in layoffs, but rather strong variations in the labour force, including a resurgence of new job seekers - mainly as a result of immigration - and, in the last month, a large number of workers unable to go to work due to adverse weather conditions (hurricane Beryl). Long-term unemployment has remained stable over the last year. While it is true that there has been a slowdown in new recruitment, the increase in unemployment is mainly due to a higher number of job vacancies. This phenomenon can only be positive for US companies, which have been suffering from labour shortages and are finally seeing wage costs start to fall.

Since the onset of the crisis, the US economy has become much more difficult to decipher. Sectors evolve according to different cycles, and we believe it is important not to react to isolated data. In this respect, it is interesting to look at nowcasts that aggregate quarterly data. Methodologies differ, but according to bloomberg, the New York Fed or the Atlanta Fed, the statistics are consistent with a quarterly growth rate of 1.17%, 2.11% and 2.54%, levels that are generally lower than the second quarter, but not plummeting. But more importantly, beyond the disagreements about the statistics, the factors that would cause the economy to go into recession - deteriorating company margins leading to restructuring and a financial crisis - are not evident. We are therefore in a slowdown phase called the "late cycle" which, historically, implies lower rates and decent returns for equities. Based on our reading of the cycle, we believe it is still too early to worry about economic risk, especially as the Fed governor believes that inflation has weakened enough for the central bank to want to strengthen the cycle.

The big change at the Bank of Japan

The Japanese stock market has been the hardest hit so far (down more than 11% since 31 July). The market's intrinsic fragility stems from the Bank of Japan's unexpected bullish turn in late July and the announcements of a potentially stronger rate hike cycle.

The central bank stands at an opposite pole to the rest of the world, which has already more or less safely rid itself of the inflation problem and has started - or is about to start - a cycle of rate cuts. This was enough to push the yen higher, weakening the exporting companies that feature strongly in Japanese stock indices. Especially since, in addition to the currency effect, the global economic slowdown will affect companies with higher operating leverage than their main rivals. Japan's zero interest rate policy has never had a happy ending, despite several attempts in recent decades. By choosing to lag its partners, the Bank of Japan is taking a serious risk.

The Japanese stock market fell first and more violently than others. However, we do not see this move as a leading indicator for the global stock market, but rather as a reflection of a very specific political risk.

Geopolitical risks persist

Recent developments have raised fears of an escalation of the conflict between Iran and Israel. However, both sides seem clearly keen to keep tensions under control. In recent days, falling oil, gold and dollar prices suggest that the geopolitical risk premium is not weighing significantly on markets at the moment.

Fed to the rescue

One element of caution is the pressure that has been mounting on the Fed to make an unscheduled rate cut before the next FOMC meeting, with investors arguing that the US central bank is late in the rate cutting cycle.

Disappointment is likely and we do not believe in this scenario. Cuts between meetings are extremely rare and only triggered by exceptional crises, such as LTCM or the market crash that followed the Kerviel scandal at the height of the subprime crisis. Although the current investor behaviour seems to be motivated by panic, no "problematic" factors have been identified so far to justify this behaviour. Moreover, lending conditions have deteriorated only slightly (thanks to the easing of long-term rates).

However, the potential for rate cuts should not be underestimated, as the central bank could largely meet market expectations before the end of the year. The Fed has already stated in recent weeks that inflation had subsided sufficiently and that it could now focus on addressing potential risks to growth.

The Fed's official estimates (points) indicate a long-term/neutral rate of 2.75%. Markets expect rates to fall to 3.2% by the end of 2025. Faced with a serious risk of recession, the Fed would set its policy rates below the neutral level: its potential for positive surprises clearly remains considerable.

The Fed will come to the rescue if the recession worsens. But in the short term, it would not make sense.