How do bonds perform in the year after the first rate cut?

9 SEPT, 2024

By Mark Munro

What does history teach us about the behaviour of bonds in the crucial 12 months following the first central bank rate cut? As we approach the first rate cut by the Fed, we look back at the historical performance of bonds in the 12 months following the first cut of the cycle.

Author: Mark Munro, Investment Director, Fixed Income, abrdn

On the interest rate front, the mantra of ‘higher for longer’ has once again taken hold. In the United States, stagnating inflation dashed the high hopes of central bank rate cuts earlier in the year.

The European Central Bank, for its part, has already begun to ease monetary policy. It is only a matter of time before other central banks follow suit and the rate-cutting cycle is extended.

What does the past teach us about the implications for fixed income assets? We have dug into the history books to see what happened to bond yields in that first year after the all-important ‘first dip’.

What does history tell us?

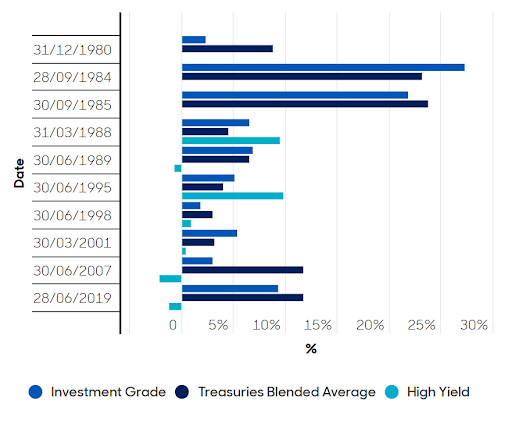

In the US there have been 10 ‘first’ rate cuts since 1980 (see Graph 1). The chart shows that the total return on investment grade (IG) corporate and government bonds after 12 months was positive each time.

Graph 1: Total bond returns one year after the first rate cut (%)

Investment grade bonds outperformed government bonds in five of the 10 cycles. However, when a major economic slowdown occurred immediately after the rate cut, as in 1980 and 2007, the higher rated government bonds performed much better.

On the other hand, lower rated high yield (HY) debt is more sensitive to the end of economic cycles and its performance was mixed, with three negative years and two flat years (out of seven).

If we are approaching the first rate cut in the US, history suggests increasing exposure to government bonds (and the longer duration to maturity that comes with it). This is especially true if a recession is looming.

Better corporate credit than government debt?

On the corporate bond side, credit spreads have also fallen sharply after 15 months of rises. Spreads indicate the additional yield over comparable government bonds that investors require to take on additional risk.

US Investment Grade (IG) and High Yield (HY) spreads have narrowed to their 20th percentile this century. This poses something of a conundrum for investors: total returns are attractive, but corporate spreads are now on the expensive side. That said, despite these spread levels, there are many reasons why credit could continue to outperform over the next 12 months.

As things stand now, economic forecasts point to the euro zone coming out of recession and achieving gross domestic product (GDP) growth of over 1%. Meanwhile, US growth is slowing moderately to between 2% and 3%.

If history is anything to go by, this range of 1%-3% GDP growth, with inflation broadly on target, is favourable territory for credit markets, and investment grade almost always outperforms government bonds.

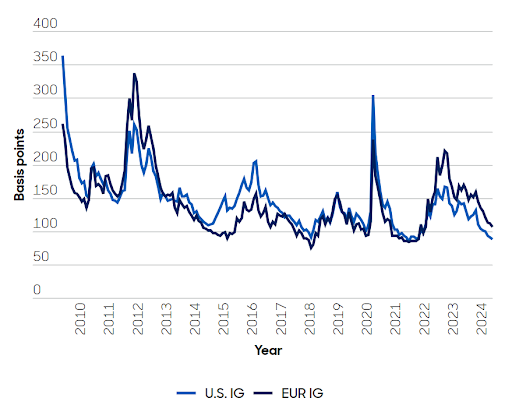

Spreads may not be cheap, but investment grade still offer an additional 1% yield over government bonds, pending rate cuts (see chart 2).

Chart 2: US investment grade credit spreads versus Europe* (bp)

Moreover, corporate spreads in Europe are not as tight, based on their own track record, as in the US. European spreads have room to tighten further (see chart 2).

Healthy companies

Meanwhile, company fundamentals are sound. Leverage - the level of debt relative to operating profits - is far from alarming, and profit margins have held up relatively well so far.

Although interest coverage ratios (operating profit, as an indicator of cash flow, divided by annual interest expense) have fallen, they are stabilising at still healthy levels.

Credit ratings are net positive - reflecting more upgrades than downgrades - and the overall composition of ratings of the major credit indices for both IG and HY bonds has improved over the last three years.

But not all is rosy….

At the beginning of the year, the focus was on slowing growth and a possible recession in the US. Then the focus shifted to inflation as a possible catalyst for further rate hikes. The latter risk remains a concern, but has diminished in importance.

Geopolitics is now the focus of much attention. Indeed, international politics has become for many investors a potential threat to market stability. Finally, it is also inevitable that idiosyncratic risk will increase as a result of rapidly rising interest rates. However, this will also provide opportunities for active managers.

…HY risk

If we experience the benign macroeconomic environment that we have outlined in the ‘good times for credit markets’ scenario, then it is quite possible that high yield bonds will outperform corporate bonds for the fourth year in a row.

That said, investors will have to weigh this possibility against another consideration: the additional yield available on high yield bonds has fallen to its lowest level this century versus corporate bonds.

For all these reasons, we believe it is wise to proceed with extreme caution, as valuation leaves little protection against any unpleasant surprises, be they economic or political.

Final conclusions

Although it has taken some time, we are getting closer to the first rate cut in the US. Given initial yields and the lessons of history, this is likely to translate into strong positive total returns for both investment grade corporate bonds and government bonds.

Credit spreads are getting more expensive. But demand for corporate bonds remains solid and the economic environment still seems conducive to higher outperformance.