Central and Eastern Europe outlook shaped by growing divergences and fiscal and governance challenges

2 JAN, 2026

Economic growth across Central and Eastern Europe (CEE) in 2026 will depend on the effective absorption of EU funds and the recovery of external demand, both of which will be critical for investment dynamics and productivity growth.

“Alongside growth, another key theme in our outlook is the institutional frictions that continue to weigh on policymaking. Reform momentum remains vulnerable to institutional frictions in Poland, political polarisation in Romania, and fragmentation in Slovakia”, said Jakob Suwalski, Executive Director of Scope Ratings’ Sovereign and Public Sector team.

“Meanwhile, persistent uncertainty surrounding the unfreezing of EU funds for Hungary continues to weigh on investment prospects and external resilience. Upcoming electoral processes and coalition shifts across the region may alter fiscal trajectories and delay structural reforms, reinforcing governance-related rating risks”.

CEE sovereigns enter 2026 facing elevated structural challenges, including fiscal pressures, demographic headwinds, and persistent external vulnerabilities. Growth and external resilience are supported by sizeable EU fund allocations, but the approaching deadline of the Recovery and Resilience Facility (RRF) creates absorption risks, particularly for countries with administrative bottlenecks such as Hungary, Bulgaria, and Romania.

“External headwinds also persist. Weak demand from Germany and other key EU markets will weigh on export-oriented economies such as the Czech Republic, Slovakia, and Hungary,” Suwalski added.

Trade policy issues and dependence on energy imports add further external pressure to higher-risk economies, including Romania (structural current account deficits), Hungary (energy import dependence, reliance on foreign capital, and unresolved EU funding issues), and Slovakia (a highly concentrated export base).

From an industrial perspective, high sectoral concentration—particularly in the automotive industries of Slovakia, the Czech Republic, and Hungary—increases vulnerability to tariff risks, uncertainty surrounding the transition to electric vehicles, and supply-chain disruptions. Tourism-dependent economies (notably Croatia and Türkiye) face cyclical and climate-related vulnerabilities, while persistent productivity gaps and the pressures of the green transition weigh on cost competitiveness.

“Regarding fiscal deficits and rising debt levels, the greatest challenges are evident in Poland, Slovakia, Romania, and Hungary, driven by widening structural gaps and significant expenditure pressures,” Suwalski noted. “Even countries with stronger fiscal fundamentals—the Baltic states, the Czech Republic, and Croatia—face rising defence demands, population ageing, and slower revenue growth. Failure to deliver on consolidation plans would increase downward pressure on ratings”.

Scope sovereign ratings for Central and Eastern Europe

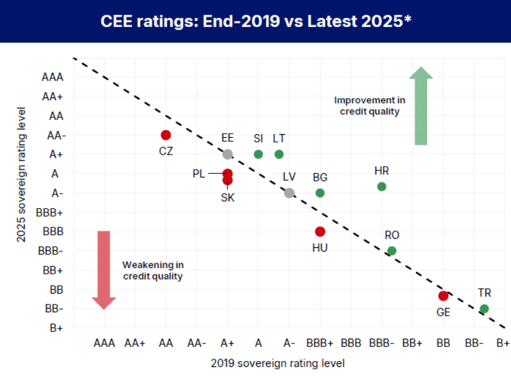

Scope upgraded the sovereign ratings of three CEE countries (Lithuania, Slovenia, and Bulgaria) in 2025 and revised one outlook to positive (Croatia, supported by sustained reform momentum and the benefits of euro area integration). The positive momentum from EU-funded investment, reform progress, and external rebalancing supports selective rating upgrades, while downside pressures stem from structural fiscal strain, governance challenges, and insufficient reform momentum.

Slovakia and Georgia currently carry negative outlooks, reflecting fiscal and governance-related pressures. Overall, the balance of sovereign outlooks across Central and Eastern Europe remains slightly negative, signalling continued divergence in rating trajectories across the region.