Is China exporting deflation to Emerging Markets?

Author: Mali Chivakul, Emerging Markets Economist at J. Safra Sarasin Sustainable AM

China's export prices have continued to fall this year, in line with our expectations. In addition, there are indications that Chinese government subsidies have led to lower export prices in the metal, furniture and automotive sectors. These subsidised products have increased their market share especially in emerging markets (EM), as they face more barriers in developed markets. On the other hand, we have found evidence that China directly contributes to deflation in two emerging markets: Brazil and Thailand. Cheaper imports from China have directly contributed to the disinflation process, while increased competition from Chinese imports could continue to put downward pressure on consumer prices.

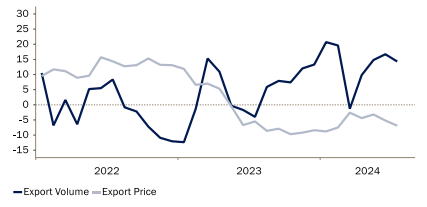

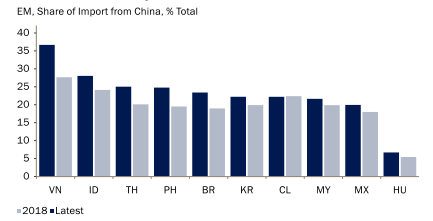

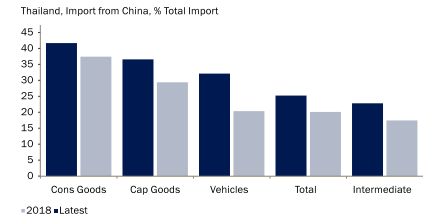

China's export prices have continued to fall this year, in line with our forecast last December (Chart 1). Weak domestic demand has prompted Chinese companies to expand abroad. Indeed, the share of imports from China has increased in major emerging markets since 2018 (Chart 2). In sectors related to the housing industry, large overcapacity due to the housing correction has pushed down prices. The steel sector is a good example. In the automobile industry, technological change (helped by government incentives) and fierce competition among producers have driven prices down.

It is widely believed that the fall in Chinese export prices has been a direct consequence of state subsidies. However, a recent IMF study shows that there is only weak evidence that China's state subsidies have reduced export prices on average. But at the sectoral level, there is evidence that subsidies have led to lower export prices and higher export quantities in metals, furniture and the automobile industry. In other sectors, such as electrical machinery, subsidies seem to have encouraged quality improvements and not to have reduced export prices.

Chart 1: China's export prices have been falling since May 2023.

Chart 2: The share of imports from China has increased in most emerging markets.

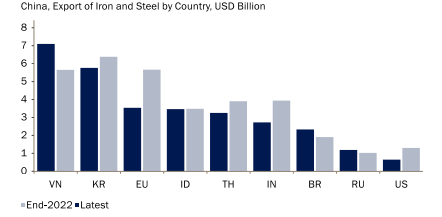

The same IMF study also finds that these subsidised products have gained more market share in emerging markets than in developed markets. One possible explanation is that China's subsidised products may face greater scrutiny and barriers in developed markets through retaliatory policies and countervailing duties. The steel sector, again, is a good example (Chart 3). Chinese steel has been subject to tariffs in the US since 2018 and anti-dumping duties in the EU. Emerging market governments have been much slower to react to increased steel imports from China. In Vietnam, an anti-dumping investigation began in June, but has not yet led to policy action. The Korean government has been mulling over the same issue without yet taking any decision.

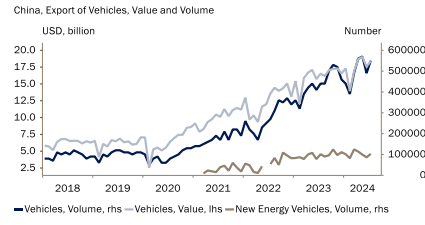

Part of the increase in imports from China reflects the lengthening supply chain and trade diversion following the US-China trade tensions that began in 2018. But the increase in import penetration is not limited to raw materials and intermediate goods. Imports of consumer goods from China have also increased. This is the case for passenger cars. The rest of the world has imported more internal combustion engine (ICE) cars from China, as producers have large spare capacity resulting from slowing demand. But imports of new energy vehicles (NEVs) have also increased rapidly. Again, the US and the EU have raised tariffs on NEVs from China, while most emerging markets have not (Chart 4).

Chart 3: China's steel exports end up mainly in emerging markets

Chart 4: China's exports of passenger cars have increased since 2020

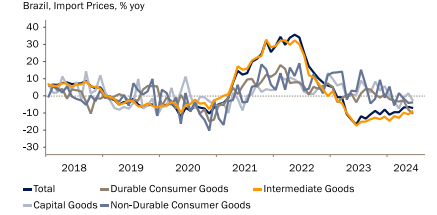

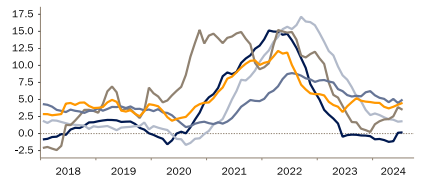

Have we seen any clear evidence of China ‘exporting deflation’ to emerging markets? We have looked at two emerging markets that have been among the top five destinations for Chinese passenger car exports (especially NEVs): Brazil and Thailand. We assume that a large share of Brazil's consumer durables are passenger cars. Brazil has experienced a fall in import prices of consumer durables, while consumer durables prices have been stable since 2023 (Chart 5). Although Brazil is a fairly closed economy, import competition may have put pressure on overall consumer durables prices. Stagnating durable goods prices have contributed to the disinflation process from the second half of 2023 onwards. However, consumer durable goods price inflation has not fallen as much as import price inflation in the recent period (Chart 6). This could be due to the weakness of the Brazilian real.

Chart 5: Falling import prices of consumer durables in Brazil

Chart 6: Fall in consumer durable goods prices

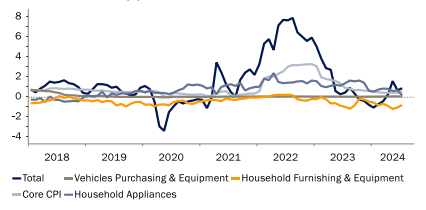

In Thailand, the Bank of Thailand (BOT) stated at its latest Monetary Policy Committee press conference that increased competition from imported goods from China has put downward pressure on Thai inflation. According to the BOT survey, import prices of consumer durables from China have fallen by around 10% from early 2023 to mid-2024. A large share of this is likely to be accounted for by passenger cars (Figure 7). Prices of non-durable goods imports from China have also fallen slightly over the same period. The large fall in prices of consumer durables imports from China has contributed to a flat overall durable goods import price index in 2023. In the consumer price index, vehicle prices have been stable for many years, but prices of consumer durables have declined. This has contributed to very low core inflation, close to zero, for quite some time (Chart 8).

Chart 7: Vehicle imports from China grew significantly in Thailand

Chart 8: CPI inflation at the lower end of the BOT target

Our main conclusion is that there is sufficient evidence that China has exported deflation to emerging markets. Interestingly, Brazil has recently increased its tariffs against Chinese NEVs and anti-dumping duties against Chinese steel. While other imported domestic goods could continue to contribute to lower inflation, China's support for Brazil's disinflation process is likely to diminish in the future.