Climbing a wall of uncertainties

3 NOV, 2025

By Thomas Hempell from Generali Investments

Political uncertainties abound in autumn with France’s new PM Lecornu struggling for survival and US/China tensions intensifying before a last-minute truce extension last week. The US government shutdown keeps depriving policy makers and investors of key US data. Markets keep climbing this wall of worries regardless.

The risk of partial setbacks has risen. Gains in global equities by ~35% from their April troughs are heavily concentrated in an increasingly circular AI ecosystem. Selected signs of stress emerged in private credit.

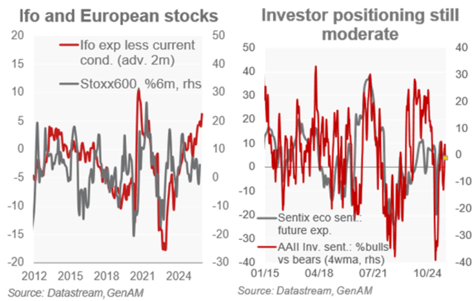

Still, economic fundamentals look conducive for risk sentiment. The US is headed for a slowdown, not a recession. Euro area’s PMIs, Ifo, ESI and ZEW point to an improving momentum. China seems on track to weather the 27%yoy (Sep.) slump in exports to the US. The inflationary impact of US tariffs keeps proving milder than feared. A solid earnings season keeps supporting risen valuations while market risk positioning remains moderate.

This setting still favours a moderate overweight in equities for now. We retain a small short duration in EUR fixed income with risks to Bund yields tilted to the upside. We still favour EUR IG Credit amid resilient risk premia as fundamentals remain decent and demand solid. We expect renewed USD weakness before long.