The Concentration of the Wealth Management Market in Europe: A Technical Analysis

15 JAN, 2025

By Jose Luis Palmer from RankiaPro Europe

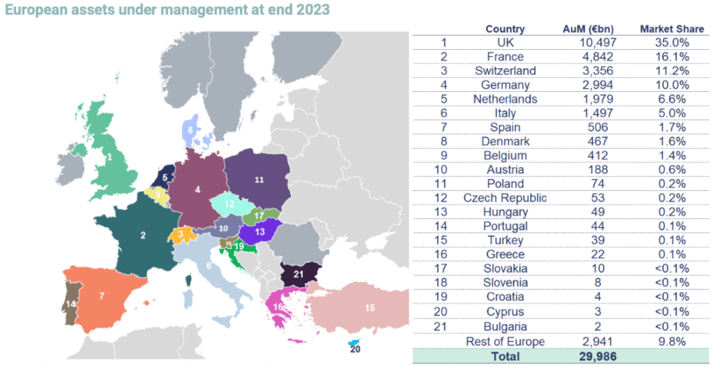

The European wealth management market is characterised by significant geographical and corporate concentration. According to the EFAMA 2025 report, six countries account for over 85% of the assets under management (AuM): the United Kingdom, France, Germany, Switzerland, the Netherlands, and Italy. This dominance reflects structural factors such as the presence of major financial centres, the scale of domestic savings markets, and regulatory specificities.

Determinants of AuM Concentration

- International financial hubs: London, Paris, Frankfurt, and Zurich act as key nodes attracting global capital flows, offering advanced infrastructure and financial connectivity.

- Domestic savings markets: Countries like the Netherlands stand out for their robust occupational pension systems, which drive locally managed volumes.

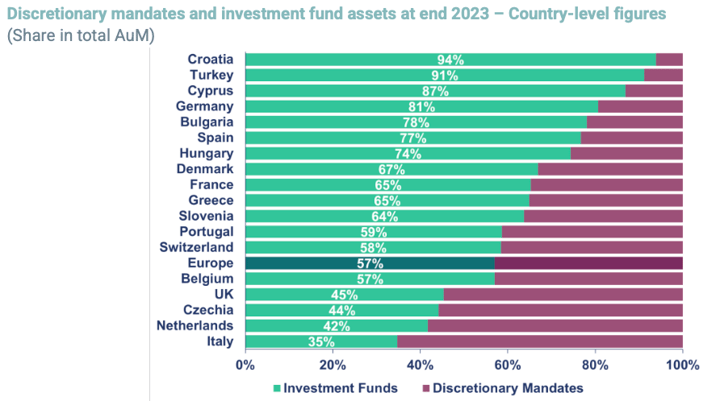

- National regulations: In Italy, discretionary mandates dominate among institutional investors, whereas Germany favours alternative funds.

The Evolution of Investment Funds and Discretionary Mandates

Investment funds have increased their share of total European AuM, reaching 57% by the end of 2023, compared to 43% for discretionary mandates. This shift is driven by differences in asset allocation: funds have greater exposure to equities (41% compared to 22% for mandates), benefiting from the superior returns of this asset class over the past decade.

At the country level, preferences vary significantly. In Italy, discretionary mandates are widely used by institutional investors, while in Germany, alternative funds are the primary investment vehicle for institutions.

Impact of Concentration on Sector Competitiveness

Despite overall growth in AuM, European asset managers face significant challenges in international competitiveness. European managers tend to be less profitable than their US counterparts due to:

- Fee pressure: The growing demand for passive solutions, such as ETFs, has compressed fee income.

- Rising operational costs: Investments in advanced technologies and compliance with sustainability and transparency regulations have increased general expenses.

In this context, market consolidation is an inevitable trend. EFAMA anticipates that the top ten managers will capture an even larger market share, driven by economies of scale and the pursuit of efficiencies.

European Market Integration: Progress and Challenges

The development of the Capital Markets Union (CMU) represents a critical goal to foster financial integration in Europe. Currently, 32.6% of European asset managers’ clients are foreign, a figure that has gradually increased since 2019.

To maximise the CMU’s potential, EFAMA highlights the need to:

- Simplify regulations: Reform the Retail Investment Strategy to facilitate access to capital markets.

- Boost pension savings: Implement auto-enrolment systems in occupational pension plans and offer attractive tax incentives.

Conclusion and Outlook

The high concentration of the European wealth management market presents significant challenges but also opportunities for asset managers capable of adapting to a transforming environment. Consolidation, technological innovation, and sustainability will be key factors in improving the sector’s competitiveness.

Looking ahead, deeper integration of European markets and regulatory alignment will be essential to unlock new investment flows and ensure Europe’s leadership in global asset management.