Cybersecurity: A Booming Sector for Investment

4 DEC, 2024

Josh Barber, investment manager at Schroders

The demand for cybersecurity has surged in recent years, with spending expected to exceed $200 billion by 2024. However, careful selection remains crucial for investors.

The digital transformation of global economies has led to an explosion in data creation, transfer, and storage. This shift has been accompanied by a rise in both the sophistication and frequency of cyberattacks, making cybersecurity a critical concern for businesses and governments alike. High-profile breaches, such as the 2017 Equifax hack, which exposed the data of 146 million U.S. customers and cost the company $1.5 billion, highlight the stakes. Similarly, the SolarWinds attack resulted in massive data theft from U.S. government agencies and corporations, with billions spent on remediation.

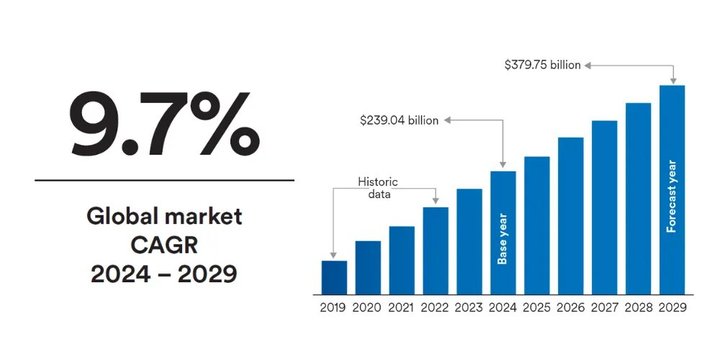

These threats underscore the need for robust cybersecurity measures, fueling an increase in IT spending. Global cybersecurity expenditure is projected to reach $240 billion in 2024 and may exceed $400 billion by 2030, with an annual growth rate of nearly 10%.

Industry Consolidation and Innovation

Beyond market growth, the ongoing consolidation within the cybersecurity sector presents a compelling case for investment. Established players are acquiring smaller competitors to expand their product portfolios and customer bases, bolstering market share and competitiveness. This trend enhances their ability to innovate and grow, making these companies attractive investment opportunities.

Additionally, the global shortage of cybersecurity professionals is a significant tailwind for leading industry players. By 2025, an estimated 3.5 million cybersecurity positions will remain unfilled. To bridge this gap, companies and governments are increasingly relying on artificial intelligence. Major firms such as Microsoft and Palo Alto Networks are heavily investing in AI solutions to address these challenges, strengthening their positions in the market.

Key Players in the Cybersecurity Market

Palo Alto Networks: Traditionally focused on securing data transfer and storage through cloud networks, Palo Alto has broadened its range of services to become a one-stop provider. This strategy has proven successful, with 1,000 of its top 5,000 clients exclusively relying on its services, driving record-high free cash flow margins. These profits enable further research and development, acquisitions, and potential shareholder returns.

Fortinet: Known for its industry-leading firewalls, Fortinet has expanded into higher-margin cloud-based solutions, now accounting for 25% of its revenue. This pivot reduces business cyclicality and strengthens its market position, enabling significant price increases. With different customer bases and revenue streams, Fortinet complements investments in Palo Alto, providing diversification within the sector.

Microsoft: While renowned for its software, Microsoft has made significant inroads into cybersecurity, integrating security solutions into its hardware, software, and cloud services. With cybersecurity revenue surpassing $20 billion—more than Palo Alto and Fortinet combined—Microsoft is poised to exceed $30 billion in the coming years. Its substantial investments in artificial intelligence and machine learning further solidify its leadership in the field, offering investors diversified growth opportunities.

A Stable and Promising Investment Opportunity

As institutions face mounting pressure to protect their digital assets, the demand for advanced cybersecurity solutions is set to remain strong. This ensures stable revenues and promising growth opportunities, making cybersecurity companies highly attractive additions to investment portfolios.