Dedollarization: Mission Almost Impossible?

Updated:

30 JAN, 2025

By DWS

The world largely depends on the US dollar. At the same time, however, there is a fundamental asymmetry between the decreasing importance of the US economy globally. As China and other emerging economies grow more rapidly, the global role of the US dollar in trade flows and as an issuing currency has tended to grow. In this context, and also for geopolitical reasons, in recent years attempts to break the dollar's dominance and establish an equivalent alternative have increased.

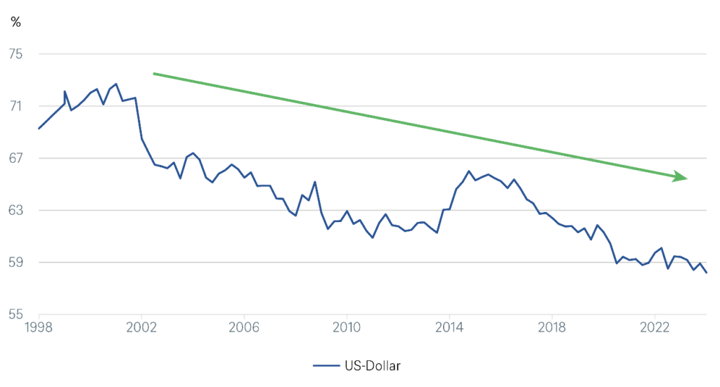

The proportion of US dollars in international currency reserves has significantly decreased

Signs of de-dollarization

Not only since the Russian attack on Ukraine has resentment grown, especially in emerging markets, towards the dominant position of the West and, by extension, the dollar. The first signs of de-dollarization are observed in commodities. In energy trade, transactions are increasingly settled in alternative currencies. An even clearer trend is observed in the international currency reserves of central banks. According to the International Monetary Fund (IMF), in the first quarter of last year, the US currency accounted for about 59% of international currency reserves; this figure is significantly lower than in the year 2000, for example, when the dollar accounted for just over 70%. However, as experts from J.P. Morgan point out, currency reserves offer an incomplete picture. A significant increase in dollar-denominated bank deposits, sovereign funds, and private foreign assets in emerging markets has more than offset the decline in reserves.

Figures that speak in favor of the dollar

For example, around 47% of all payments processed by the SWIFT system are still settled in US dollars. The euro, in second place, represents just under 23%, while the Chinese yuan (CNY)-also seen as a possible alternative to the dollar- occupies a distant fourth place with 4.6%.

The reality is that the debate about a viable alternative to the dollar among BRICS countries has so far not gone beyond words. In our opinion, the countries involved are too heterogeneous for a new currency to emerge in the short or medium term; being not only one of the main reserve currencies, but also a store of value and a global means of payment is a lot to ask. However, this does not mean that the dollar cannot weaken.

In principle, de-dollarization implies a shift in the balance of power between countries, which in an extreme case could lead to a new world order. Probably, the effects would be felt most strongly in the United States, although the focus would be less on the economic consequences and more on the impact on the capital market.

There is a diversification taking place that is moving away from the dollar. However, the dominance of the US currency still seems firmly rooted. Not only in finance does the dollar offer various advantages, such as liquidity and legal certainty when carrying out financial transactions. Also, it is likely that the electoral victory of Donald Trump will further strengthen the claim to international leadership of the US currency. It will probably be decades before the dominance of the dollar begins to noticeably crumble.