Decoding Emerging Markets: The Case for Active Exposure

24 OCT, 2025

By Schroders

Tom Wilson, Head of Emerging Market Equities at Schroders

Why should investors allocate funds to emerging markets, especially given the higher risks involved?

First, investing in emerging market equities provides access to opportunities in countries that represent more than 40% of global nominal GDP – that’s hard to ignore. Second, emerging markets offer diversification benefits within a global portfolio.

Let’s look at why the relative performance of emerging markets might be poised for change.

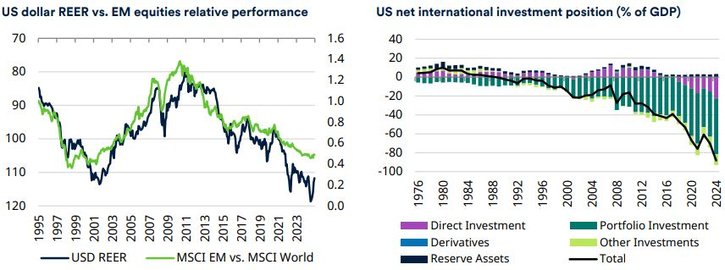

This brings us to the U.S. dollar. Emerging markets have a strong inverse correlation with the dollar, as the dollar and the U.S. yield curve influence financial conditions and nominal GDP growth in dollar terms for these markets. The chart on the left illustrates this relationship.

Source: Schroders, 2025

Therefore, a key decision when managing any emerging markets allocation is one’s view on the U.S. dollar. As noted, dollar appreciation has been a persistent drag on emerging markets for over a decade – until early 2025 – while supporting growth, investment flows, and valuations in the U.S. Currency momentum can persist far longer than what might be considered fair value, especially for the dollar, due to the “U.S. exceptionalism” thesis.

Currently, the dollar’s trade-weighted real effective exchange rate (REER) is highly valued, the U.S. runs a large twin deficit, and U.S. equities are relatively expensive. Investors are heavily exposed to U.S. assets, the net international investment position (NIIP) has widened, global central banks are diversifying reserves away from the dollar (even though it remains the dominant reserve and trade currency), and some U.S. policy choices have eroded confidence in the exceptionalism narrative. The dollar has already weakened notably this year, but there are reasons to believe we could remain in a dollar depreciation cycle for some time – potentially providing a strong tailwind for emerging market returns.

China Faces Structural Challenges

Investment as a share of GDP remains above 40%. While this may be sustainable in the short term thanks to high domestic savings, capital controls, and state influence over economic outcomes, it likely reflects a significant and persistent misallocation of capital. History shows that developing economies eventually shift from investment-led to consumption-led growth.

China’s non-financial debt is nearly 300% of GDP, its GDP deflator has been negative since Q2 2023, and the economy appears stuck in a liquidity trap. Fiscal deficits have reached double-digit levels as a share of GDP. Geopolitics adds further risk – tariffs, market access limits, technology transfer restrictions, and defensive corporate decisions all contribute to uncertainty and higher risk premiums.

However, this overlooks how far China has come as an industrial powerhouse. Its competitive edge goes beyond low labor costs – it enjoys scale advantages and powerful network effects through supply chain clusters. Chinese firms have invested heavily in R&D, improving product quality and competitiveness. As China has moved up the value chain, it continues to replace imports and gain export market share.

China also dominates certain industries, including the renewable energy supply chain, largely due to long-term industrial policy. It controls around 90% of global rare earth processing capacity – a major bargaining chip in tariff negotiations with the U.S.

Chinese companies have also proven highly innovative, both in hardware and software, and in developing new business models. Despite risks, this backdrop offers a broad range of ongoing growth opportunities, supporting China’s potential to avoid the “middle-income trap.”

Taiwan and South Korea: Technology-Driven Markets

South Korea faces structural issues such as high leverage, unfavorable demographics, a rigid labor market, and rising competition from Chinese firms. However, its equity market is cheap, and governance reform could support valuations under the new president. Technology represents about 40% of the market, dominated by Samsung Electronics and SK Hynix. While they face Chinese competition in low-end NAND and DRAM memory, both are strong in high-bandwidth memory (HBM) – essential for AI infrastructure growth. Korea also competes in industries such as shipbuilding, nuclear energy, defense, and electrification – areas protected by supply security concerns.

Taiwan also faces demographic challenges, but its external and fiscal balances are strong. About 80% of the market is tech, with TSMC alone making up half. TSMC dominates advanced-node logic chips, with strong pricing power and competitive advantages. Beyond TSMC, Taiwan offers a broad range of tech investment opportunities.

We see technology as a continuing structural opportunity – though it’s a cyclical and highly competitive sector that demands deep understanding. Tech hardware accounts for over 20% of the emerging market benchmark index.

India: A “Traditional” Emerging Market

India’s urbanization rate is low (36%), and 46% of the workforce is in agriculture. If India can create jobs, long-term productivity growth potential is significant. Prime Minister Modi’s government has worked to improve the investment climate through reforms and infrastructure spending.

India still faces hurdles – bureaucracy, protectionism, labor rigidity, lack of skills, and access to land and energy – but digitization, urbanization, financial deepening, public investment, positive demographics, and prior reforms support private investment and medium-term productivity growth.

Valuations remain high, making timing and entry points key for long-term value creation.

Risks

No discussion of emerging markets would be complete without addressing risks. These markets carry higher risks related to macroeconomic and currency volatility, rule of law, ease of doing business, governance, and politics. The key question is whether investors are adequately compensated for these risks.

Country-specific risks include geopolitics, protectionism, supply chain diversification, leverage, fiscal strain, climate change, demographics, the middle-income trap, and competitive intensity – some of which also affect developed markets.

U.S.–China tensions remain a major factor. Issues like protectionism, supply security, self-sufficiency, and economic friction hurt global efficiency. China retains defenses through supply chain integration and rare earth dominance, but it’s disadvantaged in access to U.S. markets, technology transfer, and tariff outcomes. Europe may also turn more protectionist as it defends its industrial base against perceived Chinese subsidies and overcapacity.

Greater geopolitical tension incentivizes China to push harder for self-sufficiency, especially in key technologies – seeking to maintain global leadership in select sectors.

Manufacturing reshoring to the U.S. is likely only where automation and margins are high, as cost and labor constraints remain significant. China’s limits could encourage supply chain diversification within emerging markets – though its industrial capacity still poses competitive threats.

Assessing and managing these risks – and using them as opportunities – is a core function of active management in emerging markets.

Conclusion

Emerging markets represent 21% of global equity indices and 41% of global nominal GDP, justifying a steady allocation to EM equities. When approached correctly, they can enhance diversification and risk-adjusted returns in a global portfolio.

While rising U.S.–China tensions and protectionism have increased volatility and risk compared to the 2001–2020 period, valuations remain reasonable, growth drivers are broad, and a weaker dollar could be a major positive factor for emerging market equities.