Emerging Market Investing: Opportunities and Risks for Professional Investors

10 FEB, 2025

By Renu Pothen

Emerging markets are an integral part of the global economic order, growing faster than advanced economies over the last twenty-five years. Currently, these economies account for 60% of global GDP based on purchasing power parity (PPP), up from 41% in 2000. Meanwhile, the share of these economies in the world population is 86%. The International Monetary Fund's (IMF) latest World Economic Outlook projects that the growth for emerging markets will be 4.2% in 2025, compared to 1.9% for advanced economies. The projections for emerging markets over the next decade also appear very promising. S&P Global, in its Look Forward Journal titled "Emerging Markets: A Decisive Decade," predicts that emerging markets will drive global economic growth from 2024-2035 with an average annual GDP growth rate of 4.06% while that of advanced economies will be 1.59%. Emerging markets are expected to contribute 65% of the global economic growth, with nine ranking among the twenty largest economies globally. These include China, India, Indonesia, Brazil, Russia, Mexico, Turkey, South Korea and Saudi Arabia. Notably, India is projected to become the third-largest economy by 2035, while Indonesia and Brazil are expected to be ranked eighth and ninth, respectively.

How do you define Emerging Markets?

There is an interesting story behind the origin of the term "emerging markets." In 1981, Antoine van Agtmael, a staff member of the International Finance Corporation (IFC), proposed a global equity fund for developing countries called the "Third World Equity Fund." However, an investment banker suggested it would be difficult for the IFC to attract investors for this fund as the name evoked negative connotations. Hence, van Agtmael changed the name to "Emerging Markets" as it implied progress, uplift, and dynamism, while "Third World" at that time was associated with extreme poverty, shoddy goods, and hopelessness. Since then, the term emerging markets has been widely used to describe developing countries across the globe.

The question arises: which economies are considered emerging markets? According to the IMF World Economic Outlook, 41 economies are classified as "advanced," while the remaining countries are included in the "emerging and developing" economies category. Among these, the IMF Fiscal Monitor classifies forty as "emerging market and middle-income" economies. These economies are characterized by stability and strong economic growth potential and are similar to advanced countries in their higher incomes, production of higher-value-added goods, representation in global trade, and integration into the financial system. These countries are then ranked as the top 20 emerging markets based on five weighted variables: nominal GDP, population, GDP per capita, share of world trade, and share of world external debt. Furthermore, these top-ranking emerging markets have also found their place in the indices that track emerging markets, such as those by J.P. Morgan, Morgan Stanley, and Bloomberg.

Now, if we have to define emerging markets from an investor's perspective, we can briefly look at the MSCI Emerging Markets Index, one of the most prominently used indices globally to track emerging markets. Launched in 1988, the index initially included ten markets with a market cap of $50 billion. The index is not static but dynamic, as its constituents have been added and removed over the years to reflect a broad range of emerging markets that have undergone economic transformation.. For instance, Latin America was the largest region within the index in the initial years, while countries such as China, India, and Russia were not included. As of January 31, 2025, the MSCI Emerging Markets Index consists of twenty-four countries with a total market cap of $7.79 trillion. The top five constituents of the index are China (27.5%), Taiwan (20.02%), India (18.41%), South Korea (9.43%) and Brazil (4.49%).

Emerging Markets - Opportunities & Risks for Investors

Emerging markets have become economic powerhouses in the global economy, but their long-term performance has not been particularly encouraging. For instance, the MSCI Emerging Markets Index has generated an annualized return of 4.16% compared to 11.11% for the MSCI World Index in the last ten years. Factors contributing to this underperformance include a strong dollar, low commodity prices, a slowdown in China, the largest constituent in the index, and geopolitical tensions. The performance has definitely been disappointing, but emerging markets present many opportunities besides strong growth prospects and attractive valuations, which will significantly enhance the value of investor portfolios.

The rising share of Emerging Markets in Global Market capitalization

According to Goldman Sachs Research, the share of emerging markets in the global market capitalization is projected to rise from 27% in 2022 to 47% by 2050 and 55% by 2075. The share of China is expected to increase from 10% in 2022 to 15% by 2050 but will decline to 13.5% by 2075. In contrast, India will witness the most significant rise in market capitalization from 3% in 2022 to 8% by 2050 and 12% by 2075. Meanwhile, the US will see its share in the global market capitalization decline from 42% in 2022 to 27% and 22% by 2050 and 2075, respectively. The rise in the market capitalization of emerging markets in the near future is an indication that their capital markets will only strengthen from here, and this will boost the confidence of both domestic and foreign investors. This trend also points towards sustained improvements in economic growth and robust earnings growth for companies in these economies.

Portfolio Diversification

In the MSCI World Index, the share of the US is 73%, while within the MSCI Emerging Markets Index, China's share is 27%, which declined from ~ 42% in 2020. Currently, both Taiwan and India constitute 38% of the index. Investments in emerging markets allow investors to scout for opportunities across many regions, including the Asia-Pacific (APAC), Europe, the Middle East and Africa (EMEA), and Latin America. This approach also gives investors access to more companies within specific industries and sub-industries.Investors can consider including emerging markets in their portfolios as they have a relatively low correlation with the US market.

Demographic dividend

One of the most significant game changers for emerging markets is their demographic dividend. If an aging population is a concern in many developed countries, other regions worldwide are experiencing a youth bulge (15 to 24 years). The United Nations projects that by 2030, the number of older people in Europe will surpass those under twenty. The population aged 15 to 24 is expected to increase in 82 countries between 2020 and 2050. Notably, the young working population is expected to grow by 151 million, and 73% will be in Africa.

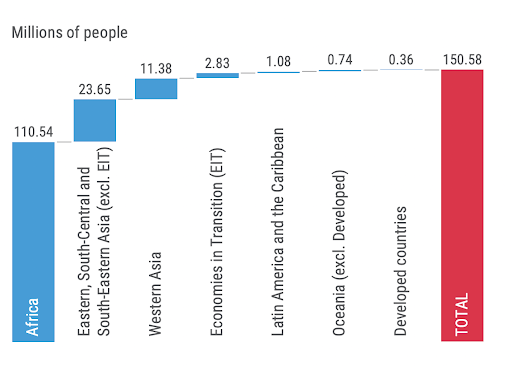

Projected increase in the population aged 15-24 years by region between 2020 and 2050

A young population means that there will be increased labor force participation, which will, in turn, impact consumption, savings, and investment patterns within these economies. In this case, one of the biggest trends is the rise of a burgeoning middle class with increased purchasing power, which will drive consumer demand and contribute significantly to economic growth. According to a report from the Brookings Institution, some of the largest consumer markets of this decade will be in emerging markets, with China and India continuing to be dominant consumer giants.Another interesting trend observed in recent years is that spending on luxury brands within these economies has increased as more wealth is being created, prompting these brands to focus their efforts in this region.The demographic transition occurring in emerging markets is remarkable but can also be challenging. Hence, policymakers must focus on skill development and employment generation to effectively manage this youth bulge.

Huge infrastructure requirements from Emerging Markets

Emerging markets have already become prominent players on the global stage, whether in terms of their contribution to world GDP and population size. These economies will have to invest heavily in infrastructure to continue on a growth trajectory. According to the G20's Global Infrastructure Hub's report, global infrastructure investment needs are projected to reach $97 trillion by 2040. Asia will have the largest infrastructure needs, estimated at $52 trillion by 2040. Among the emerging markets, China and India will be two of the top four economies, alongside the US and Japan, requiring the maximum infrastructure investments by 2040. Since infrastructure investments require considerable capital, which can strain the fiscal health of these markets, their reliance on capital markets is expected to increase in the future.

The rising dominance of Emerging Markets in AI

The IMF has projected in a report that emerging markets and low-income countries will be less disrupted by AI as their share of high-skilled jobs is lower compared to their advanced economies. However, Asia has been in the race for AI dominance for some time. For example, Taiwan is a key player in producing advanced semiconductor chips required for AI.The Taiwan Semiconductor Manufacturing Company (TSMC) holds a 60% market share of the global semiconductor foundry market and is the world's largest foundry in the semiconductor industry. Interestingly, a close analysis of the MSCI Emerging Markets Index shows that TSMC is the largest holding, with an average allocation of 9% over the last one year. Additionally, China's DeepSeek R1 model has created significant ripples across global tech firms, and we will soon know whether this will disrupt the AI industry.

Emerging markets offer many viable investment opportunities but have specific risks that should not be ignored. These risk factors should be considered while investing in these markets because they tend to influence performance in the long run.

Currency Fluctuations

A strong dollar can lead to a rise in imported inflation while increasing domestic inflation and the chances of a tighter monetary policy. The other challenges include the flight of foreign capital and an increase in the cost of servicing the dollar-denominated debt. All these factors will adversely impact the profitability of companies and can lead to a slowdown phase. The Fed maintained the status quo on rates in its recent policy meeting, and President Trump has decided to impose tariffs on Canada, Mexico, and China; both of these events will affect the dollar in the coming months. Emerging markets will feel the heat of these actions, so any investments in them should be approached with caution.

Geopolitical Risks

Geopolitical risks can adversely impact even the most stable emerging markets, at least for a short period. A recent example is the Russia-Ukraine war, which affected many emerging markets due to their dependence on both these countries for their energy and food requirements. Additionally, within specific emerging markets, risks related to instability in the existing political landscape, changes in regulations concerning the different asset classes, or a major corporate governance issue can lead to volatility that can, in turn, impact the performance of these markets.

Final reflections

Many of the emerging markets unleashed robust economic and market-friendly reforms that have led to strong and resilient macroeconomic indicators, effective regulatory frameworks, and monetary policies while maintaining fiscal prudence. It is also important to note that some fragile emerging markets are embracing necessary economic reforms, enabling them to improve their future growth prospects.The growing importance of the ten emerging markets of G20 (Argentina, Brazil, China, India, Indonesia, Mexico, Russia, Saudi Arabia, South Africa, and Turkey) can be seen not only in terms of their contributions to global growth but also international trade, global supply chains, and financial markets. A recent study by the IMF proves this point, wherein growth spillovers from China have significantly impacted global GDP, inflation, and commodity prices. In contrast, the spillovers from other G-20 emerging markets like Russia and Saudi Arabia tend to have a more regional impact. Furthermore, growing investor interest in these markets can be seen from the increase in the share of emerging markets in the MSCI ACWI Index, which has increased from less than one percent in 1988 to 10%.

The question in front of investors is whether this is the right time to enter emerging markets, as the global economy is already going through many uncertainties. The emerging markets are trading at a discount to developed countries, which means that there are many opportunities that they will offer. The rising disposable income of their middle class is leading to a significant increase in consumption and investments in the financial markets. Additionally, the huge emphasis on infrastructure initiatives to meet the growing demands of urbanization and improving the quality of life of their population suggests that their economic growth will be sustainable and inclusive.

The world has faced many challenges over the past two decades, yet the ten emerging markets of G20 have shown rapid growth, averaging a 6% growth rate. The underperformance and the risks associated with these markets cannot be undermined, but investors may still consider exposure to them through passive or active strategies. Emerging markets are generally considered inefficient, particularly in their mid-cap and small-cap segments, wherein there is a higher risk-return probability. Hence, investors interested in active strategies should go for funds from fund houses that have immense local expertise in these markets. As emerging markets tend to be volatile, risk-averse investors with a long-term horizon may consider diversifying their portfolios by taking exposure to these markets.