Emerging Markets currencies outlook

Author: Mali Chivakul, Emerging Markets Economist at J. Safra Sarasin Sustainable AM

The US dollar's strength has put further pressure on emerging market currencies (EMFX), after a weak performance in the first quarter. While we do not expect the dollar to strengthen going forward, given the slowdown in US activity and the gradual decline in inflation, we also do not expect the dollar to weaken much by the end of the year. Our target for the dollar at the end of the year is only 1% below the current level. This implies a sideways movement for EMFX until the end of the year. However, there have been a number of idiosyncratic risks from the elections that have influenced EMFX and could move them further.

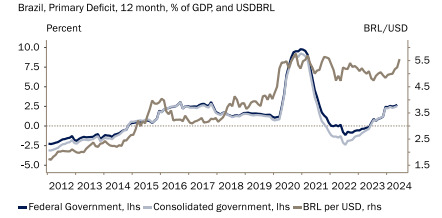

Latin American currencies have been affected by fiscal and institutional concerns. In Brazil, the looming fiscal risk has been ignored by markets in the first months of the year. However, as time goes on, it has become clear that Brazil will not be able to reach its zero primary deficit fiscal target this year without some significant spending cuts (Figure 1). The Brazilian real has lost 12.5% so far this year, the worst fall among major emerging markets, despite the strong performance of its economy. The next important date for the Brazilian real is 22 July, when budget cuts could be unveiled. Concrete and credible cuts should reverse some of the recent weakness. Without credible cuts and a new commitment to fiscal rules, the real is likely to hover around the current level.

The Mexican peso reacted strongly to the surprise election result in early June, but has since recovered somewhat. The likelihood of constitutional changes that current president López Obrador proposed in February has pulled the market back. After losing 10% in the week after the election, the Mexican peso recovered 4% and now stands at 18. The currency has lost 6% so far this year. Given our expectations that Banxico will keep its policy rate high for longer (it is likely to cut it as much as the Fed), a relatively high carry should continue to support the peso, even if there are many risks on the horizon, such as the US elections and the 2025 budget. Still, we expect more volatility.

Figure 1: Fiscal concerns have driven BRL depreciation

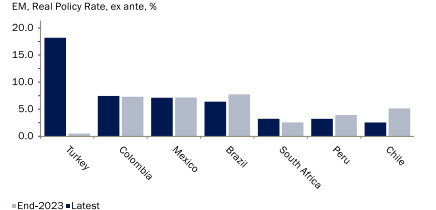

Figure 2: Higher real rate

Despite the high carry, we continue to see elevated fiscal risks in Colombia, which should put downward pressure on the Colombian peso (Figure 2). A few days ago, the government published its Medium-Term Fiscal Framework, which suggests that the fiscal deficit will remain high at 5.1% in 2025, after a deficit of 5.6% this year. In Peru, interest rate cuts have been offset by the rebound in copper prices, which peaked in mid-May. We do not expect a further copper rally, as the US is slowing down and China's copper stocks are already high. The Peruvian sol/dollar exchange rate has only lost 2% so far this year, and should remain more or less stable unless copper prices fall much further. The Chilean peso has not benefited from the rise in copper prices this year, having lost 6% so far this year. This implies that investors are more concerned about the weak recovery. It continues to have problems with copper production and rising inflation has led the central bank to halt its rate cutting cycle at 5.75%.

So far this year, the euro-zloty exchange rate has gained 2%, while the dollar-zloty exchange rate has lost only 0.2%. We continue to see depreciation pressures on the Czech koruna due to lower carry, a weak economy and an expensive real exchange rate. Hungary's fiscal outlook, which has been the main concern over the last 12 months, has improved somewhat after the government recently presented new measures to cut deficits. The improved external outlook, as well as a relatively cheap valuation, should support the forint, once the fiscal outlook becomes clearer.

With the highest carry among emerging markets, the Turkish lira has been a favourite emerging market currency. Since our February publication on Turkey, we have seen a further improvement in inflation and inflation expectations. Dollarisation has fallen and trade balances have improved. The real (ex ante) rate has risen significantly (Figure 2). The dollar-Turkish lira exchange rate has stabilised at around 32 after the local elections in March, mainly due to foreign capital inflows. Although the currency still needs to correct further, we continue to expect a good summer and high carry to offset any depreciation until the end of the year. In South Africa, the improving power situation, increased fiscal consolidation efforts and expectations that the unity government will be shut down soon have pushed the rand higher. Decent carry should also support the ZAR (Figure 2).

In Asia, the region with the largest carry disadvantages, we continue to see pressure on most currencies. While there is no reason for the People's Bank of China to devalue the Chinese yuan (CNY), it is likely to depreciate slowly during the second half of the year. However, possible US tariffs could weaken it much further by the end of the year. CNY weakness often translates into regional weakness as well. We expect the Indian rupiah to remain more or less stable, given the higher inflows in the local bond market and the Reserve Bank's intervention. The Indonesian rupiah will remain under pressure as long as the dollar remains strong. We are not too concerned about recent news of the new president's possible fiscal profligacy, as we remain confident that the new government will continue to stick to its conservative fiscal targets. In Thailand, although the economy has improved in recent months, the Thai baht did not benefit from the increase in tourism receipts in the last high season, leading us to conclude that it will remain around the current level until the end of the year.