Emerging Markets: A Fertile Ground for Sustainable Investments

2 APR, 2025

Author: Mathieu Quenechdu, ESG Analyst at IVO Capital Partners

Sustainable investment in emerging markets is often perceived as limited due to a lack of sufficiently green alternatives. However, this reasoning is flawed: Emerging countries are undergoing an evolving energy mix and a decarbonization in their electricity production. The electricity and heat sector is the world’s leading source of GHG emissions, but also the one where transition is the most affordable thanks to existing technologies (solar, wind, hydroelectricity, etc.).

Some emerging countries are already at the forefront of this shift. In Latin America, renewables account for over 50% of electricity generation, demonstrating the region’s leadership in clean energy adoption. Replacing carbon-intensive power sources with renewables has an immediate and substantial impact on emissions. Many emerging markets, particularly in Asia, are also accelerating this transition. For example, India is ramping up its renewable investments with a $13.3 billion plan for 2024 (a 40% year-on-year increase, Ember, Navigating risks to unlock 500 GW of renewables by 2030, February 2025) to diversify its energy mix and reduce coal dependency. Investing in renewables is effectively a direct trade-off against fossil fuels, leading to significant net emission reductions (by a factor of 665 for coal and 98 for gas per unit of electricity generated) by reallocating capital to low-carbon solutions.

At the same time, emerging economies are experiencing rapid growth in energy demand, requiring expanded electricity access to support development. By 2030, these markets are expected to account for 80% of the additional global electricity demand. Meeting this surge with low-carbon energy sources is crucial to minimizing the environmental impact of this expansion.

Ultimately, emerging markets play a pivotal role in the global energy transition. Regions like Latin America are already heavily reliant on renewables, while countries like India are making bold investments in clean energy to meet rising demand. Recognizing this momentum challenges outdated perceptions and underscores the potential for sustainable investment in these markets.

ESG reportings aligned with international standards

Contrary to popular belief, the lack of transparency among emerging-market companies is becoming less of an issue. While ESG disclosure requirements are facing increasing scrutiny in developed countries) particularly with the anti-ESG stance of the Trump administration in the U.S. and the Omnibus Act in the EU) emerging markets are moving in the opposite direction, aligning their corporate disclosure standards with international norms.

Several countries have already taken significant steps. In Brazil, the Securities Commission now requires publicly traded companies to comply with the IFRS Sustainability Disclosure Standards (ISSB). Mexico has adopted the same requirement for companies listed on its markets, effective January 2025. Meanwhile, Colombia integrated a green taxonomy into its legal framework in 2022, defining clear criteria for issuing green and sustainable bonds.

Far from lacking sustainable investment opportunities, emerging markets are actively strengthening their regulatory frameworks to facilitate ESG-driven investing. The question now is: how is sustainable investment evolving across these economies?

Investment Deficit in EM: Mobilizing International Capital for a Global Sustainable Energy Transition

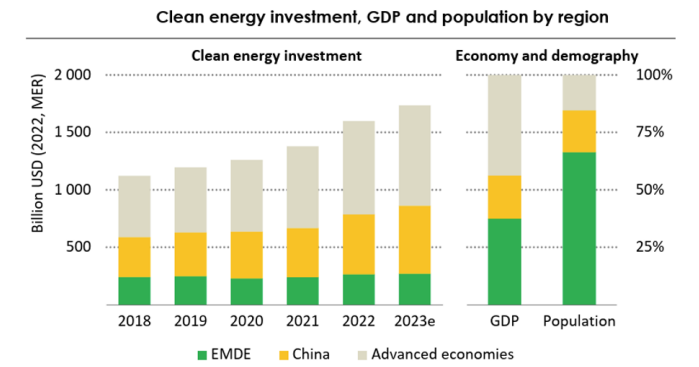

The latest report from the International Energy Agency (IEA) highlights a significant shortfall in clean energy investment for emerging economies. Despite representing nearly two-thirds of the global population and a growing share of energy demand, these countries receive less than 20% of global clean energy investments. This imbalance underscores the urgent need for increased capital flows to support their energy transition.

Given the limited availability of local financing, scaling up international funding is crucial, with a target of tripling it by 2035. Public sector institutions, such as Development Finance Institutions (DFIs), the World Bank and the African Development Bank all play a pivotal role in this effort. However, private sector investors and capital markets are just as critical in closing the funding gap.

One promising development is the rapid growth of green bond issuance in emerging markets, which surged by 50% between 2022 and 2023 and now represents 40% of the global green bond market in 2023. Yet, despite this progress, overall funding remains insufficient to meet the scale of investment needed (World Investment report 2024 – UNCTAD).

So, what barriers still hinder greater capital inflows into emerging markets?

High Cost of Capital: Drag or Investment Opportunity?

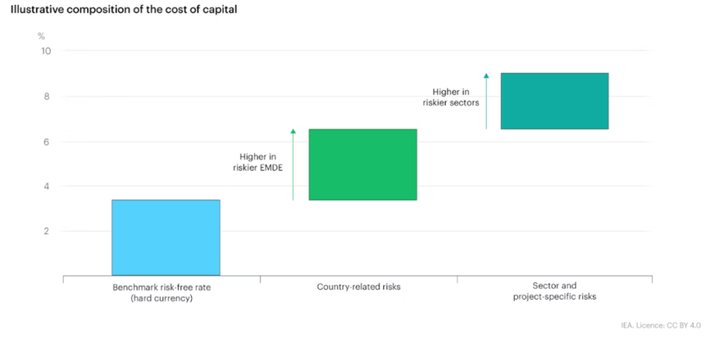

Today, the primary obstacle to sustainable investment in emerging markets is the high cost of capital (WACC). This metric, which represents the return on investment required by shareholders and creditors, is considerably higher in emerging markets than in developed economies. As a result, financing clean energy projects becomes more expensive, limiting the pace of the energy transition.

Investors demand a risk premium to finance companies operating in emerging economies due to factors like currency fluctuations, political instability, and regulatory uncertainties. These risks elevate the cost of capital, thereby limiting capital inflows. Moreover, the credit ratings of many companies in these markets, often classified as "high yield," further diminish their attractiveness to potential investors.

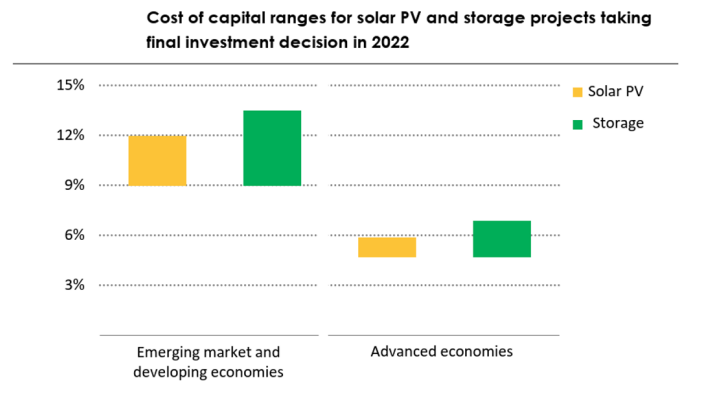

For example, in a solar energy project, financing costs can be up to twice as high as in developed markets for a comparable project. On average, around 65% of the capital cost for solar projects is debt-financed, amplifying the impact of these higher financing costs.

High capital costs are hindering project financing in emerging markets, despite the clear need for investment. Reducing these costs could alleviate the annual financing gap—just a 100-basis-point reduction could lead to savings of approximately $150 billion per year, making it easier to achieve energy transition goals.

While high capital costs reflect a higher risk premium, they also present attractive investment opportunities for those seeking higher returns. Navigating the emerging market landscape requires deep expertise and a thorough, "bottom-up" analysis of issuer quality, as well as the strategies they implement to address the identified risks.

Conclusion

The financing needs in emerging markets are clear, and impactful sustainable investment opportunities abound. However, these opportunities are often constrained by the high cost of capital in these regions. Despite this, financing sustainable development in emerging economies presents a unique chance to capitalize on long-term investment trends in strategic infrastructure. Historically, such investments have offered better return visibility and greater stability for credit investors compared to more cyclical industries.